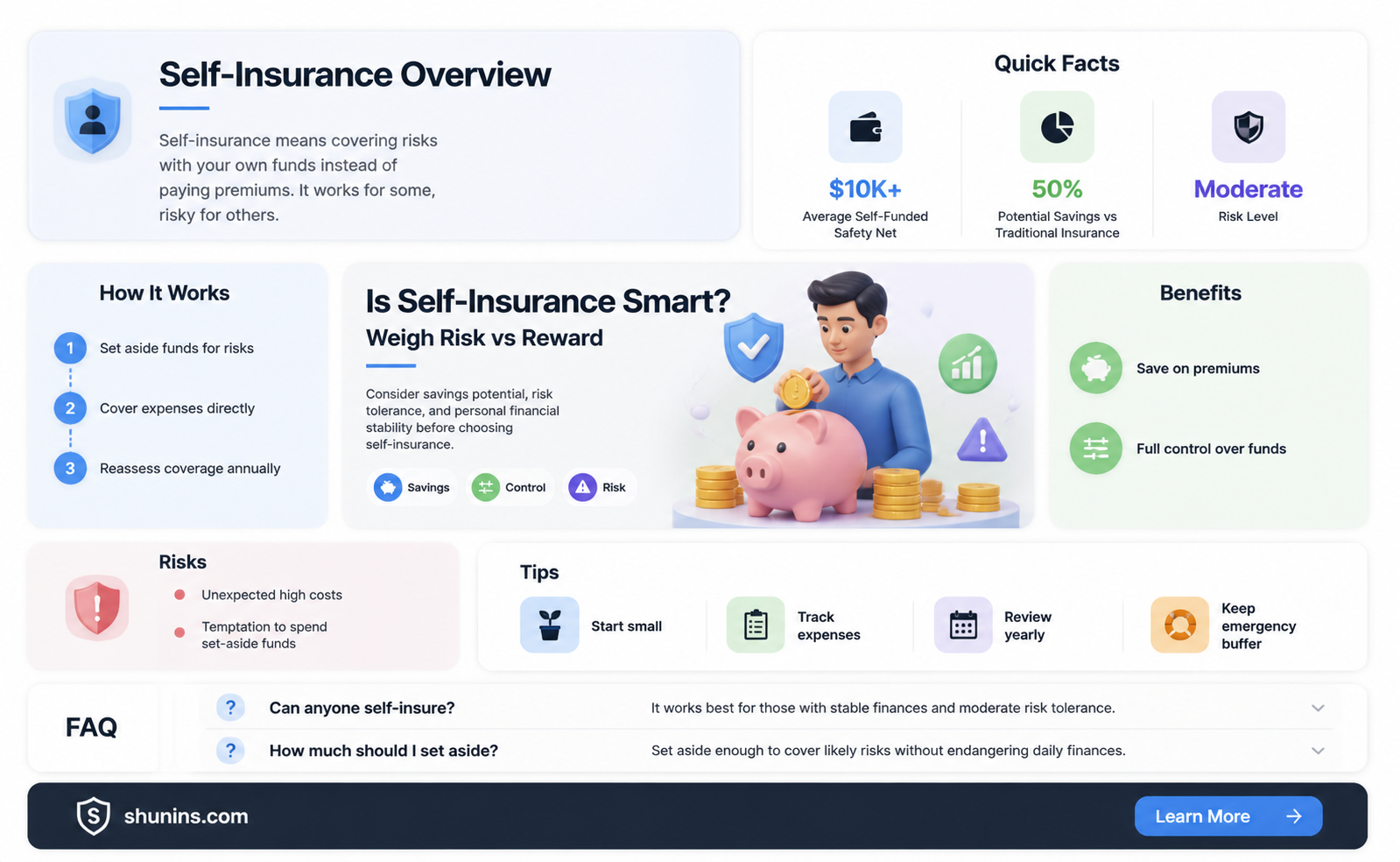

Self-insurance is an alternative to traditional insurance that involves setting aside funds to cover potential losses instead of paying insurance premiums. It can be a flexible and cost-effective option for those with sufficient savings and investments to cover any potential risks. Self-insurance is more common in healthcare, where individuals may choose to set aside money for specific procedures or routine treatments rather than pay for an additional insurance policy. However, it is important to consider the potential for unforeseen costs and the financial strain that could result. For significant risks, maintaining insurance with a high deductible can balance cost savings and risk mitigation.

