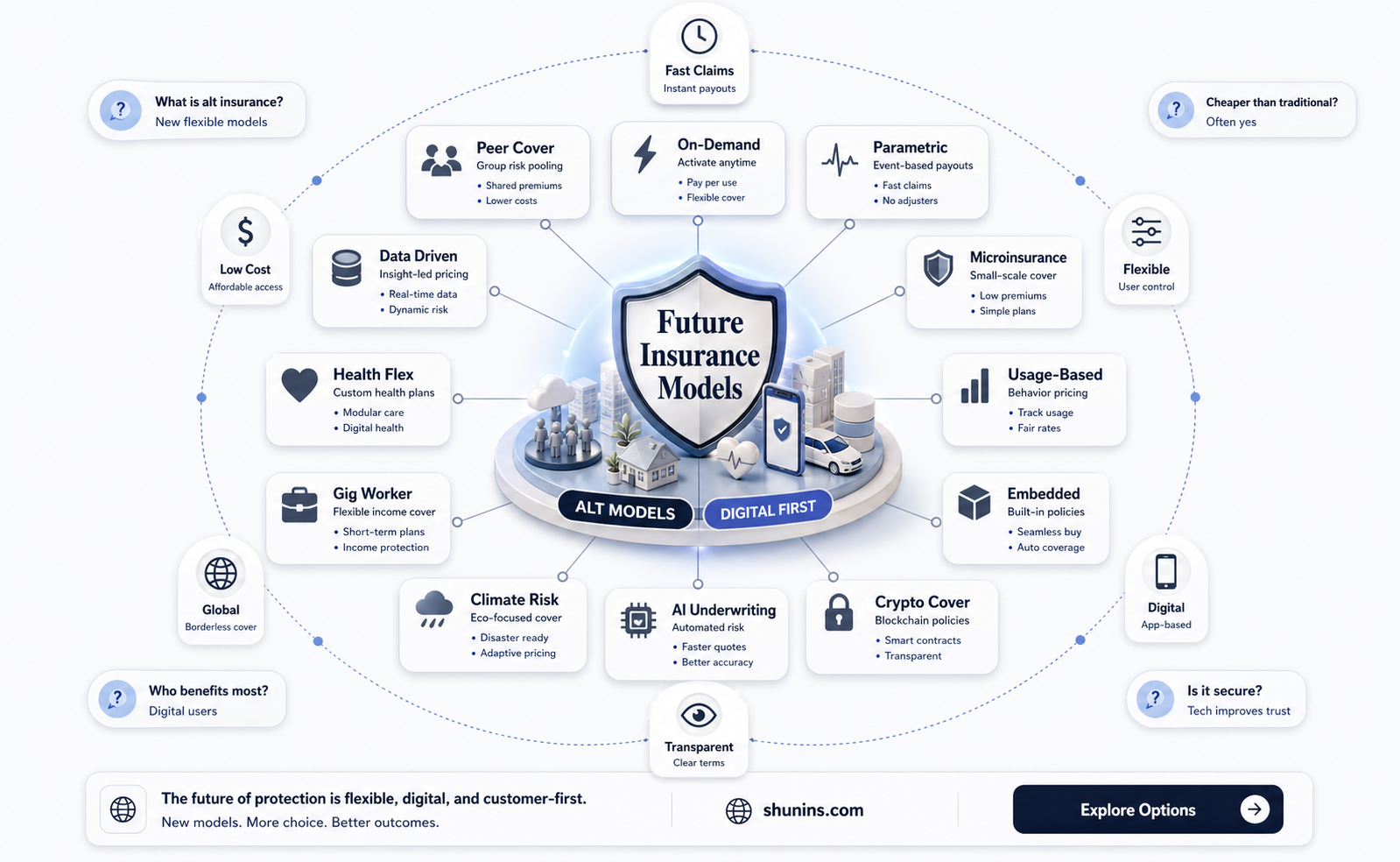

There are a variety of alternative insurance options available for individuals and businesses. For individuals, alternatives to traditional health insurance include cost-sharing programs, indemnity insurance, and health care membership services. These options can provide more affordable and flexible alternatives to traditional insurance plans. For businesses, alternative insurance options include self-insurance, captive insurance, and risk retention groups. These alternatives can help small businesses manage their protection needs and reduce costs. Additionally, some alternative coverage arrangements, such as general liability insurance, may be suitable for specific situations, such as students who are not eligible for standard coverage.

