The concept of risk is integral to the insurance industry. Insurance companies evaluate the risk of issuing policies to policyholders to calculate potential future payouts for losses, theft, damage, or injury. This risk assessment process determines the premium charged to the policyholder, with higher risks resulting in higher premiums. Insurers also employ risk management strategies to protect themselves from unexpected losses. Risk, in the context of insurance, refers to the probability of an event occurring that leads to a financial loss. Risks can be dynamic, such as changes in the economy, or pure, where there is only the potential for loss. Understanding and managing risk is essential for insurance companies to operate profitably and provide protection to their customers.

| Characteristics | Values |

|---|---|

| Definition of Risk | The probability that an event could occur that causes a loss. |

| Risk in Insurance | The potential for a loss or adverse event that an insurance company agrees to cover under a policy. |

| Types of Risk | Pure Risk, Dynamic Risk, Speculative Risk, Fundamental Risk, Particular Risk |

| Insurable Risk | Financial Risks, Non-Financial Risks |

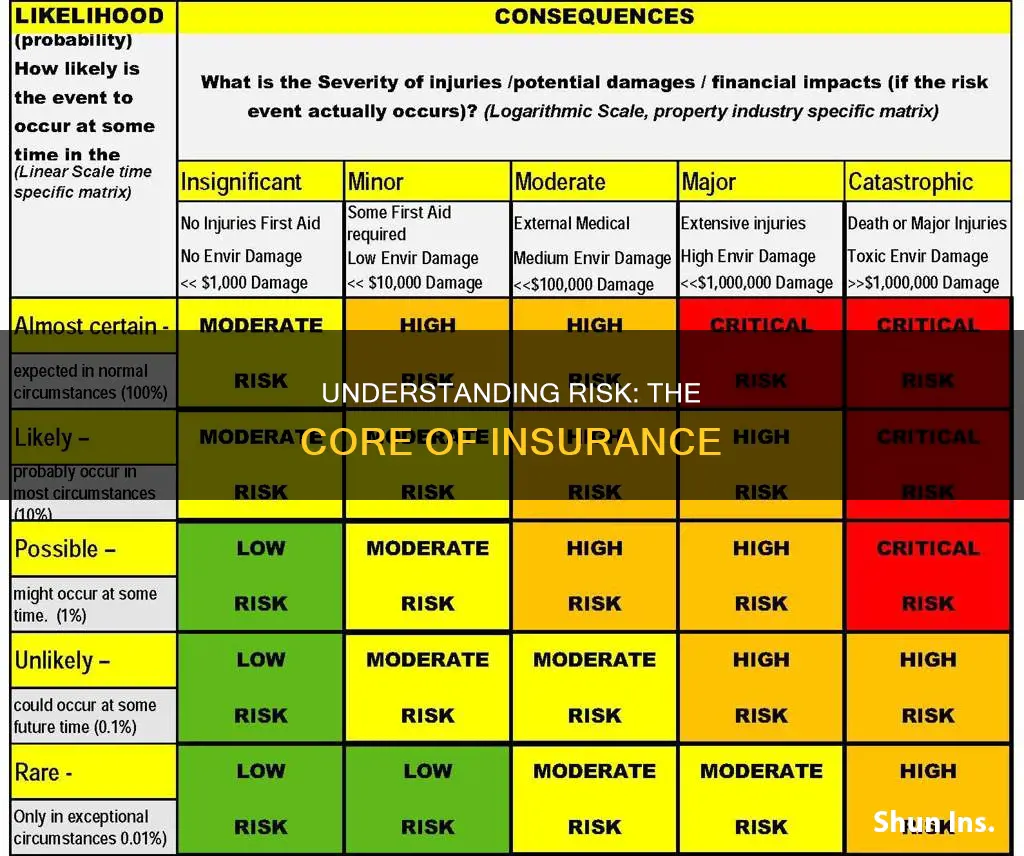

| Risk Assessment Factors | Probability of Occurrence, Severity of Impact, Number of Risks Covered |

| Risk and Premium Calculation | Higher risk = Higher premium |

| Risk Mitigation | Insurance companies and individuals/entities |

| Risk and Insurance Claims | Risk determines whether an insurance claim will be paid out. |

| Risk and Insurance Underwriting | Risk is a primary component of the insurance underwriting process. |

| Risk and Insurance Classes | Risk classes are used to determine coverage and premium costs. |

| Risk Management | Traditional risk management and enterprise risk management (ERM) approaches. |

Explore related products

What You'll Learn

![]()

Risk assessment and management

Risk is a fundamental concept in insurance, and the insurance industry revolves around it. Risk assessment and management are crucial for both insurers and insured entities.

