USAA homeowners insurance is known for its higher-than-average premiums, leading many to wonder why it is so expensive. USAA's rates are influenced by various factors, including its comprehensive coverage, superior customer service, and location-specific risk assessments. While USAA offers extensive coverage for natural disasters, theft, and other hazards, its premiums tend to be higher in areas with increased risk factors, such as states prone to hurricanes, wildfires, or high crime rates. Additionally, factors such as the age and construction materials of a home can further impact USAA's pricing. Despite the higher costs, USAA is still considered a preferred choice by many homeowners due to its reputation for high standards, excellent customer service, and comprehensive protections.

| Characteristics | Values |

|---|---|

| Higher premiums | Due to comprehensive coverage, superior customer service, and location-specific risk assessments |

| Location | USAA's rates vary state-by-state, zip code by zip code. Rates are higher in riskier states like CA, FL, and WA due to hurricane/wildfire risk. |

| Risk factors | Home age, previous claims, roof age, building materials, etc. |

| Discounts | Bundling insurance policies, installing a security system, and maintaining a good credit score |

| Availability | Only available to military and veterans |

| Ratings | Highly trusted, with 96% of customers saying they trust the company |

| Financial rating | Best possible financial rating from AM Best, an A++ |

| Performance rating | 5 out of 5 stars for overall performance |

Explore related products

What You'll Learn

![]()

USAA's high standards for comprehensive coverage

USAA homeowners insurance is known for its higher-than-average premiums. One of the main reasons for this is the company's commitment to providing comprehensive coverage. USAA has set high standards in the insurance industry, offering an exceptional range of coverages that protect against numerous perils.

USAA's homeowners insurance policies provide a safety net for almost any eventuality. They offer protection against natural disasters, theft, and other hazards. For instance, USAA's dwelling coverage pays to repair or rebuild the structure of your home if it is damaged or destroyed. Their other structures coverage includes damage to unattached buildings such as sheds or fences. Personal property coverage pays to repair or replace personal belongings, such as furniture or clothing, and loss-of-use coverage pays for additional living expenses if you have to live elsewhere while your home is being repaired.

USAA also offers several optional coverages and riders, such as earthquake insurance, coverage for high-value items, and identity theft coverage. While these add-ons provide valuable additional protection, they can also increase the overall cost of the insurance policy.

The company's high standards for comprehensive coverage also extend to its commitment to serving high-risk areas. USAA provides insurance in areas that other companies have pulled out of due to high risk, such as California and Florida, which are prone to hurricanes and wildfires. By continuing to offer insurance in these areas, USAA assumes more risk, which is reflected in its higher premiums.

In addition to its comprehensive coverage, USAA is also known for its superior customer service and responsive agents. Their efficient claims process ensures a seamless experience for policyholders, contributing to higher customer satisfaction but also to higher premiums.

While USAA's homeowners insurance may be more expensive than some other providers, it is important to note that the company offers various discounts and savings opportunities to offset the costs. These include bundling insurance policies, installing a security system, and maintaining a good credit score.

Overall, USAA's high standards for comprehensive coverage, exceptional customer service, and commitment to serving high-risk areas contribute to its higher premiums. However, for many homeowners, the peace of mind offered by USAA's extensive coverage options is well worth the investment.

Mortgage Insurance: Can You Negotiate a Lower Rate?

You may want to see also

Explore related products

![]()

Superior customer service

USAA homeowners insurance is known for its higher-than-average premiums, which can be attributed to various factors, including superior customer service. Here are some key points highlighting how superior customer service contributes to higher costs:

Responsive Agents and Efficient Claims Process

USAA is renowned for its exceptional customer service, employing responsive agents who provide efficient claims processing. This level of service naturally contributes to higher operational costs, which are reflected in the premiums charged to policyholders. The company prioritises a seamless experience for its customers, ensuring that any issues or claims are handled promptly and effectively.

Comprehensive Coverage and Risk Assessment

USAA offers an extensive range of coverages that surpass the standard offerings of many other insurance companies. Their policies are designed to provide a safety net for almost any eventuality, including natural disasters, theft, and other hazards. This comprehensive coverage comes at a cost, as USAA assumes a greater financial burden by insuring against a wider range of risks.

Location-Specific Risk Factors

USAA considers location-specific risk factors when determining premiums. Homes located in areas prone to natural disasters, such as hurricanes, wildfires, or floods, or regions with high crime rates, typically face higher premiums. While this is a standard practice across the insurance industry, USAA's comprehensive coverages can make their policies even more expensive in these high-risk areas.

