AM Best health insurance ratings are a critical tool for consumers and businesses seeking reliable and financially stable insurance providers. These ratings, provided by A.M. Best, a globally recognized credit rating agency, evaluate the financial strength and creditworthiness of insurance companies, ensuring policyholders that their chosen insurer can meet its financial obligations, such as paying claims. The ratings are based on a comprehensive analysis of an insurer’s balance sheet, operating performance, business profile, and enterprise risk management. For health insurance, these ratings are particularly important as they provide assurance that the company can handle long-term healthcare costs and claims efficiently. Understanding AM Best ratings helps individuals and employers make informed decisions when selecting health insurance plans, ensuring both financial security and peace of mind.

Explore related products

What You'll Learn

- Rating Criteria Overview: Key factors AM Best uses to evaluate health insurers' financial strength

- Rating Scale Explained: Understanding AM Best’s rating scale from A++ (Superior) to D (Poor)

- Financial Stability Indicators: Metrics like capital adequacy, operating performance, and liquidity assessed by AM Best

- Rating Updates Frequency: How often AM Best revises health insurance company ratings

- Impact on Policyholders: How AM Best ratings influence consumer trust and insurer reliability

![]()

Rating Criteria Overview: Key factors AM Best uses to evaluate health insurers' financial strength

AM Best, a leading credit rating agency, employs a rigorous framework to assess the financial strength of health insurers, ensuring policyholders and stakeholders can make informed decisions. Their rating criteria delve into a multitude of factors, each offering a unique lens into an insurer's stability and reliability. Here's an overview of the key elements that shape these critical evaluations.

Financial Performance and Stability: At the heart of AM Best's assessment lies a comprehensive analysis of an insurer's financial statements. This involves scrutinizing revenue growth, profitability trends, and expense management. For instance, a consistent increase in premium income coupled with controlled administrative costs can signify a robust financial position. AM Best also examines an insurer's ability to manage claims, as efficient claims handling directly impacts profitability. A key metric here is the loss ratio, which compares incurred losses to earned premiums, providing insight into an insurer's underwriting discipline.

Risk Management and Capital Adequacy: Evaluating an insurer's risk management practices is crucial. AM Best assesses how companies identify, measure, and mitigate risks, including investment, underwriting, and operational risks. This includes analyzing the diversity and quality of an insurer's investment portfolio, as well as their ability to manage market volatility. Capital adequacy is another critical aspect, ensuring insurers have sufficient capital to absorb losses and maintain operations during adverse events. AM Best's criteria consider the quality and availability of capital, with a focus on surplus levels and the ability to generate capital organically.

Operational Efficiency and Market Position: The efficiency of an insurer's operations is a significant indicator of long-term sustainability. AM Best examines factors such as expense ratios, operational scalability, and the effectiveness of cost-control measures. Insurers with streamlined processes and innovative technologies often demonstrate better operational efficiency. Additionally, market position and competitive advantage play a role. This includes assessing market share, brand reputation, and the ability to attract and retain customers, all of which contribute to an insurer's overall financial strength.

Enterprise Risk Management (ERM) and Strategic Planning: AM Best recognizes the importance of a holistic approach to risk management. They evaluate insurers' ERM frameworks, which encompass identifying and managing risks across the entire organization. This includes strategic risks, such as those associated with business model changes or regulatory shifts. Insurers with robust ERM practices and well-defined strategic plans are better equipped to navigate industry challenges. AM Best's criteria encourage insurers to adopt a forward-looking perspective, ensuring they are prepared for emerging risks and market dynamics.

In summary, AM Best's rating criteria provide a comprehensive evaluation of health insurers' financial health, offering insights into their stability, risk management, and operational prowess. By considering these factors, policyholders and industry professionals can make informed choices, ensuring they partner with financially secure and reliable insurers. This detailed assessment process is a cornerstone of the insurance industry's credibility and transparency.

Navigating Depression Medication: Accessing Treatment Without Insurance

You may want to see also

Explore related products

![]()

