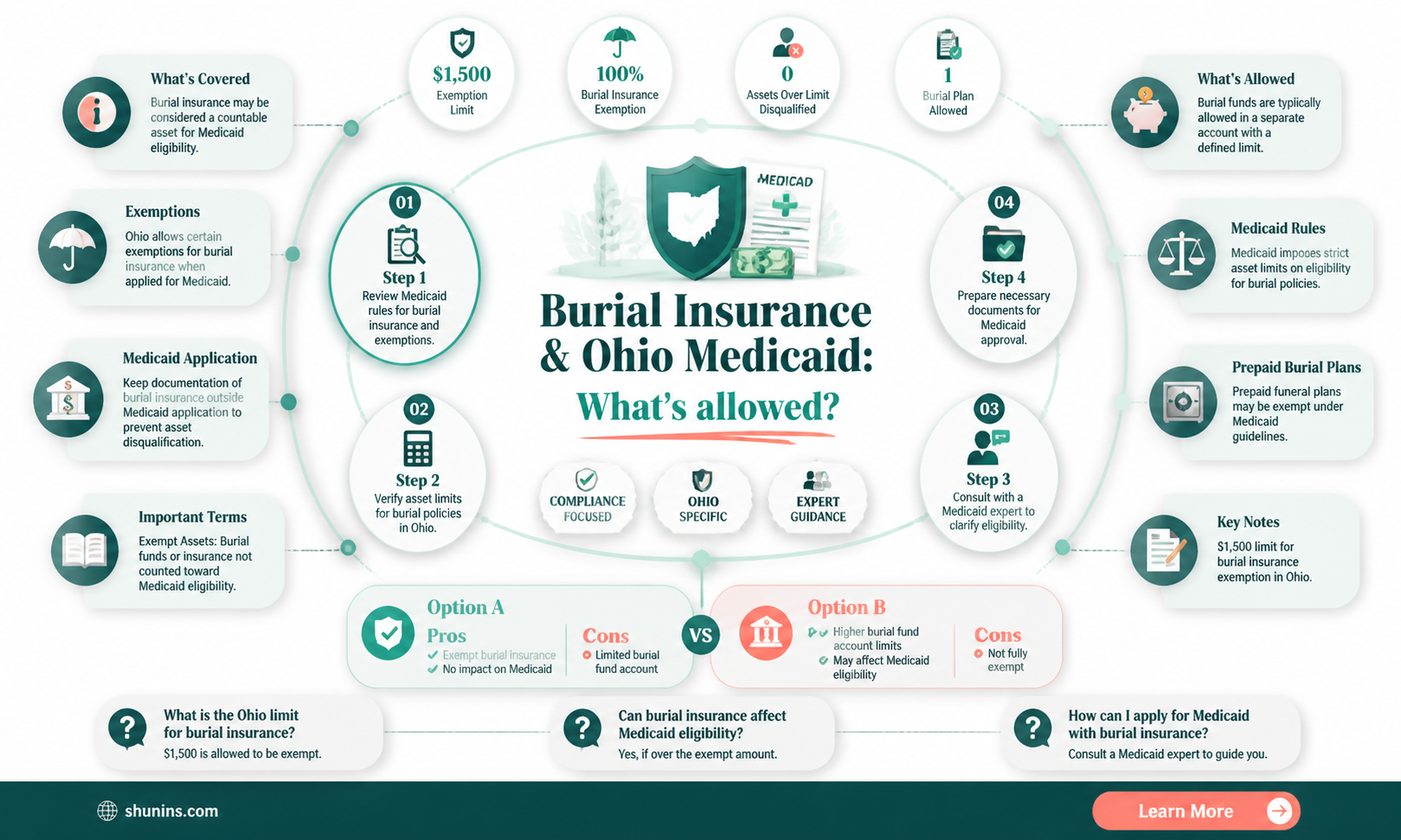

Medicaid is a state and federally funded health insurance program for people with low incomes and a critical need for medical care. Each state has different rules regarding Medicaid, and Ohio is no exception. In this paragraph, we will explore the topic of burial insurance and its compatibility with Ohio Medicaid, highlighting the key points that you need to know.

Explore related products

What You'll Learn

![]()

Burial funds and burial space items

Medicaid rules vary from state to state and are subject to change. It is always best to consult a qualified attorney or professional tribute planner to ensure that your contract meets all of your state’s requirements for Medicaid spend-down.

In Ohio, Medicaid allows for burial funds and burial space items to be set aside within an irrevocable contract as two separate categories. "Irrevocable" means that there is no option to cancel the contract for its cash value, which excludes it from being counted as an asset.

Burial funds may include everything that may be needed for a funeral service for both the Medicaid applicant and their spouse. This includes funeral goods and services, embalming, cosmetics, clothing, cremation fees, flowers, honorariums, limousines, police escort, obituaries, and so on. The burial funds must be placed in an irrevocable prepaid funeral contract (maximum value determined by the state), or they must be less than $1,500 if the funds are in a revocable account.

Burial space items can be purchased for the applicant, their spouse, and the applicant's immediate family members and their spouses. Burial space items include caskets, urns, grave liners, vaults, burial plots, cremation niches, family crypt, grave markers, and perpetual care. Burial space items are counted as separate from burial funds.

