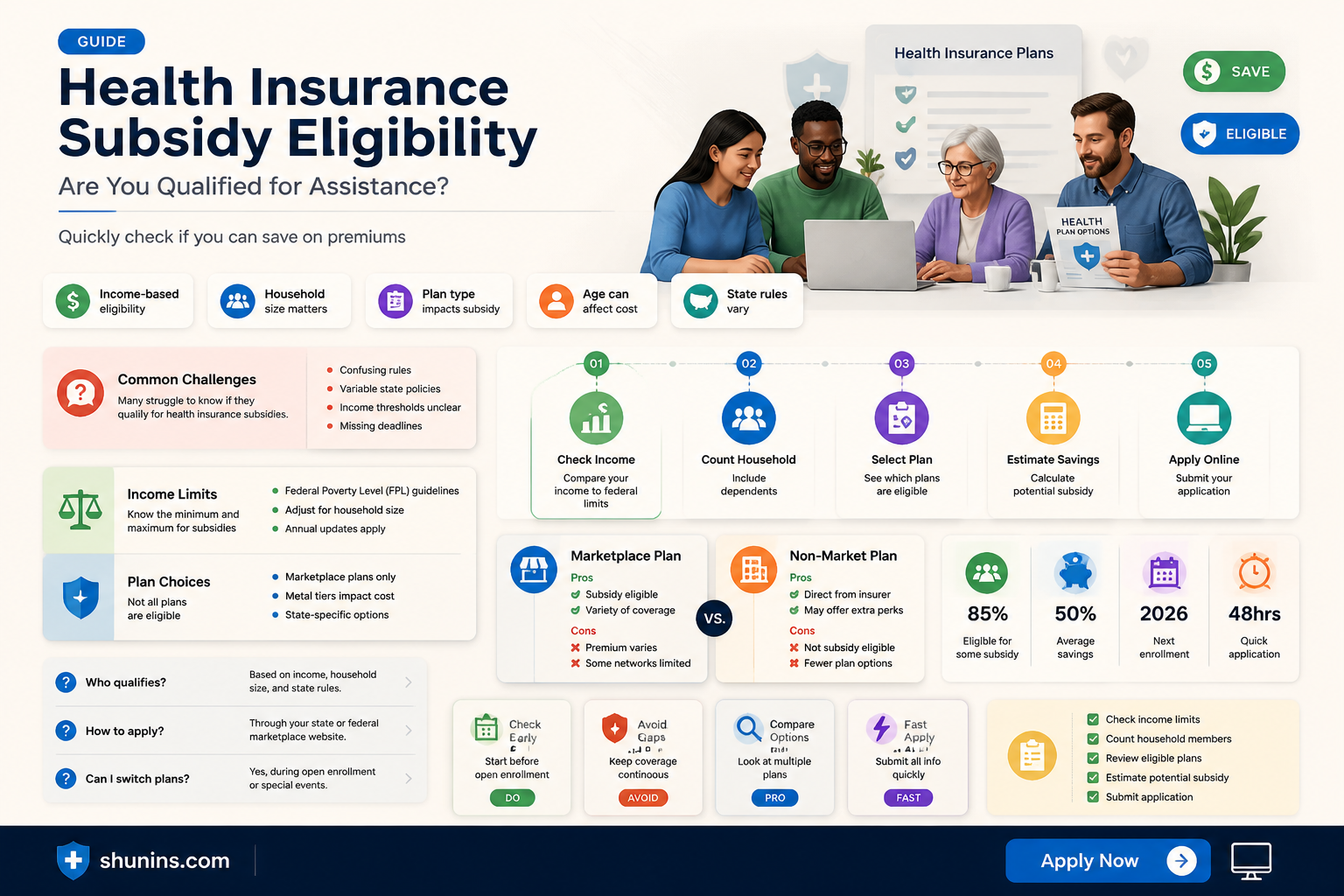

Navigating the complexities of health insurance can be daunting, especially when it comes to understanding eligibility for subsidies. Health insurance subsidies are financial assistance programs designed to help individuals and families with lower incomes afford health coverage. Eligibility for these subsidies typically depends on factors such as household income, family size, and the cost of insurance in your area. To determine if you qualify, you’ll need to compare your income to the Federal Poverty Level (FPL) guidelines and check if your state has expanded Medicaid. Additionally, if you purchase insurance through the Health Insurance Marketplace, you may be eligible for premium tax credits if your income falls within a specific range. It’s essential to review the latest regulations and use online tools or consult with a healthcare navigator to assess your eligibility accurately.