| Characteristics | Values |

|---|---|

| Company Name | American Alternative Insurance Corporation |

| Location | Princeton, New Jersey, US |

| Services | Automobile, agricultural, ocean marine, surety, general liability, and political risk insurance |

| Other Services | Workers' compensation and professional liability insurance |

| Contact Number | +1 800-544-2378 or +1 908-572-0841 |

| [email protected] | |

| Website | www.americanalternativeinsurancecorporation.com |

| Alternative Company Name | Alternative Balance |

| Focus | Fitness, Beauty, and Wellness Insurance |

| Testimonial | "Alternative Balance has been amazing at helping me get the best coverage for my business!" |

| App | Ambetter Health App |

Explore related products

What You'll Learn

![]()

Self-insurance

For individuals, self-insurance is generally uncommon due to the rarity of having sufficient funds to cover large uncertain risks and achieving significant cost savings on premiums to justify taking on the risk. Most individuals prefer to transfer the risk to an insurer rather than self-insure, especially for catastrophic risks with high loss values that are typically underwritten by the reinsurance or wholesale insurance market. Examples of such risks include earthquakes, which cannot be fully insured against due to the potential for damage exceeding the total assets of the insurer or the combined insurance market.

However, individuals may unintentionally engage in self-insurance by opting for higher deductibles or declining extended warranties. A deductible is the amount of risk an individual is comfortable paying out of pocket, and by choosing a higher deductible, they essentially self-insure for that amount. Similarly, when individuals reject extended warranties, they assume the risk of covering the cost of adverse events themselves.

Organizations may choose to self-insure for certain risks, particularly those that are predictable and measurable. Employee benefits insurance is a popular form of self-insurance for corporations with a large number of employees. By forming captive insurance companies, corporations can predict and price the risk of losses from employee benefits, thereby managing their financial exposure without purchasing commercial insurance. Organizations that self-insure set aside money based on actuarial and insurance information to ensure sufficient funds to cover future uncertain losses.

Full or exclusive self-insurance is rare among organizations, with most combining self-insurance and commercial insurance. Typically, the organization retains and self-insures the predictable losses, creating a "working layer" of cover, and purchases a stop-loss or stop-gap policy from the commercial insurance market for losses exceeding the specified self-insurance limit. This hybrid approach allows organizations to balance their risk exposure and cost savings.

How Do Medical Insurance Advocates Get Paid?

You may want to see also

Explore related products

![]()

Health discount cards

With healthcare premiums on the rise, many Americans are searching for more affordable health insurance. This has led to an increase in discount health plans being marketed. It is important to know the difference between health insurance and discount health cards, and to be able to distinguish between legitimate and fraudulent cards.

Discount health cards are not insurance. Legitimate discount health cards offer discounts on services from doctors, pharmacists, etc., who accept these cards. Buyers should be aware that because discount cards are not insurance, fewer consumer protections exist for buyers. Many state insurance departments do not regulate the entities that sell discount health cards, although some insurance departments have recently enacted legislation to allow regulation, including licensing or registration requirements. Some insurance carriers offer discount cards at little or no cost as an added value to their members.

Prescription discount cards have become more popular as patients seek out ways to afford the medication they need. They are free to obtain and deliver significant discounts on commonly prescribed medications. They allow you to compare pharmacies for the best price and are accepted by a large network of pharmacies. GoodRx, for example, offers a free prescription savings card that can be used for discounts of up to 83% on most prescription drugs at over 70,000 U.S. pharmacies. Optum Perks offers prescription drug savings of up to 80% at more than 64,000 pharmacies nationwide.