Understanding Self-Insured Medical Plans: An Alternative Approach

You may want to see also

Explore related products

![]()

Irrevocable prepaid burial contracts

In the state of Ohio, irrevocable prepaid burial contracts are not considered a resource. Any portion of the contract that represents burial funds reduces the amount available under the burial funds exclusion. However, any part of the contract that represents the purchase of burial spaces has no effect on the burial funds exclusion.

A burial space refers to a burial plot, gravesite, crypt, mausoleum, casket, urn, niche, or other repository traditionally used for the deceased's bodily remains. It also includes a contract for the care and maintenance of the gravesite and necessary improvements or additions to such spaces.

A burial contract can be funded by an individual purchasing a life insurance policy and then assigning the proceeds to a third party, typically a funeral provider. The resource value of the burial contract is equal to the cash surrender value (CSV) of the life insurance policy, subject to the burial funds exclusion. If the face value (FV) of the burial funds portion of the contract exceeds $1500, it is treated according to the burial funds exclusion.

Malpractice Insurance: Understanding Coverage for Medical Professionals

You may want to see also

Explore related products

![]()

Burial insurance as an asset

Burial insurance is a type of life insurance that covers funeral services and merchandise costs after an individual's death. It is typically a feature of whole life insurance coverage rather than a separate offering. Burial insurance is a cash policy, meaning it builds cash value over time. This cash value, or surrender value, is the amount the policy owner would receive if the policy were cashed in.

In the context of Ohio Medicaid, burial insurance and burial spaces are treated as excluded resources, regardless of their value. This means that they do not count towards the individual's asset total when determining eligibility for medical assistance. Specifically, irrevocable prepaid burial contracts are not considered resources, and any portion of the contract representing burial funds reduces the amount available under the burial funds exclusion.

However, if a contract includes both burial spaces and burial funds without specifying which amounts represent each, the entire contract is considered a resource in the form of burial funds. The resource value of a burial contract is equal to the cash surrender value (CSV) of the life insurance policy. If the face value (FV) of the policy, or the death benefit, exceeds $1500, the CSV is treated according to the burial funds exclusion.

It is important to note that the rules and regulations regarding burial insurance and assets may vary by state and that individuals should refer to their specific insurance contracts and seek professional advice for their unique situations.

Obtaining Medical Insurance Without Providing a Social Security Number

You may want to see also

Explore related products

![]()

Medicaid's asset limit

In the United States, Medicaid provides health coverage for low-income seniors and people with disabilities who are enrolled in Medicare. Medicaid eligibility is based on both the applicant's income and assets (resources).

Countable assets refer to liquid resources such as bank balances, stocks, and bonds. Exempt assets, on the other hand, include home furnishings, appliances, personal items, vehicles, and generally the applicant's home. Additionally, burial spaces or burial space contracts are considered excluded resources, regardless of their value. This means that a burial space held for an individual or their immediate family, such as a burial plot, urn, or casket, does not count towards the asset limit.

The complexity of the Medicaid asset test highlights the importance of Medicaid planning, where families who exceed the asset limit can still become Medicaid-eligible through various strategies.

Get Free Medical Insurance in California: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Burial space exclusion

In the United States, Medicaid is a joint state and federally funded health insurance programme for people with low incomes and a critical need for medical care. Each state sets its own qualification rules, and the rules are constantly changing.

In Ohio, burial spaces are excluded from the resource value of burial contracts. This means that the purchase of a burial space does not affect the burial funds exclusion. A burial space is defined as a burial plot, gravesite, crypt, mausoleum, casket, urn, niche, or other repository customarily and traditionally used for the deceased's bodily remains. It also includes a contract for the care and maintenance of the gravesite, sometimes referred to as endowment or perpetual care, and any necessary and reasonable improvements or additions to such spaces, including vaults, headstones, markers, burial containers, and arrangements for the opening and closing of the gravesite.

The burial space exclusion applies if the burial space contract with a funeral service company represents the current right to use the items at the amount shown. This means that the contract must clearly indicate that it is for the purchase of a burial space and not for burial funds. If the contract does not specify which amounts are for the purchase of burial spaces and which are for burial funds, then the entire contract is considered a resource in the form of burial funds.

Irrevocable prepaid burial contracts are not considered a resource. However, any portion of the contract that represents burial funds will reduce the amount available under the burial funds exclusion.

Medical Insurance Costs in California: What to Expect

You may want to see also

Frequently asked questions

Yes, you can have burial insurance while on Ohio Medicaid. However, there are specific rules regarding burial funds and contracts that you must follow to remain eligible for Medicaid.

Burial funds are considered exempt if they are in an irrevocable prepaid funeral contract with no limit on the amount or in a revocable account of less than $1,500. Burial space items must be in an irrevocable contract to be considered exempt, and there is no limit on the amount. Any portion of the contract that represents burial funds reduces the amount available under the burial funds exclusion.

If you do not follow the rules regarding burial insurance and Medicaid, you may void your Medicaid benefits. It is important to ensure that your burial insurance policy complies with Medicaid's asset limitations. If you are purchasing burial insurance for a parent on Medicaid, you must establish yourself as the policy owner.