Explore related products

What You'll Learn

![]()

Income Limits for Subsidies

Income limits for health insurance subsidies are not one-size-fits-all. They vary by household size, location, and the federal poverty level (FPL) for the current year. For 2023, individuals earning between 100% and 400% of the FPL may qualify for premium tax credits through the Affordable Care Act (ACA) marketplace. For a single person, this translates to an annual income range of roughly $13,590 to $54,360. Families of four must fall between $27,750 and $111,000. However, these figures are adjusted annually, so it’s crucial to check the latest thresholds before applying.

Consider a practical example: a 35-year-old living in Texas with an annual income of $30,000. Since this falls within the 100% to 400% FPL range, they’re likely eligible for a subsidy. However, the exact amount depends on the benchmark plan in their area and how their income compares to the FPL. Using the healthcare.gov subsidy calculator can provide a quick estimate, but understanding the income brackets is the first step in determining eligibility.

For those near the upper income limit, small fluctuations in earnings can affect subsidy eligibility. For instance, a household of three earning $80,000 might qualify, but an increase to $85,000 could push them above the 400% FPL threshold, eliminating their subsidy. To avoid surprises, track income changes throughout the year and report them promptly to the marketplace. This ensures accurate subsidy calculations and prevents potential repayment of excess credits at tax time.

Beyond the ACA, some states have expanded Medicaid to cover individuals earning up to 138% of the FPL. For example, in California, a single adult earning up to $18,754 annually may qualify for Medicaid. However, states like Texas have not expanded Medicaid, leaving a coverage gap for those earning below 100% FPL but too much for traditional Medicaid. Understanding these state-specific variations is essential for navigating subsidy and coverage options effectively.

Finally, income limits aren’t the only factor in subsidy eligibility. Factors like immigration status, access to employer-sponsored insurance, and household composition also play a role. For instance, if an employer’s plan costs more than 9.12% of household income, individuals may still qualify for marketplace subsidies. Always review the full eligibility criteria and consult resources like healthcare.gov or a certified navigator to ensure you’re maximizing available benefits.

Why Insurance Companies Conduct Audits: Understanding the Process and Purpose

You may want to see also

Explore related products

![]()

Household Size Impact

Your household size is a critical factor in determining eligibility for health insurance subsidies. The Affordable Care Act (ACA) uses your Modified Adjusted Gross Income (MAGI) relative to the Federal Poverty Level (FPL) to assess subsidy eligibility. However, the FPL isn’t a static number—it scales with household size. For example, in 2023, the FPL for an individual is $14,580, but for a family of four, it jumps to $30,000. This means larger households can have higher incomes and still qualify for subsidies, as the income threshold increases proportionally.

Consider a family of three earning $50,000 annually. At first glance, this might seem too high for assistance. However, since the FPL for a family of three is $21,960, their income is 227% of the FPL. Under ACA guidelines, households earning between 100% and 400% of the FPL qualify for premium tax credits. This family falls squarely within that range, making them eligible for subsidies that could significantly reduce their monthly premiums.

The impact of household size extends beyond income thresholds—it also affects the subsidy amount. The ACA’s subsidy formula considers both income and the cost of a benchmark plan (the second-lowest-cost Silver plan in your area). Larger households often face higher benchmark plan costs, which can result in larger subsidies. For instance, a family of five might receive a subsidy that covers 70% of their premium costs, while a single individual with the same income percentage might only get 60% coverage.

Practical tip: When applying for subsidies, ensure your household size is accurately reported. Include all dependents, such as children under 26 or elderly relatives living with you, even if they don’t need coverage. This not only maximizes your eligibility but also ensures the subsidy calculation reflects your true financial situation.

In summary, household size isn’t just a number—it’s a lever that can significantly influence your eligibility and subsidy amount. Understanding how it interacts with income thresholds and benchmark plan costs empowers you to navigate the system effectively. Whether you’re a single parent or part of a multi-generational household, this factor could be the key to unlocking affordable health insurance.

Navigating Medical Insurance Claims in the USA

You may want to see also

Explore related products

![]()

ACA Marketplace Eligibility

To determine if you qualify for a health insurance subsidy through the Affordable Care Act (ACA) Marketplace, understanding the eligibility criteria is crucial. The ACA, also known as Obamacare, provides financial assistance to individuals and families who meet specific income requirements. The primary factor is your household income relative to the Federal Poverty Level (FPL). For 2023, individuals earning between 100% and 400% of the FPL are eligible for premium tax credits. For a family of four, this translates to an annual income range of approximately $28,000 to $112,000. However, eligibility isn’t solely based on income; you must also not have access to affordable employer-sponsored insurance and be a U.S. citizen or lawfully present immigrant.

