Knoxville, Tennessee, has some of the lowest car insurance rates in the state, with an average annual cost of $1,283, which is $46 cheaper than the statewide average. However, insurance costs can vary depending on several factors, including age, gender, marital status, driving record, credit score, and vehicle make and model. For instance, younger drivers tend to pay more than older drivers due to their lack of experience, and a DUI on one's record can significantly increase insurance rates. Additionally, Knoxville's insurance rates are influenced by factors such as traffic congestion, accident rates, the number of uninsured drivers, personal injury lawsuits, and insurance fraud.

| Characteristics | Values |

|---|---|

| Average insurance cost in Knoxville | $1,283 per year or $2,266 per year |

| Average insurance cost in Tennessee | $2,312 per year |

| Average insurance cost in the US | $1,738 per year |

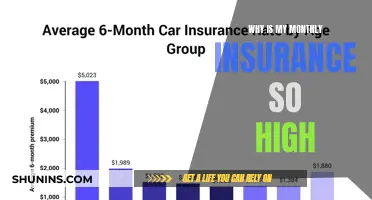

| Average insurance cost in Knoxville for a 20-year-old | $6,800 per year |

| Average insurance cost in Knoxville for a 35-year-old | $2,266 per year |

| Average insurance cost in Knoxville for a 60-year-old | $900 per year |

| Average insurance cost in Knoxville for a male driver | $73 per month |

| Average insurance cost in Knoxville for a female driver | $73 per month |

| Average insurance cost in Knoxville for a driver with a speeding ticket | $103 per month |

| Average insurance cost in Knoxville for a driver with an at-fault accident | $107 per month |

| Average insurance cost in Knoxville for a married policyholder | $11 per month less than unmarried policyholders |

| Average insurance cost in Knoxville for a homeowner | $3 per month less than renters |

| Average insurance cost in Knoxville for a driver with a DUI | $1,900 per year |

| Average insurance cost in Knoxville for a driver with a clean record | $73 per month |

Explore related products

What You'll Learn

![]()

High rate of accidents

Knoxville drivers with a history of at-fault accidents will pay a higher premium. This is because insurance companies view such accidents as a sign of higher risk and potential claims. Drivers in Knoxville with a single accident on their record will pay around $73 a month. The type of accident is also taken into account; an accident caused by running a red light will be treated differently from a minor collision.

Drivers with a DUI on their record will also pay substantially more than a driver without one. This is because insurance companies view DUIs as a major red flag that indicates a higher likelihood of accidents and claims. A DUI conviction will lead to a significant increase in car insurance premiums.

The number of accidents in a particular area can also affect insurance rates. Some parts of a city may have higher rates of accidents, which can lead to an increase in the price you pay.

Age is another factor that influences insurance rates. Younger drivers tend to pay more than older drivers with similar driving histories and credit scores due to having less experience on the road. A higher rate of accidents among younger drivers means they also pay more for car insurance. By the age of 35, car insurance rates should plateau.

Insurance rates have also been increasing steadily over the last four years, with the average auto insurance cost per year in 2024 being 33% higher than in 2021. Inflation is one reason for this increase, as are costlier claims.

Auto Insurance Tracker Devices: Worthwhile or Risky?

You may want to see also

Explore related products

![]()

High-risk drivers

The cost of car insurance in Knoxville, Tennessee, is influenced by various factors, including age, gender, vehicle type, driving record, and credit score. While the average annual cost of car insurance in Knoxville is $1,283, drivers deemed high-risk will typically pay significantly more.

Insurance companies consider several factors when determining whether a driver is high-risk. These factors include a history of accidents, speeding tickets, and DUI convictions. Even a single at-fault accident can increase premiums by 45%. Other high-risk categories include teens, seniors, and people with bad credit.

For high-risk drivers in Knoxville, several insurance companies offer competitive rates and specialised coverage. Dairyland, for instance, specialises in insuring drivers with low credit scores or limited credit history. They also offer non-owner car insurance policies, coverage for motorcycles, and off-road vehicles. First Acceptance Insurance Company also caters to high-risk drivers, offering 18 discounts, including reductions for going paperless and obtaining a quote before a current policy expires. Additionally, they provide flexible monthly payment plans to help drivers secure coverage within their budget.

USAA, available to military personnel, veterans, and their families, offers competitive rates, even for those with at-fault accidents and speeding tickets on their records. Similarly, Erie provides some of the lowest premiums for high-risk drivers with at-fault accidents, and their rate lock feature prevents rates from rising after a claim. Progressive is another insurer with lower rates for drivers with DUIs, offering three tiers of accident forgiveness and coverage options like rideshare insurance.

While these insurers provide alternatives for high-risk drivers in Knoxville, it's important to remember that rates can vary based on individual circumstances. Comparing quotes from different companies can help high-risk drivers find the most suitable coverage for their needs.