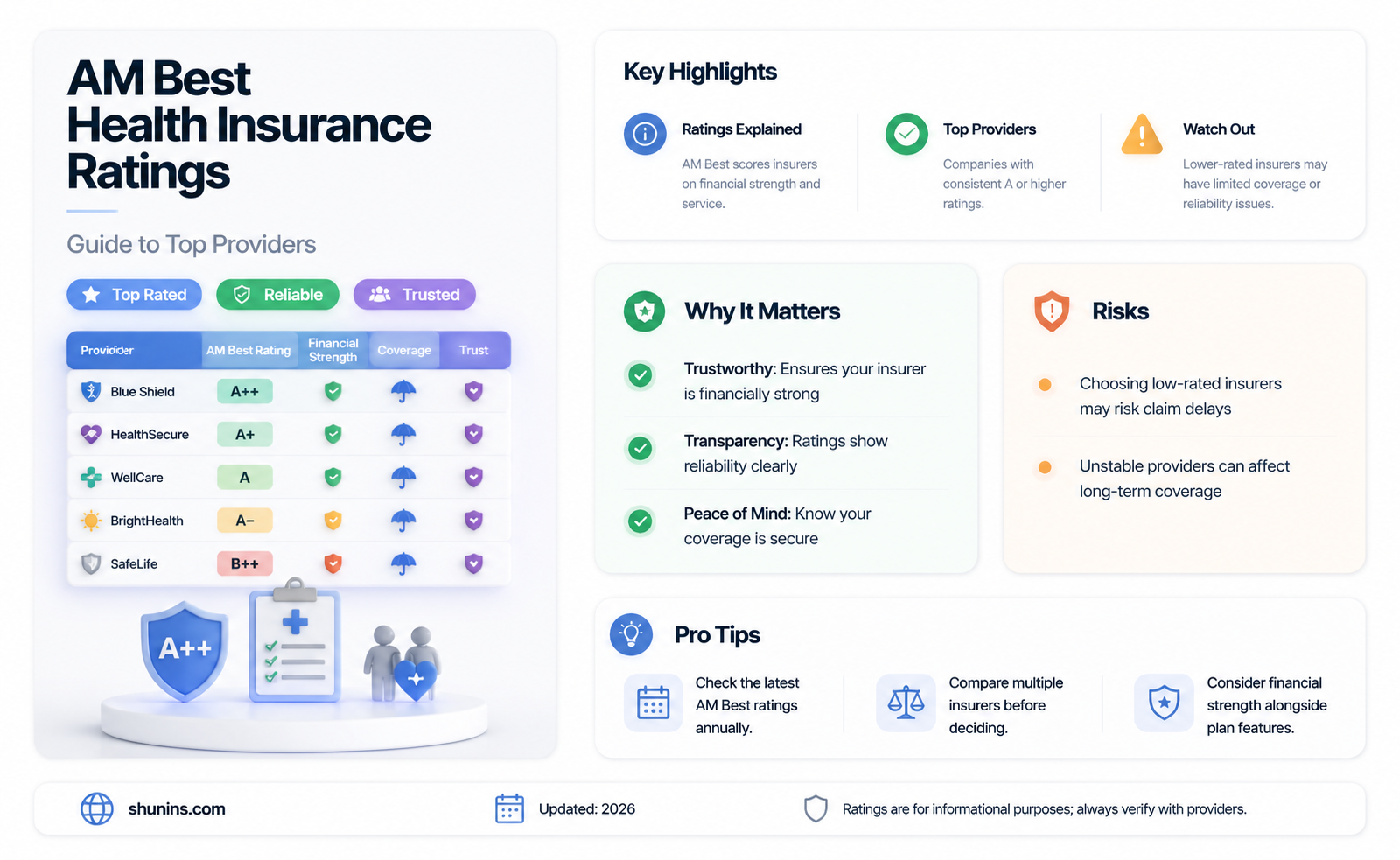

Rating Scale Explained: Understanding AM Best’s rating scale from A++ (Superior) to D (Poor)

AM Best’s rating scale is a cornerstone for evaluating the financial strength and creditworthiness of insurance companies, including health insurers. Ranging from A++ (Superior) to D (Poor), this scale provides a clear, standardized measure of an insurer’s ability to meet its ongoing obligations. Understanding this scale is critical for consumers and businesses alike, as it directly impacts the reliability of coverage and claims processing. Each rating reflects a comprehensive analysis of factors such as balance sheet strength, operating performance, and enterprise risk management.

At the top of the scale, A++ (Superior) and A+ (Superior) ratings signify the highest levels of financial stability. Insurers in this tier are deemed capable of withstanding adverse economic conditions and maintaining consistent performance. For health insurance, this means policyholders can trust that their claims will be paid promptly, even during periods of financial stress. Companies like UnitedHealth Group and Kaiser Foundation have historically maintained ratings in this range, reflecting their robust financial health. If your insurer holds an A++ or A+ rating, you can proceed with confidence, knowing your coverage is backed by a financially secure entity.

Moving down the scale, ratings from A (Excellent) to B++ (Good) still indicate strong financial health but with varying degrees of risk. A-rated insurers, such as Anthem and Aetna, are considered excellent but may face slightly more challenges in adverse conditions. B++-rated companies are good but may exhibit vulnerabilities in their financial structure or operational efficiency. Policyholders with insurers in these tiers should monitor industry trends and company performance to ensure continued stability. While these ratings are still reliable, they warrant occasional reassessment to avoid surprises.