| Characteristics | Values |

|---|---|

| Definition | Self-insurance is a strategic option for those willing to accept the risks associated with paying for potential losses directly from their own funds. |

| Pros | No insurance premiums, more flexibility, cost-effective, peace of mind |

| Cons | Risk of unforeseen costs potentially leading to financial strain, may not have sufficient funds to cover liability, may not be practical for health insurance and car insurance |

| Who is it for? | Those with no debt and a considerable amount of assets, those with high net worth relative to the value of their house, businesses |

| Examples | Health insurance, car insurance, renter's insurance, life insurance, warranties |

Explore related products

What You'll Learn

![]()

Self-insurance can save you money

Self-insurance can be a great way to save money on insurance premiums. By being self-insured, you can avoid paying unnecessary insurance premiums and instead rely on your savings and investments to cover any potential risks. This approach can be particularly useful for minor expenses or when you want to avoid high insurance premiums for unlikely events. For example, if you have no debt and a significant amount of assets, you may choose to self-insure for life insurance. Similarly, some tenants prefer to self-insure by setting aside money to protect their assets in the rental property instead of purchasing renter's insurance.

Another example is health insurance, where self-insurance is more common than in car insurance. People might choose to set aside money for specific health needs, such as dental care or braces, instead of paying for an additional insurance policy that covers these expenses. Additionally, self-insurance can be beneficial for businesses looking to control healthcare costs without compromising their employees' health. Self-funded insurance plans offer flexibility and the potential to get money back at the end of the year.

However, it's important to consider the risks associated with self-insurance. While it can save you money on premiums, you must be prepared to cover any potential losses directly from your funds. For significant risks, maintaining insurance with a high deductible can balance cost savings and risk mitigation. Additionally, in the case of property insurance, the cost to repair major damage could exceed your available funds, and you may experience multiple losses or damage events in a short period, quickly depleting your savings.

Self-insurance is most suitable when you have a good understanding of the potential worst-case scenarios and are confident in your ability to financially handle them. It is generally more feasible for minor or unlikely expenses, allowing you to save money by bypassing insurance premiums. However, for major risks, it is essential to carefully weigh the potential costs against the benefits of self-insurance.

Life Insurance: Preparation for Peace of Mind

You may want to see also

Explore related products

![]()

Self-insurance offers flexibility

Self-insurance is a strategic option for those who can afford to pay for potential losses directly from their funds. It offers flexibility in terms of cost and coverage. By choosing self-insurance, individuals can retain the money they would have spent on insurance premiums and use those funds to build up savings. This option is particularly attractive to those who want to avoid high insurance premiums for unlikely events. For example, some tenants prefer to self-insure rather than purchase renter's insurance to protect their assets in the rental.

Self-insurance allows individuals to choose what they want to insure. For instance, some may opt for self-insurance for basic auto insurance to afford more comprehensive insurance for their homes, which they believe have greater potential liability. Self-insurance is also a common option for healthcare. People might set aside money for specific health needs, such as dental care or braces, instead of paying for an extra policy with benefits they might not use.

Self-insurance can also be a strategic option for businesses. As healthcare costs continue to rise, businesses explore self-insurance as a way to control costs without compromising their employees' health. Self-insurance offers flexibility in managing healthcare costs and allows employers to provide health benefits to their employees without going through an insurance company.

However, self-insurance carries the risk of unforeseen costs, potentially leading to financial strain. It is important for individuals and businesses to understand the potential worst-case scenarios and ensure they have sufficient funds to cover liabilities. Self-insurance may not always be a practical option for high-cost events, such as health insurance or car insurance, due to the potential risk and high payout.

Life Insurance Accounts: Types and Options Explained

You may want to see also

Explore related products

![]()

Self-insurance is risky

Self-insurance is a strategic option for those who can accept the risks associated with paying for losses directly from their funds. It may be a good option for those who want to avoid insurance premiums and have control over their insurance coverage. However, self-insurance is not without its risks.

The financial risk is one of the most significant disadvantages of self-insurance. When an individual or organization self-insures, they take on the entire financial risk of potential loss. This can be challenging for smaller organizations or individuals who may not have the financial resources to cover large, unexpected claims. In the event of a catastrophic event or large claim, self-insurance can be financially devastating if insufficient funds are set aside.

Another disadvantage is the administrative burden of self-insurance. It requires expertise in managing retained risk, including policy wording, risk management, claims handling, and financial management. Small organizations or individuals may not have the necessary resources to effectively handle these responsibilities.