Optional Coverages and Add-ons

USAA offers a variety of optional coverages and riders, such as earthquake insurance, coverage for high-value items, and identity theft protection. While these additional protections provide enhanced peace of mind, they come at an extra cost. Policyholders can customise their coverage by selecting relevant add-ons, but this flexibility contributes to the overall higher cost of USAA homeowners insurance.

Customer Satisfaction and Trust

USAA has earned a reputation for providing superior customer service, resulting in high levels of customer satisfaction and trust. According to surveys, 96% of customers trust the company, and many homeowners find the peace of mind offered by USAA worth the investment, even with the higher premiums. This loyalty and satisfaction are, in part, a reflection of the company's commitment to delivering exceptional service.

In summary, the superior customer service offered by USAA homeowners insurance is a significant contributing factor to its higher premiums. The company's dedication to responsiveness, efficiency, comprehensive coverage, and customer satisfaction results in increased operational costs, which are passed on to policyholders in the form of higher premiums. While the costs may be higher, many customers find the level of service and protection provided by USAA to be well worth the expense.

GEICO: Florida Home Insurance Options

You may want to see also

Explore related products

![]()

Location-specific risk factors

USAA homeowners insurance is known for its higher cost, which can be attributed to various factors, including location-specific risk factors. Here is an overview of how location-specific risk factors impact the cost of USAA homeowners insurance:

The location of a home is a significant factor in determining the pricing of USAA homeowners insurance. USAA considers location-based risks, such as the likelihood of natural disasters or high crime rates, when setting premiums. Areas prone to hurricanes, wildfires, or other natural disasters typically face higher insurance rates. For example, USAA has increased rates in California due to the state's wildfire risks and the challenges posed by climate change and economic inflation. Similarly, in states like Florida, where the risk of hurricanes is high, insurance rates tend to be higher.

The age of a home and the materials used in its construction can also impact insurance rates. Older homes, particularly those built before 1940, may be considered higher risk and result in higher premiums. Additionally, if a home is constructed with expensive materials, the cost of insurance may increase to reflect the potential expense of repairs or replacements.

USAA's commitment to providing comprehensive coverage, even in high-risk areas, has made it a preferred choice for homeowners seeking top-tier insurance protection. However, this commitment to offering extensive coverage in risk-prone locations contributes to the higher premiums associated with USAA homeowners insurance.

It is worth noting that USAA's rates may vary from state to state and even between different zip codes within a state. This variation in pricing reflects USAA's assessment of location-specific risks and their commitment to providing appropriate coverage based on those risks.

While location plays a significant role in determining insurance rates, it is not the sole factor. Other considerations, such as the age of the home, the presence of security systems, and personal factors like credit score, can also impact the cost of USAA homeowners insurance.

In conclusion, USAA homeowners insurance rates are influenced by location-specific risk factors, including the likelihood of natural disasters, crime rates, and the unique characteristics of the property's location. This results in higher premiums for homeowners in areas that USAA considers higher risk.

