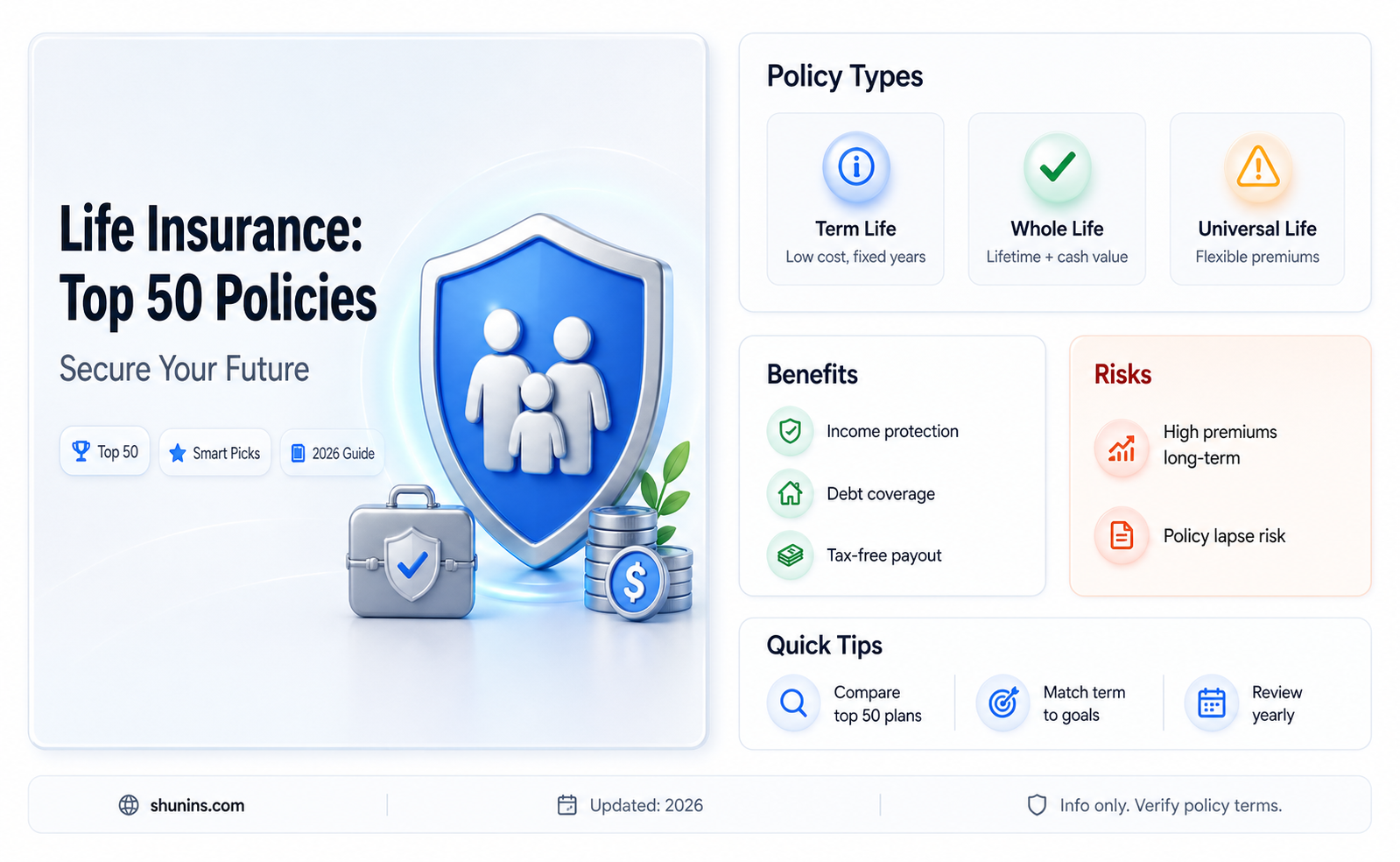

Life insurance is a financial safety net for your loved ones, offering them support in the wake of your passing. It's a way to protect the people who matter most to you.

There are many life insurance companies out there, so how do you choose the best one for you? Here's a list of the top 50 life insurance companies, in no particular order:

1. Nationwide

2. Banner by Legal & General

3. Lafayette Life

4. SBLI

5. Penn Mutual

6. Thrivent

7. Pacific Life

8. Symetra

9. Protective Life

10. MassMutual

11. Lincoln Financial

12. Principal

13. Corebridge Financial (formerly AIG)

14. State Farm

15. New York Life

16. Mutual of Omaha

17. USAA

18. Guardian Life

19. Bestow

20. Haven Life

21. Northwestern Mutual

22. John Hancock

23. Prudential

24. Equitable

25. Transamerica

26. John Hancock

27. North American

28. Western & Southern

29. Brighthouse

30. Securian

31. Farmers

32. Northwestern Mutual

33. Symetra

34. Foresters

35. Gerber

36. Minnesota Life

37. Fidelity

38. Mutual Trust Life Solutions

39. Corebridge Financial (formerly AIG)

40. New York Life

41. Kansas City Life

42. Globe Life

43. Aflac

44. Boston Mutual

45. Bankers

46. American National

47. Colonial Penn

48. Allianz

49. Legal & General America

50. Transamerica

Explore related products

What You'll Learn

![]()

Whole life insurance

Some companies that offer whole life insurance include Lafayette Life, MassMutual, Pacific Life, and Protective.

