Health insurance ratings play a crucial role in helping individuals and families make informed decisions about their healthcare coverage. These ratings, often provided by independent agencies or consumer organizations, evaluate insurance companies based on factors such as customer satisfaction, financial stability, claims processing efficiency, and the breadth of coverage offered. Understanding AM Best health insurance ratings, for instance, can provide insights into an insurer’s ability to meet its financial obligations, ensuring policyholders are protected when they need it most. By comparing these ratings, consumers can identify plans that offer the best balance of affordability, reliability, and comprehensive benefits, ultimately securing peace of mind in managing their health and financial well-being.

Explore related products

What You'll Learn

- Financial Strength Ratings: Assesses insurer's ability to meet claims obligations

- Customer Satisfaction Scores: Measures policyholder experience and service quality

- Claims Processing Efficiency: Evaluates speed and accuracy of claim settlements

- Coverage Options Analysis: Reviews policy benefits, exclusions, and flexibility

- Premium Cost Comparison: Compares pricing across plans and providers

![]()

Financial Strength Ratings: Assesses insurer's ability to meet claims obligations

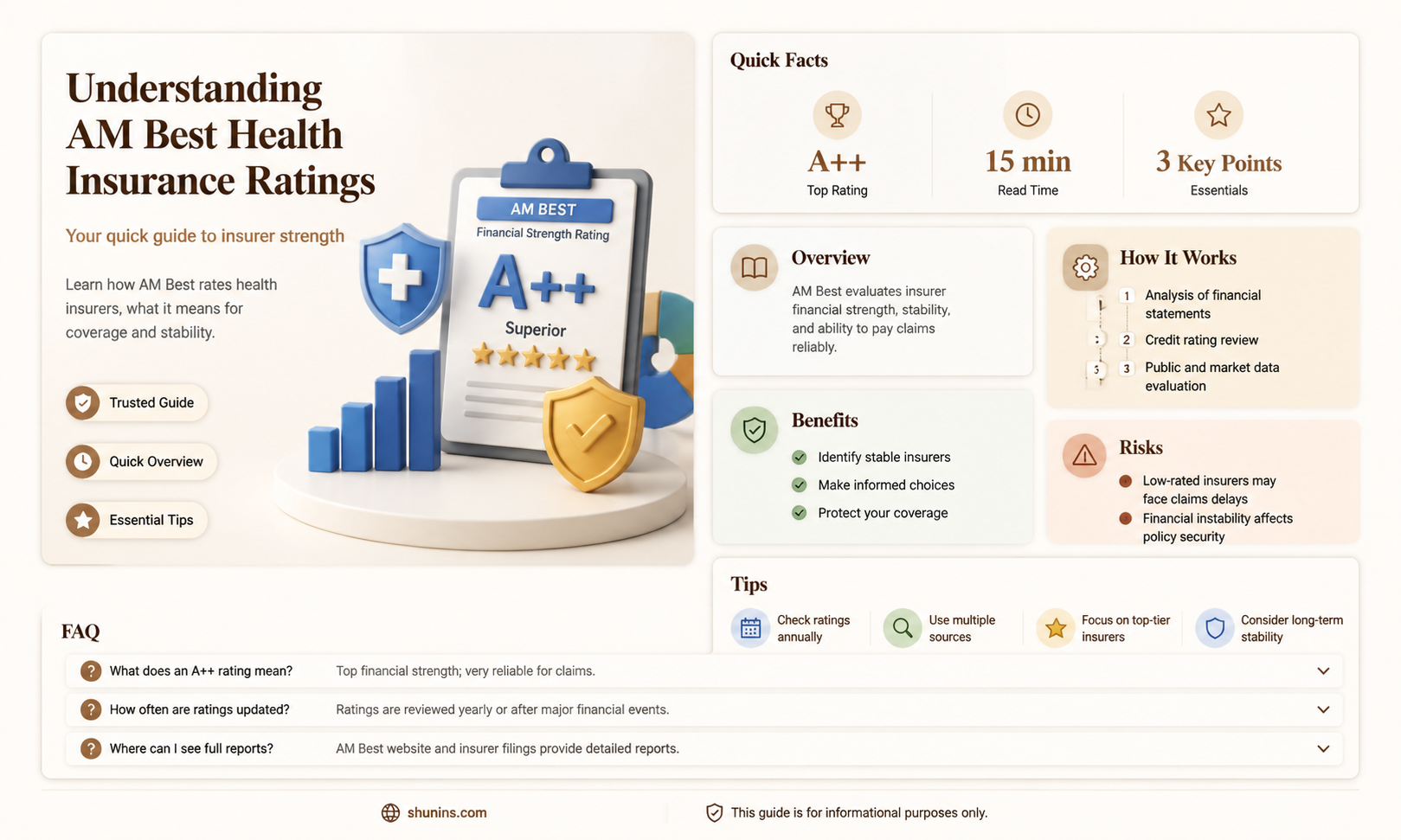

Financial strength ratings are a critical tool for evaluating an insurer's ability to fulfill its claims obligations, providing policyholders with a measure of security and confidence. These ratings, assigned by independent agencies like A.M. Best, Moody's, and Standard & Poor's, assess an insurer's financial health, capital adequacy, and risk management practices. For instance, A.M. Best uses a letter-grade system, with "A++" and "A+" indicating superior and excellent financial strength, respectively. Understanding these ratings is essential for anyone considering health insurance, as they directly impact the insurer's reliability in times of need.

To interpret financial strength ratings effectively, start by identifying the rating agency and its specific scale. For example, Moody's uses a system ranging from "Aaa" (highest quality) to "C" (lowest quality), while Standard & Poor's employs a similar scale from "AAA" to "D." Cross-referencing ratings from multiple agencies can provide a more comprehensive view of an insurer's financial stability. Additionally, consider the rating trend—whether it has been stable, upgraded, or downgraded over time. A consistent "A" rating from A.M. Best, for instance, suggests long-term financial reliability, whereas a recent downgrade might warrant closer scrutiny.

One practical tip for policyholders is to prioritize insurers with ratings of "A-" or higher, as these are generally considered financially secure. However, it's also important to balance financial strength with other factors like coverage options, premiums, and customer service. For example, a smaller insurer with a slightly lower rating might offer more personalized service or competitive pricing. Conversely, a highly rated insurer may provide peace of mind but at a higher cost. Evaluating your risk tolerance and budget alongside financial strength ratings ensures a well-rounded decision.