Ratings below B+ (Good) signal increasing financial risk. B (Fair) and B- (Fair) ratings suggest an insurer may struggle to meet obligations during economic downturns, while C++ (Marginal) and C+ (Marginal) indicate significant financial weaknesses. Health insurance policyholders with insurers in these categories should consider alternatives, as the risk of delayed or denied claims rises sharply. A D (Poor) rating is a red flag, indicating the insurer is nearing or already in financial distress. Policyholders with D-rated insurers should immediately seek coverage elsewhere to protect their health and financial well-being.

To make informed decisions, consumers should regularly check AM Best’s ratings, especially before purchasing or renewing health insurance policies. These ratings are updated periodically, reflecting changes in an insurer’s financial health. Practical tips include comparing ratings across multiple insurers, reviewing the rating rationale provided by AM Best, and consulting with insurance brokers who specialize in financially stable providers. By understanding and leveraging AM Best’s rating scale, you can ensure your health insurance coverage remains reliable and secure, even in uncertain times.

When Are Medical Insurance Premiums Due?

You may want to see also

Explore related products

![]()

Financial Stability Indicators: Metrics like capital adequacy, operating performance, and liquidity assessed by AM Best

AM Best’s assessment of financial stability in health insurance companies hinges on three critical metrics: capital adequacy, operating performance, and liquidity. Capital adequacy measures an insurer’s ability to absorb losses while meeting policyholder obligations. AM Best evaluates this through the risk-adjusted capitalization model, which considers asset quality, business profile, and risk management practices. For instance, a company with a capital adequacy ratio above 150% is often viewed as financially secure, whereas ratios below 100% may signal vulnerability. This metric is particularly vital in health insurance, where claims can fluctuate unpredictably due to pandemics, medical inflation, or policy changes.

Operating performance, the second pillar, reflects an insurer’s efficiency in generating profits from core activities. AM Best scrutinizes metrics like underwriting margins, expense ratios, and investment returns. A combined ratio (claims and expenses divided by premiums) below 100% indicates profitability, while consistent losses may raise red flags. For example, a health insurer with a combined ratio of 95% and a 5% investment yield demonstrates robust operational health. However, companies relying heavily on investment income rather than underwriting profits may face risks during economic downturns, making this metric a key differentiator in AM Best’s ratings.

Liquidity, the third indicator, assesses an insurer’s ability to meet short-term obligations without compromising long-term stability. AM Best examines cash flow, marketable securities, and access to capital markets. Health insurers must maintain sufficient liquid assets to cover claims, especially in high-volume periods like flu seasons or post-disaster scenarios. A liquidity ratio (current assets to current liabilities) of 1.5 or higher is generally favorable. Insurers with diversified funding sources, such as reinsurance agreements or credit facilities, often fare better in AM Best’s evaluations, as they demonstrate resilience in adverse conditions.

Practical takeaways for consumers and stakeholders include focusing on these metrics when comparing health insurance providers. A company with strong capital adequacy, consistent operating profits, and robust liquidity is better positioned to honor claims and withstand market volatility. AM Best’s ratings, often denoted by letter grades (A++ to D), provide a snapshot of these indicators. For instance, an A+ rating signifies superior financial strength, while a B- rating indicates marginal stability. By understanding these metrics, policyholders can make informed decisions, ensuring their insurer’s financial health aligns with their long-term needs.

Understanding Your Medical Insurance Premium: Cost Breakdown

You may want to see also

Explore related products

![]()

Rating Updates Frequency: How often AM Best revises health insurance company ratings

AM Best, a leading credit rating agency, typically revises health insurance company ratings on an annual basis, though this frequency can vary depending on market conditions, regulatory changes, or significant events affecting the industry. This annual review ensures that ratings remain current and reflective of a company’s financial strength, operating performance, and ability to meet policyholder obligations. For consumers and stakeholders, this regularity provides a reliable benchmark for assessing insurer stability and reliability.

However, AM Best reserves the right to conduct off-cycle rating updates in response to material changes within a company or the broader market. Such triggers include mergers and acquisitions, leadership shifts, regulatory interventions, or financial distress. For instance, if a health insurer reports a substantial loss or undergoes a significant restructuring, AM Best may issue an updated rating outside the standard annual cycle. This flexibility ensures that ratings remain dynamic and responsive to real-time developments.