Auto Insurance Payment Options: Monthly or Annual Plans?

You may want to see also

Explore related products

![]()

Age demographics

Age is a significant factor in determining the price of car insurance in Knoxville, Tennessee. Generally, the older you are, the less you pay for car insurance. This is because older drivers tend to have more experience on the road and established driving records, so insurers know what to expect and charge accordingly. For instance, younger drivers usually pay more than older drivers with similar driving histories and credit scores.

According to NerdWallet, the average rate for car insurance in Tennessee is $2,312, while in Knoxville it is $2,266. However, this rate can vary depending on where you live in Knoxville, even from one neighbourhood to another. For example, the most populated ZIP codes in Knoxville have an average annual cost of car insurance of $2,266 for a 35-year-old driver with good credit and a clean driving record. By age 35, car insurance rates typically plateau, making it a great time to compare rates as the cheapest insurer in your 20s may no longer be the best deal.

As people age, their insurance rates tend to decrease until they reach retirement age, at which point their rates may start to climb back up. For example, an 18-24-year-old will pay significantly more than a retiree. By age 60, car insurance rates are about as low as they are going to get, provided the driver has a clean record. Most drivers in this age group have a lot of driving experience and established driving records, so insurers know what they are getting into and charge less.

In addition to age, several other factors influence the cost of car insurance in Knoxville. These include gender, vehicle make and model, driving record, credit score, relationship status, and housing status. For instance, female drivers typically pay slightly less than male drivers, and married policyholders often benefit from special discounts, paying about $11 less per month than single policyholders. Renters can also expect to pay around $3 more per month than homeowners, while those living with their parents will see significantly higher rates.

How Commercial Auto Insurance Saves You Money

You may want to see also

Explore related products

![]()

Speeding tickets

The exact amount by which your insurance premium will increase depends on several factors, including your insurance company, driving record, insurance history, and the severity of the speeding violation. For example, speeding between 6 and 10 miles over the speed limit will, on average, cause your insurance rates to increase by $40 per month, or $480 per year. On the other hand, speeding 21-25 mph over the speed limit will result in an average increase of $54 per month or $648 per year.

Insurers consider drivers with speeding tickets to be higher-risk customers, and so are likely to charge them higher rates. However, not all insurers increase their rates by the same amount, and some may not increase them at all. For example, State Farm had the smallest average rate hike after a speeding ticket, at around $22 more per month, while Farmers had the biggest increase among large insurers.

In addition to the financial penalties, speeding tickets can also result in points being added to your license. Accumulating a significant number of points can lead to further penalties, such as having to attend traffic school or even having your license suspended.

If you have received a speeding ticket in Knoxville, it is worth shopping around for a new insurance policy, as different insurers may offer lower rates for drivers with a speeding ticket. You may also be able to lower your insurance rate by participating in a driver safety course accepted by your insurer.

Auto Insurance and Flood Damage: What's Covered?

You may want to see also

Explore related products

![]()

State averages

The average cost of a full-coverage car insurance policy in Knoxville is $1,283 per year, which is $46 cheaper than the statewide average in Tennessee. The average rate in Tennessee is $2,312, while in Knoxville it is $2,266. The cost of auto insurance varies based on where you live, even from one neighbourhood to another. Some parts of a city may have higher accident or theft rates, which can cause an increase in the price you pay.

Tennessee is an at-fault state, which means that in the case of an accident, the driver found at fault will be legally and financially responsible for the damage and injuries resulting from the accident. Knoxville drivers can take advantage of any applicable insurance discounts to save on car insurance costs. The five cheapest car insurance companies in Knoxville, Tennessee, are USAA ($69 per month), State Farm ($71 per month), Auto-Owners Insurance ($81 per month), GEICO ($86 per month), and Nationwide ($99 per month).

Insurance companies consider at-fault accidents as a sign of higher risk and potential claims, so policyholders with accidents on their records will pay a higher premium. Knoxville drivers with a single accident on their record will usually see rates of around $73 a month. Drivers with one ticket on their record will be looking at an average rate of around $66 a month. Accidents, tickets, and other driving infractions can significantly impact your monthly rate. Speeding tickets can also cause insurance costs to increase, as insurance companies view speeding violations as a sign of increased risk, leading to higher premiums. Knoxville drivers with a speeding ticket on their record pay an average of $103 per month for liability coverage.

The number of accidents, the type of roads, and even the weather can affect the rates drivers are charged. Younger drivers tend to pay more than older drivers with similar driving histories and credit scores due to having less experience on the road. A driver with a DUI on their record should expect to pay substantially more than a driver without one. A DUI conviction will cause car insurance rates to increase significantly.

Auto Insurance Down Payment: Split or Save?

You may want to see also