A comparative analysis reveals that financial strength ratings are particularly crucial in health insurance, where claims can be unpredictable and costly. Unlike auto or home insurance, health claims often involve long-term or catastrophic expenses, making an insurer's ability to pay out claims over time a critical factor. For instance, an insurer with a strong financial rating is more likely to handle a surge in claims during a public health crisis without compromising its obligations. This resilience is a key differentiator when comparing insurers, especially in volatile economic or health environments.

In conclusion, financial strength ratings serve as a vital indicator of an insurer's capacity to meet claims obligations, offering policyholders a benchmark for reliability. By understanding rating scales, trends, and their implications, individuals can make informed decisions that align with their financial and health needs. While a high rating is reassuring, it should be one of several factors considered when choosing health insurance. Ultimately, the goal is to find an insurer that not only promises to pay claims but has the proven financial strength to do so consistently.

Discover the Most Affordable Life Insurance Providers in 2023

You may want to see also

Explore related products

![]()

Customer Satisfaction Scores: Measures policyholder experience and service quality

Customer satisfaction scores are the pulse of health insurance ratings, revealing how well a company meets policyholder needs. These scores, often derived from surveys and feedback, quantify experiences across claims processing, customer service, and overall value. For instance, a 2023 J.D. Power study found that insurers with satisfaction scores above 850 (on a 1,000-point scale) had 30% lower policyholder churn rates. This metric isn’t just a number—it’s a predictor of loyalty and a benchmark for service quality.

Analyzing these scores requires context. A high satisfaction rating in claims processing might indicate efficient payouts, but it could also mask issues like delayed responses or complex paperwork. For example, Company A may score 90% in claims satisfaction but have a 48-hour average response time, while Company B scores 85% but resolves claims within 24 hours. Policyholders aged 55+ often prioritize responsiveness, while younger demographics may value digital tools. Understanding these nuances ensures scores reflect real-world experiences, not just surface-level performance.

To improve satisfaction scores, insurers must focus on actionable insights. Start by segmenting feedback by age, policy type, and interaction channel. For instance, millennials may rate mobile app usability higher than phone support. Implement changes incrementally: reduce call wait times by 10% quarterly, or introduce a claims tracker tool. Caution: avoid overloading staff with new protocols without training. A 2022 survey showed that 60% of policyholders would switch insurers after just two negative experiences, so consistency is key.

Comparatively, satisfaction scores also highlight industry trends. Telehealth integration, for example, has become a differentiator, with insurers offering virtual care seeing a 15% uptick in satisfaction among policyholders under 40. However, this feature alone isn’t a silver bullet. Companies must balance innovation with traditional service quality. A descriptive takeaway: imagine a policyholder filing a claim via app, receiving updates via SMS, and speaking to a representative who already knows their case. This seamless experience is what drives top scores.