LifeLock Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

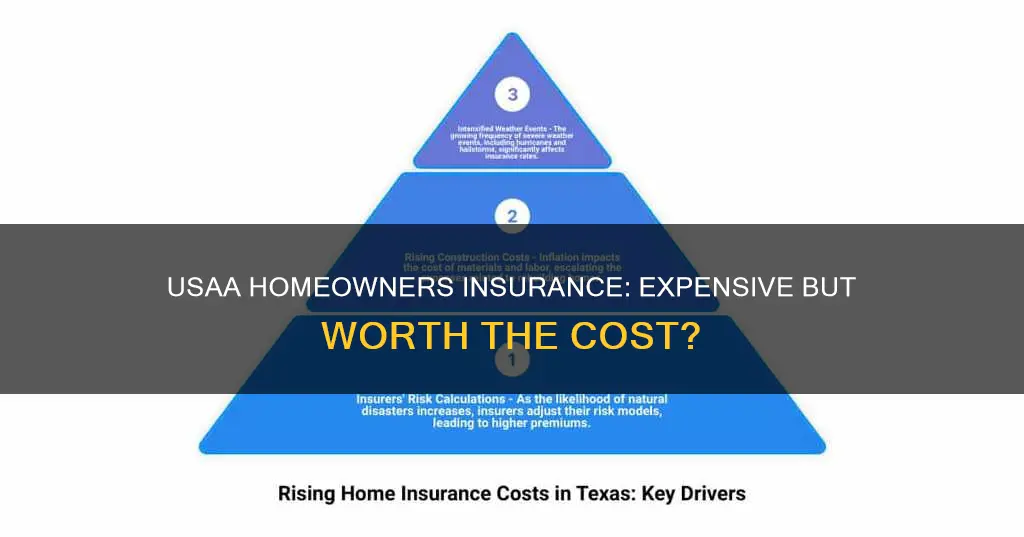

Inflation and increased claim costs

Inflation has impacted the cost of materials and labour, leading to higher expenses for insurance companies when paying out claims. As a result, insurance companies, including USAA, have raised their rates to offset these increased claim costs.

Additionally, USAA's rates in California specifically have been affected by rising costs associated with economic inflation, climate change, and wildfire risks. California's insurance market has faced challenges due to these factors, and USAA's direct premiums written in the state increased significantly from $523.1 million in 2019 to $741.7 million in 2023.

While USAA's rates have increased, they still offer competitive pricing for military members, veterans, and their families. USAA provides reasonable rates, low consumer complaints, and generous coverage, making it a preferred choice for those who qualify. Their rates are generally lower than the national average, and they include additional coverages that often cost extra with other insurance companies.

Navigating the Farm: A Guide to Purchasing Farmers Insurance

You may want to see also

Explore related products

![]()

Home age and location

The age and location of a home are key factors in determining the cost of homeowners insurance. In general, older homes tend to be more expensive to insure than newer ones. This is because older homes may have outdated or deteriorating features that increase the risk of damage or loss. For example, older electrical systems may not be able to handle the demands of modern appliances and may be more prone to electrical fires. Similarly, older plumbing systems may be more susceptible to leaks or water damage. Additionally, older homes may not have been built to modern building codes, which could make them less able to withstand natural disasters such as hurricanes, earthquakes, or floods.

When it comes to location, insurance companies will consider the specific risks associated with the area where the home is situated. Homes located in areas prone to natural disasters, such as hurricanes, earthquakes, or floods, will typically have higher insurance rates. For example, if your home is located in a flood zone, you may be required to purchase additional flood insurance to protect against water damage. Similarly, homes in areas with a high crime rate may also see higher insurance costs due to an increased risk of theft, vandalism, or burglary.

Another factor related to location is the distance of the home from emergency services. If your home is in a remote area, far from fire stations or police departments, it may take longer for emergency services to respond to an incident, which could result in more extensive damage. As a result, insurance companies may charge a higher rate to compensate for the increased risk. Additionally, the availability of local fire hydrants and the quality of the local fire department's equipment can also impact insurance costs. Areas with well-maintained fire hydrants and up-to-date firefighting equipment may receive more favourable insurance rates.

The replacement cost of a home is another critical factor considered by insurance companies. This takes into account the cost of rebuilding the home in its entirety, should it be completely destroyed. Older homes may have unique architectural features or use specific construction materials that are more expensive to replace or replicate, driving up the overall replacement cost. Additionally, if the home has historical significance, the cost of rebuilding it to its original specifications could be significantly higher, impacting the insurance premium.

It's important to note that insurance companies may also take into account the condition and maintenance of the home, especially for older properties. Regular maintenance and timely updates to critical systems such as plumbing, electrical, and roofing can help mitigate some of the risks associated with older homes. By investing in preventative measures and keeping the home well-maintained, homeowners may be able to secure more favourable insurance rates, even for older properties. Routine inspections and providing documentation of maintenance and repairs can help demonstrate the condition of the home and potentially lower insurance costs.

Mortgage Payment Protection Insurance: What You Need to Know

You may want to see also

Frequently asked questions

USAA homeowners insurance is expensive due to its comprehensive coverage, superior customer service, and location-specific risk assessment. USAA offers various discounts and savings opportunities to help offset costs, but the overall cost remains higher compared to some other insurers.

The location of a home plays a significant role in the pricing of USAA homeowners insurance. Areas prone to natural disasters or with high crime rates typically face higher premiums. Other factors include the age of the home, whether it was built before 1940, if the roof is old, and if the home is made with expensive materials.

USAA's home insurance rates are increasing due to increased claim costs and inflation. Inflation has made it more expensive to repair or rebuild houses, which means insurance premiums have increased.

USAA homeowners insurance is highly rated and offers reasonable rates, low consumer complaints, and generous coverage. While it is not the cheapest option, many homeowners find the peace of mind offered by USAA to be worth the investment.