There are many factors that influence the price of collision insurance. Collision insurance covers the cost of repairing or replacing your car after an accident or collision with an object. It is often paired with comprehensive coverage, which covers incidents such as theft, fire damage, and natural disasters. The cost of collision insurance can vary depending on the insurer, but it tends to be expensive because it is typically included in a full-coverage policy, and cars are becoming more expensive to repair or replace. Collision insurance rates can also be influenced by factors such as age, gender, location, driving record, and the make and model of the car.

| Characteristics | Values |

|---|---|

| Age and gender | Statistically, younger drivers and males pay higher premiums |

| Driving record | The more violations you have, the higher your risk of filing a claim, resulting in a rate increase |

| Coverage gaps | Gaps in coverage can make you seem like a higher risk, leading to higher rates or denial of coverage |

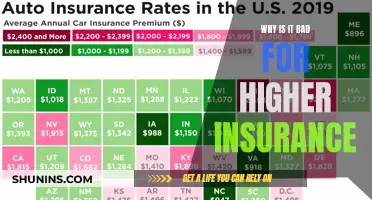

| Location | Living in an area with a high rate of theft, accidents, or weather-related claims can increase rates |

| Car make and model | Certain makes and models have higher collision losses, higher repair costs, and more insurance claims, leading to higher rates |

| Deductible | Choosing a higher deductible can lower your insurance premiums, but you'll pay more out-of-pocket when you make a claim |

| Policy changes | Adding a new driver, especially a teen or high-risk driver, can increase rates |

| Car value | More expensive cars tend to have higher insurance rates due to increased risk of theft and higher repair or replacement costs |

Explore related products

What You'll Learn

- Collision insurance covers damage sustained in an accident with another vehicle or object

- Higher repair and replacement costs can lead to higher insurance rates

- Age, gender, and marital status can influence the price of insurance

- The make and model of your car can affect your insurance rate

- Coverage gaps can make you seem like a higher risk, leading to higher rates

![]()

Collision insurance covers damage sustained in an accident with another vehicle or object

Collision insurance is a type of auto insurance that covers damage sustained in an accident with another vehicle or object. It is important to note that collision insurance only covers the policyholder's vehicle and not damage to other vehicles or objects involved in the accident. This type of insurance is often paired with comprehensive coverage, which covers incidents such as theft, fire damage, and natural disasters. Collision insurance is typically more expensive than comprehensive insurance because it is included in a full-coverage policy, and the odds of filing a collision claim are statistically higher. The average collision claim can cost more than $3000, making it a costly affair.

Collision insurance is not required by state law, but it is a smart option to protect your investment in your vehicle. It is especially important for new drivers, such as teenagers, who have less experience on the road. If you are leasing or financing your vehicle, your lender may require you to purchase both collision and comprehensive coverage.

The cost of collision insurance can vary by insurer, and there are ways to lower your premiums. One way is to increase your deductible, which is the amount you pay out of pocket before your insurance coverage begins. While a higher deductible can result in premium savings, it also means you'll pay more when you make a claim. Another way to reduce your collision insurance costs is to drive safely and maintain a good driving record.

Additionally, collision insurance covers a wide range of accident types, including accidents involving only your car, such as rolling over, or accidents with objects such as telephone poles, guardrails, or potholes. It is important to note that collision insurance does not cover bodily injuries sustained in the accident. Overall, collision insurance provides valuable protection against financial loss due to physical damage to your vehicle.

Flood Insurance: Can I Get Covered Now?

You may want to see also

Explore related products

![]()

Higher repair and replacement costs can lead to higher insurance rates

The make and model of your car can significantly influence your insurance rates. The more expensive your car is, the higher your insurance rate is likely to be. This is because more expensive cars are more likely to be stolen and cost more to repair or replace. Certain car models are also known to cause more damage to other vehicles, which also increases the likelihood of a costly insurance claim.

Cars with low safety ratings, high repair or replacement costs, and a history of frequent insurance claims will also result in higher insurance rates. This is because these cars tend to cost insurers more in claims costs, and insurers will price policies accordingly to mitigate their risks. For example, according to IIHS-HLDI, the Malibu, Altima, and K5 have higher-than-average collision losses, meaning it costs insurers more to repair these cars when they are involved in a collision, regardless of fault. As a result, if you own one of these cars and have collision car insurance coverage, your rate is likely to be higher.

The age and gender of the driver can also influence insurance rates. Statistically, younger drivers and males pay higher premiums. This is because younger drivers have less experience on the road and are more likely to be involved in an accident or collision, resulting in higher insurance claims. Additionally, males are generally considered to be more aggressive drivers and are therefore perceived as a higher risk by insurance companies.

Finally, it is important to note that insurance rates can be influenced by factors beyond your control, such as increased claims in your area due to extreme weather damage, accidents, or other factors. These factors can contribute to higher repair and replacement costs, which insurance companies will reflect in their pricing.