Additionally, self-insurance exposes individuals or organizations to the risk of unforeseen losses. They are responsible for covering the full cost of any retained losses, which can be challenging to predict or plan for. This unpredictability of losses is a significant risk to consider.

Self-insurance may also not provide adequate coverage for certain risks. For example, in the case of health insurance, self-insurance may not be practical due to the potentially high costs of medical care. Similarly, for very expensive risks, such as homeowners' insurance, self-insurance may only be feasible for those with high net worth and a low risk-averse attitude.

While self-insurance can offer flexibility and cost savings, it is essential to carefully consider the potential risks and ensure sufficient resources are available to cover any unforeseen losses.

Life Insurance Proceeds: Can Creditors Garnish Your Money?

You may want to see also

Explore related products

$39.99 $119.95

![]()

Self-insurance is more common with healthcare

Self-insurance is when an individual or entity has enough money to cover any losses or claims without the help of an insurance company. In the case of healthcare, self-insurance is usually an employer taking on the responsibility of setting funds aside to pay for employee healthcare claims instead of a health insurer. This is also referred to as a self-funded plan.

There are several benefits to self-insurance in healthcare. Firstly, it can provide a clearer picture of employee healthcare claims, allowing employers to design more flexible benefit programs. Secondly, self-insurance can result in cost savings for employers, as they are not paying insurance premiums and may have money left over at the end of the year. Finally, self-insurance allows employers to offer the same benefit package to employees in different states, as they are exempt from state health insurance mandates.

However, there are also some drawbacks to self-insurance in healthcare. One potential pitfall is that self-insured employers tend to pay higher rates to hospitals and other providers compared to insured health plans. Additionally, self-insurance carries the risk of unforeseen costs, which could result in financial strain. Furthermore, self-insurance may result in higher costs for employees who use healthcare services, as the higher prices paid by self-insured plans are often passed on to the employees.

Overall, self-insurance in healthcare can be a viable option for employers who are willing to take on the associated risks and have the financial means to do so. It offers flexibility and the potential for cost savings, but it is important to carefully consider the potential drawbacks before making the switch from traditional insurance.

Life Insurance Payments: Tax Write-Off or Not?

You may want to see also

Explore related products

![]()

Self-insurance is not the same as being uninsured

Self-insurance is a strategic option for those who can afford to accept the risks associated with paying for losses directly from their own funds. This approach may be suitable for minor expenses or when one wishes to avoid high insurance premiums for unlikely events. However, it is not the same as being uninsured.

Being uninsured means there are no mitigation measures in place. There is no personalised fund to cover the cost of a claim, and the individual simply hopes that they will not need to claim or that they will have enough funds on hand to cover the cost if required. In contrast, self-insurance involves setting aside funds in a dedicated account to cover potential losses. This account can earn interest, providing additional financial benefits.

Self-insurance is a conscious decision made by individuals or businesses who have assessed their financial situation and determined that they have the capacity to bear potential losses. They actively choose to self-insure by forgoing traditional insurance policies and instead building up their savings, investments, and assets to cover any potential risks. This approach allows them to avoid paying insurance premiums and gives them greater control over their finances.

On the other hand, being uninsured can often result from a lack of awareness, financial constraints, or a willingness to take risks. Uninsured individuals may not fully understand the importance of insurance or the potential consequences of not having adequate coverage. They may be unable to afford insurance premiums or choose to gamble by operating without insurance, hoping that they will not encounter any incidents that would require a claim.

In summary, self-insurance is a deliberate and strategic financial decision made by those with the means to cover potential losses. It involves actively setting aside funds to mitigate risks. In contrast, being uninsured is a state of not having any financial protection in place, either by choice or due to financial limitations, and carries the risk of significant financial strain in the event of an unforeseen incident.

Life Insurance: MLM or Legit?

You may want to see also

Frequently asked questions

Self-insurance is when you have enough money to pay for any losses or damages yourself, instead of paying insurance premiums.

Self-insurance can save you money on insurance premiums and give you more flexibility and control over your healthcare costs. You also get to choose what you want to insure.

Self-insurance carries the risk of unforeseen costs, which could lead to financial strain. It may not always be feasible to self-insure, especially for high-cost events like health or car insurance.

Self-insurance may be suitable if you have a high net worth relative to the value of your insured assets and are not risk-averse. Understanding the potential worst-case scenarios can help determine if you are financially prepared for self-insurance.

Self-insurance is more common for minor and predictable expenses. Certain types of insurance, like car insurance, are mandatory in most states, and insurance on a primary home is not tax-deductible.