Term Life Insurance: Do You Have Coverage?

You may want to see also

Explore related products

![]()

Universal life insurance

When you die, your beneficiaries will receive the death benefit, but the insurance company will keep the remaining cash value.

Life Insurance and Taxes: What You Need to Know

You may want to see also

Explore related products

![]()

Term life insurance

There are several types of term life insurance:

- Fixed term: The most popular type of term life insurance, which lasts for 10, 20, or 30 years. The premiums remain static throughout the policy.

- Increasing term: This type of policy allows you to increase the value of your death benefit over time, but the premiums will also increase slightly. These policies tend to be more expensive but offer a larger payout.

- Decreasing term: This type of policy reduces the premium payments over time, which may result in a smaller death benefit. This option is suitable for those who predict they will have fewer financial obligations as they age.

- Annual renewable: This type of policy provides coverage on a yearly basis and must be renewed by the end of the term to continue coverage. The premiums usually increase each time the plan is renewed, making this option more expensive overall.

When choosing a term life insurance policy, it is important to consider the company's financial strength and stability to ensure they will be able to pay out a claim if needed. You can check the company's financial strength rating through independent rating agencies such as AM Best.

Wealth Calculation: Does Life Insurance Count?

You may want to see also

Explore related products

![]()

No-exam life insurance

There are three types of no-exam life insurance:

- Accelerated Underwriting Life Insurance: This process involves the insurance company gathering information about the applicant electronically, and using algorithms to assess the quote. It can be just as competitively priced as a traditional policy.

- Simplified Issue Life Insurance: This is a streamlined process that usually only involves answering some health and lifestyle questions, without a medical exam. The cost tends to be higher because the insurer has minimal information about the applicant.

- Guaranteed Issue Life Insurance: This type of policy is intended for those in poor health who want minimal coverage, usually for funeral expenses. There is no medical exam and no questions, and the applicant cannot be turned down. This option tends to be the most expensive.

When considering a no-exam life insurance policy, it's important to assess your chances of being approved, as a denial can hinder future applications. Additionally, no-exam policies may have maximum coverage caps, so it's important to calculate your coverage needs beforehand. It's also worth noting that rates for no-medical-exam term life are generally on par with those for standard term policies.

Graded Life Insurance: Understanding the Policy and Its Benefits

You may want to see also

Explore related products

![]()

Permanent life insurance

There are several types of permanent life insurance policies:

Whole Life Insurance

Whole life insurance is the most common type of permanent life insurance. It is a policy that covers you for your whole life, with fixed premiums that won't change over time. Whole life insurance policies also accumulate cash value over time, which can be used as a financial tool to support other goals. This type of policy is offered by companies such as Pacific Life, Northwestern Mutual, Guardian Life, and Protective.

Universal Life Insurance

Universal life insurance offers a death benefit and accumulates cash value, but it differs from whole life insurance in that it provides flexibility over premium payments. You can adjust your premiums or raise/lower your death benefit amount within certain limits. This type of policy is offered by companies such as Lincoln Financial and Protective.

Variable Universal Life Insurance

Variable universal life insurance is similar to universal life insurance but offers more flexibility in how the cash value is managed. You can invest your cash value in sub-accounts tied to the market, allowing for potentially higher growth. However, this also means that the value of your cash could decline.

Indexed Universal Life Insurance

Indexed universal life insurance is another type of universal life insurance where the cash value grows based on a chosen stock market index. If the chosen index performs well, the account will grow, and if it doesn't, some companies allow it to grow at a minimum rate.

Life Insurance Options for Diabetics: What You Need to Know

You may want to see also

Frequently asked questions

AM Best is a credit rating agency that assigns insurance companies a letter grade from "A++" to "D", indicating their ability to pay claims and meet financial obligations.

AM Best evaluates insurance companies based on financial stability, customer satisfaction, and other factors to determine their ability to honour claims and provide reliable coverage.

A high AM Best rating, such as an A or A++, indicates superior financial strength and a lower risk of defaulting on debts. This gives confidence that the insurer will be able to pay out claims in the future.

While AM Best rates many insurance companies, not all companies choose to pursue or achieve an AM Best rating. It is important to consider other factors and ratings when evaluating insurance providers.

You can typically find the AM Best rating of a life insurance company by searching for it on the AM Best website or through third-party sources that compile and compare insurance company ratings.