Risk Assessment for Insurers

Insurers assess risk to determine whether to underwrite a policy and calculate the premium to charge. They consider factors such as the likelihood of a claim and the potential payout. For example, a young, healthy individual applying for life insurance is likely to receive lower premiums than an unhealthy, older individual as they are less likely to die, presenting a lower risk of the insurer paying a death claim.

Insurers also assess dynamic risks, which arise from changes in the economy, such as fluctuations in income, tastes, and preferences. These risks are challenging to predict and often lead to financial losses for those in the economy.

Risk Assessment for Insured Entities

Individuals and businesses must assess their risks to make informed decisions about insurance policies. It is essential to consider the type and extent of coverage needed, the reputation and financial stability of the insurer, policy exclusions and limitations, and the premium costs.

Risk Management

Risk management aims to mitigate risks that could harm organizations. Traditional risk management involves buying insurance to protect against losses from events like fire, theft, or cyber liability. However, critics argue that traditional risk management fails to understand risk as an integral part of enterprise strategy.

Enterprise Risk Management (ERM) takes a different approach, viewing risk as a strategic enabler rather than a cost. ERM encourages organizations to embrace the "proper amount of risk needed to grow."

Insurers themselves also engage in risk management. They often have large risk departments headed by Chief Risk Officers (CROs), who focus on brand reputation and understand the horizontal nature of risk.

Historical Context

The concept of insurance has ancient roots, with examples found in Hindu scriptures from the 3rd century BC and ancient Greek maritime loans. The direct insurance of sea-risks for a premium began in Belgium around 1300 AD, and separate insurance contracts were invented in Genoa in the 14th century.

Current Landscape

The insurance industry faces a changing risk landscape, with supply chain shocks, the aftermath of the pandemic, geopolitical risks, and climate change all impacting the industry. Insurers are navigating these challenges, but customer satisfaction has declined due to premium increases and tighter coverage.

Mary Padian: From Storage Wars to Insurance Wars

You may want to see also

Explore related products

![]()

Risk and insurance classes

Risk is a fundamental concept in the insurance industry. It refers to the probability of an event occurring that could lead to a loss. Insurers evaluate the risks associated with issuing insurance policies to determine the likelihood of potential claims. This evaluation process helps them decide whether to offer a policy and calculate the premium to be charged.

Insurable risks, such as financial risks, can be measured and valued monetarily, enabling insurance companies to assess and cover these risks. For example, damage to property or vehicles can be repaired or replaced at a financial cost. On the other hand, non-financial risks, like choosing the wrong career, cannot be valued in monetary terms and are therefore uninsurable.

Pure risk, also known as absolute risk, refers to situations where there is only the potential for loss or, at best, breaking even. This type of risk is insurable. Speculative risk, on the other hand, involves the possibility of either a gain or a loss, such as gambling, and is not insurable.

Dynamic risk arises from changes in the economy, such as fluctuations in income, tastes, and preferences. These risks are challenging to predict and generally not easily insurable.

Insurance risk classes are a way for insurers to categorise individuals or companies with similar characteristics to assess the risk of underwriting a new policy. Riskier groups, such as those with health issues, advanced age, or poor driving records, will generally pay higher premiums. The risk class helps determine the amount of coverage needed and the associated costs.

Underwriters play a crucial role in evaluating risks and determining appropriate coverage terms. They consider various factors, including the type of coverage, the reputation of the insurance provider, policy exclusions, and premium costs.

