Life insurance is a way to reduce the financial burden on your loved ones when you die. There are many types of life insurance policies, but they generally fall into two categories: term and permanent. Term life insurance provides coverage for a defined length of time, such as ten years, while permanent life insurance provides lifelong coverage. Within these two categories, there are several types of life insurance accounts. These include whole life, universal life, variable life, and final expense life insurance. Each type of life insurance is designed to meet specific needs and budgets, so it's important to do your research and consult with a financial professional to determine which type of policy is best for you.

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

What You'll Learn

![]()

Term life insurance

There are a few variations on term life insurance. One, called group term life insurance, is common among insurance options that you might have access to through your employer. This type of insurance provides a base amount of coverage for all employees, typically at no cost to the employee, with the ability to purchase additional coverage that is taken out of the employee's paycheck. Another variation is annual renewable term life insurance, which provides coverage on a yearly basis and must be renewed by the policy end date to continue coverage. The premiums usually increase each time the plan is renewed. This option is best for those in need of short-term coverage.

There are also three main types of term life insurance: fixed term, increasing term, and decreasing term. Fixed term is the most popular choice and is the most basic version. It lasts 10, 20, or 30 years, and the premiums remain static. Increasing term allows you to scale up the value of your death benefit throughout the term, but the premiums slightly increase over time. These types of policies tend to cost more but usually deliver a larger payout. Decreasing term reduces the premium payments over time, which can result in a smaller death benefit. This type of insurance makes sense for those who predict they will have fewer financial obligations as they age.

Epilepsy and Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Whole life insurance

The cost of whole life insurance is determined by several factors, including the age and health of the insured, the coverage amount, and the cash value growth rate. Younger individuals tend to pay lower premiums, and the premiums are generally lower the earlier the policy is started. Whole life insurance premiums tend to be higher than term life insurance, but the permanent coverage and ability to build cash value make it a beneficial option for those seeking long-term financial security.

Life Insurance Lab Tests: Alcohol Detection and Implications

You may want to see also

Explore related products

![]()

Universal life insurance

There are a few variations of universal life insurance:

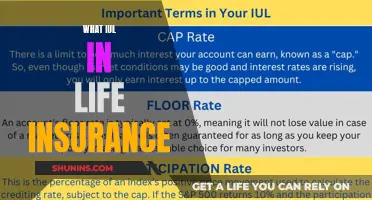

- Variable Universal Life Insurance: This gives you the same kind of lifetime protection and payment flexibility as standard universal life, with more investment options. You can invest part or all of your cash value in "subaccounts". However, you have to choose and manage these investments, assuming more risk and the possibility of losing your principal.

- Indexed Universal Life Insurance: This type of policy allows the policyholder to divide cash value amounts between a fixed account (low-risk investments that are not affected by the stock market) and an equity-indexed account, such as Nasdaq 100 or the S&P 500. The cash value growth is tied to a stock or bond index, allowing it to grow based on the performance of the index.

- Guaranteed Universal Life Insurance: This policy does not offer the same flexibility as other plans and typically has minimal cash value growth and lower premiums.

While universal life insurance offers flexibility, it is important to carefully manage your policy. If your cash value falls to zero and your premiums do not cover the cost of insurance, your policy may lapse. Additionally, if you withdraw more than you've paid into the policy, your withdrawals will be taxed.

Understanding Variable Life Insurance Midpoint Ledgers

You may want to see also

Explore related products

![]()

Variable life insurance

Some insurers offer a hybrid policy known as variable universal life insurance. This has similar features to variable life insurance, except the premiums are adjustable, which may suit those who don't want to commit to paying the same amount in premiums each month.

Term Life Insurance: A Smart Financial Move?

You may want to see also

Explore related products

![]()

Final expense life insurance

Final expense insurance is a more affordable alternative to traditional whole or term life insurance policies, which generally provide higher coverage amounts. Final expense policies are designed for small to moderate costs, typically ranging from $5,000 to $50,000. As a result, the premiums are often much lower, making them accessible to those who may not qualify for larger life insurance policies due to age or medical conditions.

One of the advantages of final expense insurance is its simplicity and ease of application. It usually does not require a medical exam, only a brief health questionnaire. The approval process is generally quick, and coverage can be issued within days or even on the same day as the application. Additionally, final expense policies offer fixed premiums that do not change over time, providing stability and predictability.

When considering final expense life insurance, it is important to look at your monthly expenses, immediate needs, and potential funeral expenses to determine the appropriate coverage amount. Final expense insurance provides a way to ensure that your loved ones are not burdened with unexpected costs during their time of grief and allows you to plan for your end-of-life expenses proactively.

Critical Illness Cover: Enhancing Your Life Insurance

You may want to see also

Frequently asked questions

There are two basic types of life insurance: term insurance and cash-value insurance. Term insurance covers you for a defined length of time, typically one, five, 10, 15, 20, 25 or 30 years. Cash-value insurance, on the other hand, is a permanent life insurance policy that builds up a cash value that can be accessed during your lifetime for any reason.

Term life insurance is a simple, low-cost policy that aims to replace your income when you die. It is typically much cheaper than whole life insurance and offers a higher coverage amount.

Whole life insurance is a permanent life insurance policy that lasts your entire life. It includes a cash value component that grows over time on a tax-deferred basis.

Universal life insurance is another type of permanent life insurance that provides coverage for your entire life as long as you pay the premiums. It is sometimes called adjustable life insurance because it allows you to adjust your premium payments and death benefit.