Ultimately, customer satisfaction scores are a call to action for insurers. They demand transparency, adaptability, and a focus on policyholder needs. By dissecting these scores, companies can identify pain points—like a 20% dissatisfaction rate in billing clarity—and address them systematically. Practical tip: conduct quarterly satisfaction surveys with incentives (e.g., a $10 gift card) to boost response rates. The takeaway? High scores aren’t just about retaining customers—they’re about building trust in an industry where trust is paramount.

Why Insurance Companies Often Include 'Mutual' in Their Names

You may want to see also

Explore related products

![Texas Property and Casualty Insurance License Exam Prep - Full-Length Practice Tests, Secrets Study Guide and Review: [Detailed Answer Explanations]](https://m.media-amazon.com/images/I/71J3Oq50CJL._AC_UY218_.jpg)

![]()

Claims Processing Efficiency: Evaluates speed and accuracy of claim settlements

Efficient claims processing is a cornerstone of customer satisfaction in health insurance. Policyholders expect timely reimbursement for medical expenses, and delays can exacerbate financial stress during already challenging times. A 2023 J.D. Power study revealed that insurers with average claim processing times under 10 days scored 20% higher in customer satisfaction metrics compared to those taking over two weeks. This highlights the direct correlation between speed and policyholder loyalty.

Analyzing the Impact of Automation:

The integration of artificial intelligence ( AI) and robotic process automation (RPA) is revolutionizing claims processing. These technologies can automate data extraction from medical bills, verify coverage eligibility, and flag potential fraud, significantly reducing manual intervention. For instance, a leading insurer reported a 40% decrease in processing time after implementing an AI-powered claims adjudication system, allowing them to settle 85% of claims within 48 hours. However, relying solely on automation carries risks. Complex cases requiring human judgment, such as those involving pre-existing conditions or disputed diagnoses, necessitate a hybrid approach where technology assists human reviewers.

Beyond Speed: The Crucial Role of Accuracy:

While speed is essential, accuracy is equally vital. Errors in claim settlements, such as incorrect benefit calculations or denied claims due to coding discrepancies, can lead to costly appeals and damage the insurer's reputation. A single inaccurate claim can result in financial losses for both the policyholder and the insurer, highlighting the need for robust quality control measures. Implementing multi-level reviews, utilizing standardized coding systems, and providing ongoing training for claims adjusters are crucial strategies to minimize errors.

Transparency Builds Trust:

Policyholders appreciate transparency throughout the claims process. Providing clear communication regarding claim status, expected timelines, and reasons for delays fosters trust and reduces anxiety. Insurers can leverage digital platforms and mobile apps to offer real-time updates, allowing policyholders to track their claims and access explanations for any adjustments. This proactive approach demonstrates a commitment to customer service and empowers individuals to make informed decisions about their healthcare.

Benchmarking for Continuous Improvement:

To ensure ongoing efficiency, insurers should benchmark their claims processing performance against industry standards and competitors. Analyzing key performance indicators (KPIs) such as average processing time, first-pass resolution rate, and customer satisfaction scores allows for identifying areas for improvement. Regularly reviewing claims data can reveal bottlenecks, common error types, and opportunities for process optimization, ultimately leading to a more streamlined and customer-centric claims experience.

How to Easily Check Your Health Insurance Status: A Quick Guide

You may want to see also

Explore related products

![]()

Coverage Options Analysis: Reviews policy benefits, exclusions, and flexibility

Health insurance policies often tout comprehensive coverage, but the devil is in the details. A meticulous review of policy benefits, exclusions, and flexibility is crucial to ensure you’re not left with unexpected gaps in protection. For instance, while most plans cover hospitalization and emergency care, the extent of coverage for preventive services like annual check-ups, vaccinations, or mental health care can vary widely. A policy that includes telehealth services or wellness programs might offer greater flexibility for managing health proactively, especially for individuals with chronic conditions or those seeking convenient care options.

Consider exclusions as the fine print that can derail your financial stability. Common exclusions include cosmetic procedures, experimental treatments, and pre-existing conditions during a waiting period. For example, a policy might exclude coverage for bariatric surgery unless deemed medically necessary, or it may limit prescription drug coverage to generic medications only. Understanding these limitations requires scrutinizing the policy’s Summary of Benefits and Coverage (SBC), which outlines what is and isn’t covered in plain language. Ignoring this step could lead to out-of-pocket expenses that negate the perceived value of the plan.

Flexibility in coverage is often underestimated but can be a game-changer in dynamic life situations. Policies with customizable deductibles, copayments, or out-of-pocket maximums allow you to align your insurance with your financial risk tolerance. For instance, a high-deductible health plan (HDHP) paired with a Health Savings Account (HSA) offers tax advantages and greater control over healthcare spending, particularly for healthy individuals under 40 who rarely require medical services. Conversely, families with children or older adults might prioritize lower deductibles and broader provider networks for predictable costs and accessibility.