The frequency of updates is also influenced by the insurer’s size, market position, and risk profile. Larger, more complex organizations with diverse product lines may warrant closer monitoring, potentially leading to more frequent reviews. Conversely, smaller, stable insurers with consistent performance may adhere more strictly to the annual update schedule. Understanding these nuances helps stakeholders interpret rating changes in context rather than viewing them as isolated events.

For practical application, consumers should monitor AM Best’s rating announcements, especially during periods of industry volatility. Subscribing to alerts or regularly checking the agency’s website can provide timely updates on insurers’ financial health. Additionally, advisors and brokers should educate clients on the significance of rating changes and their potential impact on policy decisions. By staying informed, individuals can make proactive adjustments to their coverage, ensuring alignment with their risk tolerance and financial goals.

In conclusion, while AM Best’s health insurance ratings are primarily updated annually, the agency’s adaptive approach ensures responsiveness to critical industry shifts. This balance between consistency and flexibility underscores the credibility of their ratings, making them an indispensable tool for evaluating insurer reliability. Stakeholders who understand this update frequency can better leverage AM Best’s insights to navigate the complexities of health insurance markets.

Medical Tourism Insurance: Understanding the Cost and Coverage

You may want to see also

Explore related products

$23.16 $28.95

$42.36 $57.95

![]()

Impact on Policyholders: How AM Best ratings influence consumer trust and insurer reliability

AM Best ratings serve as a financial compass for policyholders, offering a clear indication of an insurer’s ability to meet its obligations. These ratings, ranging from A++ (Superior) to D (Poor), provide a snapshot of an insurer’s financial strength, stability, and reliability. For consumers, this translates into confidence—knowing that their claims will be paid promptly, even in the aftermath of catastrophic events. For instance, a policyholder with a health insurance plan from an A+-rated insurer can rest assured that the company has a strong balance sheet and robust risk management practices, reducing the likelihood of financial distress.

Consider the practical implications for a 45-year-old individual shopping for health insurance. With rising healthcare costs and increasing premiums, this consumer is not just looking for coverage but also for long-term reliability. An AM Best rating of A or higher signals that the insurer is financially secure, capable of handling claims efficiently, and less likely to increase premiums unpredictably. Conversely, a lower rating might prompt the consumer to weigh the risks of potential claim denials or delayed payouts against the allure of lower premiums. This decision-making process underscores how AM Best ratings directly influence consumer behavior and trust.

From a persuasive standpoint, AM Best ratings act as a seal of approval, encouraging policyholders to prioritize financial stability over short-term savings. For example, a family with a history of chronic illnesses might opt for a slightly more expensive plan from a highly rated insurer rather than risk inadequate coverage from a lower-rated provider. The peace of mind that comes with knowing an insurer is financially sound often justifies the additional cost. Insurers, aware of this consumer mindset, strive to maintain or improve their ratings, fostering a competitive environment that benefits policyholders through better service and reliability.

Comparatively, the impact of AM Best ratings on consumer trust can be likened to credit scores in personal finance. Just as a high credit score opens doors to better loan terms, a high AM Best rating enhances an insurer’s credibility and attracts risk-averse consumers. However, unlike credit scores, which are private, AM Best ratings are publicly available, making them a transparent tool for comparison. This transparency empowers policyholders to make informed decisions, ensuring they align with insurers that match their risk tolerance and financial expectations.

In conclusion, AM Best ratings are more than just alphabetical grades—they are a critical factor in shaping consumer trust and insurer reliability. By providing a standardized measure of financial health, these ratings enable policyholders to navigate the complex health insurance landscape with confidence. Whether it’s a young professional seeking affordable coverage or a retiree prioritizing stability, understanding and leveraging AM Best ratings can lead to better outcomes. For insurers, maintaining a strong rating is not just about reputation but about fostering long-term relationships with policyholders built on trust and reliability.

Danville, VA: Finding the Right Medicare Supplement Insurance

You may want to see also

Frequently asked questions

AM Best health insurance ratings are a measure of an insurance company's financial strength, stability, and ability to meet its ongoing obligations to policyholders. AM Best is a globally recognized credit rating agency that specializes in the insurance industry, providing independent opinions and assessments of insurance companies.

AM Best determines health insurance ratings through a comprehensive evaluation process that considers various factors, including an insurer's balance sheet strength, operating performance, business profile, and enterprise risk management. The rating agency analyzes financial statements, conducts interviews with company management, and assesses the company's competitive position, market share, and risk management practices.

AM Best health insurance ratings are important for consumers because they provide valuable insights into an insurance company's financial health and its ability to pay claims. A high rating (e.g., A++ or A+) indicates a strong financial foundation and a lower risk of default, giving policyholders confidence that their claims will be paid in a timely manner. Consumers can use these ratings to compare insurance companies and make informed decisions when selecting a health insurance provider.