Strategies to Reduce GEICO Auto Insurance Premiums

You may want to see also

Explore related products

![]()

Age, gender, and marital status can influence the price of insurance

Age, gender, and marital status can all influence the price of insurance. Statistically, younger drivers and males pay higher premiums. This is because younger drivers are considered to be less experienced and more likely to take risks, resulting in a higher number of accidents and subsequent insurance claims. Being male is also considered a risk factor, with men generally paying higher insurance premiums than women.

Marital status is another factor that can impact insurance rates. Married individuals are often offered lower insurance premiums compared to single individuals. This is because married people are statistically seen as more stable and responsible, thus presenting a lower insurance risk. Insurance companies may view unmarried individuals as more likely to engage in risky behaviour, which could increase the likelihood of accidents and insurance claims.

In addition to age, gender, and marital status, other factors such as driving history, claims history, and location can also influence insurance rates. For example, individuals with a history of speeding tickets, accidents, or insurance claims may be considered high-risk drivers and face higher insurance premiums. Similarly, living in an area with a high rate of accidents, theft, or weather-related damage can increase insurance rates, as the likelihood of filing a claim is perceived to be higher.

While age, gender, and marital status are beyond an individual's control, it is important to note that insurance companies use statistical data and risk assessment to determine insurance rates. By considering multiple factors, insurance companies aim to balance their risk while providing coverage for their customers. It is always beneficial to compare insurance rates and review the specific factors that influence the price of insurance to ensure a fair and competitive rate.

To lower insurance costs, individuals can consider increasing their deductible, which is the amount paid out of pocket before insurance coverage begins. A higher deductible typically results in lower premiums, but it is important to remember that this also means higher out-of-pocket expenses in the event of a claim. Additionally, reducing unnecessary coverage, such as roadside assistance if already covered by another source, can help lower monthly premiums.

Motorcycle Insurance: Motor Vehicle Classification

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

![]()

The make and model of your car can affect your insurance rate

The make and model of your car can significantly influence your insurance rate. This is due to several factors, including the frequency of insurance claims associated with that particular make and model, the cost of repairs, and the safety features of the vehicle.

Firstly, the more claims filed for a specific make and model, the higher the insurance rate is likely to be. This is because insurers interpret a higher number of claims as an increased risk, leading to higher premiums. For instance, the Malibu, Altima, and K5 have been identified as having higher-than-average collision losses, resulting in elevated insurance rates for these vehicles.

Secondly, the cost of repairing or replacing a vehicle is a crucial factor in determining insurance rates. Expensive car models tend to have higher insurance rates because they are more costly to repair or replace. Additionally, cars with higher trim levels may also have higher rates since they are likely to be more expensive to repair due to their additional features.

Conversely, vehicles with superior safety ratings may benefit from lower insurance rates. Insurers consider cars with advanced safety features to be less likely to be involved in accidents or to sustain less damage in collisions, reducing the potential costs of claims.

It is worth noting that insurance rates are influenced by various factors beyond the make and model of the vehicle. These factors include the driver's age, gender, driving record, location, and the presence of any discounts or loyalty rewards offered by the insurance company.

While the make and model of your car can impact your insurance rate, it is essential to consider the overall cost of ownership, including maintenance, fuel efficiency, and resale value, when making a purchasing decision.

Vehicle Registration and Insurance: Keep or Toss?

You may want to see also

Explore related products

![]()

Coverage gaps can make you seem like a higher risk, leading to higher rates

Gaps in your insurance coverage can make you seem like a riskier client to insurance companies. This is because insurance companies interpret lapses in coverage as an indication that you may be a less careful driver or that you may have financial difficulties. As a result, they may increase your rates or even deny you coverage altogether.

If you're facing a coverage gap, it's important to consider your options carefully. One option is to pause or reduce your coverage if you're unable to afford your current premium. While this may result in higher rates or a denial of coverage, it can be a temporary solution until you're able to secure a new policy.

Another option is to shop around for a new insurance provider. Different insurance companies may have different rates and requirements, so it's worth comparing their offers. You may be able to find a provider that is more accommodating of your situation.

Additionally, if you're coming off a lapse in coverage, you may want to consider reinstating your policy as soon as possible. The longer the gap, the higher the risk you pose to insurance companies, which can result in higher rates. By reinstating your policy promptly, you may be able to mitigate the impact of the coverage gap on your rates.

Finally, it's worth noting that your insurance rates are influenced by a variety of factors, including your age, driving record, location, and the make and model of your vehicle. These factors can change over time, so it's a good idea to review your policy periodically to ensure you're getting the best rate possible.

Food Delivery Auto Insurance: Cost and Coverage

You may want to see also

Frequently asked questions

Collision insurance covers the actual cash value of a vehicle, and cars are becoming increasingly expensive. The cost of collision insurance is also influenced by factors such as your age, gender, driving record, location, and the make and model of your car.

Statistically, younger drivers and males pay higher premiums.

If you have a history of violations on your motor vehicle report, such as a DUI or multiple speeding tickets, your insurance company will consider you more likely to have an accident and increase your rates.

If you live in an area with a high rate of theft, accidents, or weather-related claims, insurance companies may consider it riskier to cover drivers in that area and increase their rates.