A practical approach to analyzing coverage options involves comparing policies side by side using real-life scenarios. For example, calculate the total cost of managing a chronic condition like diabetes under different plans, factoring in premiums, copays for specialist visits, and insulin coverage. Similarly, assess how each policy handles catastrophic events, such as cancer treatment, by examining coverage limits for chemotherapy, radiation, and rehabilitation services. This methodical comparison ensures you’re not just choosing the cheapest plan but the one that best meets your specific health and financial needs.

Finally, don’t overlook the role of customer reviews and third-party ratings in evaluating coverage options. Platforms like the National Committee for Quality Assurance (NCQA) and J.D. Power provide insights into insurer performance, including claims processing efficiency and customer satisfaction. Reviews often highlight pain points, such as denied claims or restrictive provider networks, that official policy documents might obscure. Combining this qualitative data with your quantitative analysis ensures a well-rounded understanding of how a policy performs in real-world situations, helping you make an informed decision.

Understanding HSA Eligibility and Health Insurance Premiums

You may want to see also

Explore related products

![]()

Premium Cost Comparison: Compares pricing across plans and providers

Health insurance premiums can vary dramatically, even for similar coverage levels, making a direct comparison essential for cost-conscious consumers. A 35-year-old nonsmoker in Texas, for instance, might pay $312 monthly for a Silver plan with a $4,000 deductible through Provider A, while Provider B offers a comparable plan for $278. This $34 monthly difference translates to $408 annually, a significant savings without sacrificing coverage. Such disparities highlight the importance of meticulous comparison, as premiums are influenced by factors like age, location, and provider-specific pricing strategies.

To effectively compare premiums, start by identifying your coverage needs—deductible tolerance, copay preferences, and essential services. Use online tools like Healthcare.gov or private comparison platforms to input your details and generate a side-by-side view of plans. For example, a family of four in California might find that Provider X’s Gold plan costs $1,200 monthly but includes free preventive care, while Provider Y’s Silver plan is $950 monthly but requires 20% coinsurance for specialist visits. Analyzing these trade-offs ensures you’re not overpaying for unnecessary features or underinsuring critical needs.

A persuasive argument for premium comparison lies in its long-term financial impact. Consider a 28-year-old in New York who chooses a Bronze plan at $250 monthly over a Gold plan at $500, saving $3,000 annually. However, if they require unexpected surgery with a $7,000 out-of-pocket maximum on the Bronze plan, their total yearly cost could surpass $9,500. Conversely, the Gold plan’s $1,000 out-of-pocket maximum would cap expenses at $6,000. This example underscores that lower premiums don’t always equate to lower overall costs, making a holistic comparison critical.

Practical tips can streamline the comparison process. First, check if your preferred doctors and hospitals are in-network for each plan, as out-of-network care can negate premium savings. Second, factor in subsidies or employer contributions, which can significantly reduce net costs. For instance, a household earning $60,000 annually might qualify for a $400 monthly subsidy, making a $600 premium plan effectively $200. Lastly, review customer satisfaction ratings alongside premiums; a cheaper plan with poor service may cost more in stress and unresolved claims.

In conclusion, premium cost comparison is a cornerstone of informed health insurance decision-making. By analyzing specific examples, understanding trade-offs, and applying practical strategies, consumers can secure plans that balance affordability with adequate coverage. Whether saving $408 annually or avoiding hidden out-of-pocket traps, the effort invested in comparison pays dividends in financial security and peace of mind.

Why Mortgage Companies Require Hazard Insurance: Protecting Investments

You may want to see also

Frequently asked questions

AM Best health insurance ratings are financial strength and credit ratings assigned by AM Best, a leading credit rating agency specializing in the insurance industry. These ratings assess an insurer’s ability to meet its financial obligations, such as paying claims. They are important because they help consumers and businesses evaluate the reliability and stability of an insurance company before purchasing a policy.

AM Best determines its ratings by analyzing an insurer’s financial health, including its balance sheet strength, operating performance, business profile, and enterprise risk management. Factors like capitalization, liquidity, profitability, and market position are considered. Ratings range from A++ (Superior) to D (Poor), with higher ratings indicating stronger financial stability.

While a low AM Best rating may indicate financial instability, it doesn’t necessarily mean you should avoid the company. However, it’s advisable to prioritize insurers with higher ratings (A- or better) for greater assurance that they can fulfill their obligations. Always consider the rating alongside other factors like coverage options, customer service, and pricing when choosing a health insurance provider.