Individuals can take steps to improve their risk classification and potentially reduce their premium costs. For example, improving health, quitting smoking, or switching to a safer occupation can lead to a lower-risk category and more favourable insurance rates.

Condo Insurance: Commercial vs Private

You may want to see also

Explore related products

![]()

Dynamic risk

The concept of risk is fundamental to the very existence of the insurance industry. Risk, in the context of insurance, refers to the probability of an event occurring that could lead to a loss. This loss could be financial, such as property damage, theft, or injury. Insurers evaluate these risks to determine the likelihood of future claims and calculate premiums accordingly.

Now, dynamic risk refers to the risks that emerge from unpredictable changes in the economy. These changes can be sudden and encompass fluctuations in pricing, income, brand preference, or technology. For instance, the COVID-19 pandemic caused disruptions in supply chains, government lockdown measures, and income losses, impacting various lines of insurance coverage. Dynamic risks are challenging to insure against due to their unpredictable nature.

Additionally, cultural shifts and economic crises can trigger dynamic risks. These shifts can influence consumer behaviour, brand preferences, and purchasing patterns, potentially leading to financial losses for businesses. Dynamic risks are often assessed using planning tools that measure and predict potential risks. However, these assessments can be complex due to the absence of historical data for emerging factors.

In high-risk and dynamic environments, such as construction sites or emergency response situations, dynamic risk assessments are employed to handle unknown risks and maintain control. These assessments involve continuously evaluating and adapting risk management measures to effectively manage risks in a changing environment. Dynamic risk assessments are particularly useful when dealing with rapidly evolving or unpredictable situations, ensuring that exposures are minimized even before a full understanding of all relevant data is attained.

The Mystery of Missed Connections: When Public Adjusters Stand Up Insurance Adjusters

You may want to see also

Explore related products

$9.99 $31.99

![]()

Pure risk

Property risks involve property damage due to uncontrollable forces such as fire, lightning, hurricanes, tornadoes, or hail. For example, an insurance company insuring a policyholder's automobile against theft would bear a loss if the car were stolen. However, if it isn't stolen, the company doesn't make any gain.

Liability risks may involve litigation due to real or perceived injustice. For instance, a person injured after slipping on someone else's icy driveway may sue for medical expenses, lost income, and other associated damages. Pure risk is often insurable because insurers can predict their potential losses using the law of large numbers, a statistical concept that helps them estimate loss figures in advance.

Overall, pure risk is an essential concept in insurance as it allows individuals and businesses to protect themselves financially from potential losses beyond their control. By transferring these risks to insurance companies, they can mitigate the financial impact of adverse events and maintain business continuity.

Understanding Property All-Risk Insurance Coverage

You may want to see also

Explore related products

![]()

Speculative risk

The concept of risk is fundamental to insurance. Risk refers to the probability of an event occurring that leads to a loss. Insurers evaluate this probability to determine whether they may have to pay a claim. This evaluation helps them decide whether to issue an insurance policy and how to calculate the premium.

Switching Insurance: Farmers Commercial Fee-Free?

You may want to see also

Frequently asked questions

Risk is necessary for insurance because it determines the likelihood of an insurer having to pay a claim. This helps the insurer decide whether to issue an insurance policy and how much to charge for it.

Pure risk, also known as absolute risk, is the potential for a loss to occur without the possibility of gain. Speculative risk, on the other hand, involves the chance of either a gain or a loss. For example, betting on a roulette wheel is a form of speculative risk and is not insurable.

Insurance companies use risk classifications to group individuals or companies with similar characteristics. This helps insurers estimate the likelihood of a policyholder filing a claim. Factors such as age, health, driving record, and occupation are considered when determining an insurance risk class.

Yes, individuals can sometimes improve their risk classification and reduce their premium costs. For example, improving one's health or switching to a safer occupation may lead to a lower-risk category. However, some factors, such as chronic health conditions, may be beyond one's control.

Insurance companies often have dedicated risk management departments, typically headed by a Chief Risk Officer (CRO). They employ risk scenario modeling and analysis to quantify and assess financial risks. Additionally, insurers purchase reinsurance to protect themselves against unexpected losses.