It is important to be cautious when purchasing a discount health card. Avoid companies that insist on debit or credit card information and may pressure you to make quick decisions. Legitimate discount card issuers will never suggest you drop your health insurance. Check with your state insurance department for more information on the differences between discount health cards and health insurance.

Life Insurance: Medication's Impact on Eligibility

You may want to see also

Explore related products

![]()

Cost-sharing programs

Medical cost-sharing programs, also known as healthcare sharing plans, healthcare sharing ministries, or health-sharing plans, are communal models where group members pool their money to pay for everyone's approved medical costs. These programs are typically run by nonprofit organizations and are not the same as health insurance plans or premiums. They are also not subject to the same consumer protections as health insurance.

Members of these programs pay a set monthly amount into a group fund, which is used to cover everyone's approved healthcare costs. When a member receives a large medical bill, they can request to use the collective funds to cover some or all of their charges. Many programs encourage members to seek low-cost healthcare or charity care before requesting a payout.

The monthly payments for these programs are typically lower than health insurance plans, and members can often choose their healthcare providers. However, there are financial risks associated with medical cost-sharing programs, and members can end up with unpaid bills and medical debt. Additionally, traditional health insurance typically provides broader coverage, including preventive care and maternity services, which may not be fully covered by a health-sharing plan.

Some popular health-sharing programs include Liberty HealthShare, Medi-Share, Samaritan Ministries, and Zion HealthShare. These programs offer flexibility, a sense of community, and reduced overall healthcare costs.

Life Insurance with Diabetes: Getting a Mortgage

You may want to see also

Explore related products

![]()

Primary care memberships

However, primary care memberships won't help if you need surgery, hospitalization, or a specialist. They are not considered insurance, so they're not regulated like traditional policies. That means what's covered under one membership may not be covered under another. For example, some memberships may include annual check-ups, sick visits, and prescriptions, while others may not.

Some people combine primary care memberships with a high-deductible, low-premium health plan to cover more serious medical issues. One example of a primary care membership is Amazon One Medical, which offers on-demand virtual care through the One Medical app, as well as in-person appointments for a membership fee of $9/month or $99/year with Prime.

Valuation in Life Insurance: Why It's Essential

You may want to see also

Explore related products

![]()

Higher deductibles

A High-Deductible Health Plan (HDHP) is a health insurance plan that offers lower monthly premiums and a higher deductible. This means that you will pay less every month for your plan, but you will have to pay more out of pocket for your medical expenses before your insurance provider starts contributing.

For example, if your deductible is $2,000, you will have to pay the first $2,000 of covered services yourself. This amount is separate from your monthly premium and is paid directly to your healthcare provider. After you have paid the deductible, your insurance provider will start contributing to your healthcare costs.

HDHPs are a good fit for those who are generally healthy and rarely need to go to the doctor beyond annual check-ups or preventive care. This is because the lower monthly premiums offered by HDHPs are offset by the higher upfront costs that you will have to pay if you require medical care. If you have a chronic health condition that requires regular visits to your primary care provider or specialists, you may incur significant out-of-pocket expenses that could be difficult to manage.

However, it is important to carefully consider your own situation when deciding on an HDHP. If you have young children or take several medications, your upfront costs may be higher. Additionally, you must be prepared to pay your full deductible upfront in case of an emergency. To help with these costs, some HDHPs can be paired with a Health Savings Account (HSA), which allows you to set aside money on a pre-tax basis to pay for qualified medical expenses.

Insurance Adjusters: Are They Lawyers in Disguise?

You may want to see also

Frequently asked questions

Alternative insurance refers to risk funding techniques or facilities that provide coverages or services outside the realm of traditional property-casualty (P&C) insurers. It is often sought by those who cannot afford traditional insurance plans.

Some examples of alternative insurance include self-insurance, captive insurance, and general liability insurance. Cost-sharing programs are another example, where participants pay a pre-set monthly contribution that covers the medical bills of other members.

Alternative insurance plans can be cheaper than traditional insurance plans and may allow for more customization and flexibility in choosing one's doctor.