Let’s break down the steps to assess your eligibility. First, calculate your household income and compare it to the current FPL guidelines, which are updated annually. Tools like the Healthcare.gov subsidy calculator can simplify this process. Second, verify that the health insurance offered by your employer, if any, meets the ACA’s affordability standards—it should cost no more than 9.12% of your household income for the employee’s coverage in 2023. If it exceeds this threshold, you may qualify for subsidies. Third, ensure you’re not eligible for Medicaid or Medicare, as these programs typically disqualify you from ACA subsidies.

A common misconception is that subsidies are only for low-income individuals. In reality, middle-income households often benefit significantly. For example, a family of three earning $75,000 annually may still qualify for a premium tax credit, reducing their monthly premiums by hundreds of dollars. Additionally, cost-sharing reductions (CSRs) are available for those earning up to 250% of the FPL, lowering out-of-pocket costs like deductibles and copayments. These reductions are only available through Silver-tier plans, so selecting the right plan is essential.

Practical tips can streamline your application process. Gather all necessary documents, including income verification (W-2s, tax returns) and immigration status proof if applicable. Apply during the Open Enrollment Period, typically from November 1 to January 15, unless you qualify for a Special Enrollment Period due to life events like marriage or job loss. If your income fluctuates, estimate conservatively to avoid repaying excess subsidies at tax time. Finally, consider consulting a navigator or broker for personalized guidance, especially if your financial situation is complex.

In conclusion, ACA Marketplace eligibility hinges on income, citizenship status, and the affordability of available employer coverage. By understanding these criteria and leveraging available tools, you can maximize your chances of securing a subsidy. Remember, the goal is not just to enroll in a plan but to find one that balances affordability and comprehensive coverage. Take the time to explore your options—it could save you thousands of dollars annually.

When Does Health Insurance Begin at Your New Job?

You may want to see also

Explore related products

![[Self-Adhesive Wall Repair] S Self-Adhesive Fibre Mesh Wall Repair Subsidy | Drywall Repair Tool for Ceiling and Wall Crack Fixing - Easy Installation](https://m.media-amazon.com/images/I/61NW97HSTkL._AC_UY218_.jpg)

![]()

Citizenship Requirements

Citizenship status plays a pivotal role in determining eligibility for health insurance subsidies, particularly in the United States under the Affordable Care Act (ACA). To qualify for premium tax credits or cost-sharing reductions, individuals must be either U.S. citizens, nationals, or lawfully present immigrants. Undocumented immigrants are explicitly excluded from these subsidies, though they may purchase unsubsidized plans on the marketplace. This requirement ensures compliance with federal immigration laws while extending financial assistance to those legally residing in the country.

For lawfully present immigrants, eligibility for subsidies depends on specific immigration statuses. For instance, lawful permanent residents (green card holders), refugees, asylees, and individuals granted withholding of deportation are generally eligible. However, there’s a five-year waiting period for certain immigrants, such as those with green cards, before they can access Medicaid or Children’s Health Insurance Program (CHIP) benefits, though they may still qualify for marketplace subsidies during this period. Understanding these distinctions is crucial for navigating the application process effectively.

Proving citizenship or lawful presence is a critical step in the subsidy application process. Applicants must provide documentation such as a U.S. passport, birth certificate, naturalization certificate, or immigration documents like an I-551 stamp or I-94 form. Inaccurate or incomplete documentation can delay approval or result in denial of subsidies. It’s advisable to gather all necessary documents beforehand and double-check their validity to streamline the process.

While citizenship requirements are clear-cut, exceptions and nuances exist. For example, Native Americans, regardless of their income, may qualify for additional benefits through the Indian Health Service. Similarly, certain lawfully present immigrants, such as victims of trafficking or domestic violence, may be exempt from the five-year waiting period for Medicaid. These exceptions highlight the importance of consulting resources like Healthcare.gov or a certified enrollment counselor to explore all available options.

In summary, citizenship requirements are a cornerstone of health insurance subsidy eligibility, but they are not without complexity. By understanding the specific criteria for U.S. citizens, nationals, and lawfully present immigrants, as well as the documentation needed and potential exceptions, individuals can better position themselves to secure the financial assistance they need. This knowledge empowers applicants to navigate the system confidently and access affordable healthcare coverage.

Top Insurers for Tesla Vehicles: Comprehensive Coverage Options Revealed

You may want to see also

Explore related products

![]()

Employer Coverage Effect

The availability of employer-sponsored health insurance can significantly impact your eligibility for subsidies under the Affordable Care Act (ACA). If your employer offers coverage that meets certain standards, you may not qualify for premium tax credits on the ACA marketplace, even if your income would otherwise make you eligible. This is because the ACA prioritizes employer-based insurance as the primary source of coverage for working individuals.

Understanding the Employer Coverage Effect

The ACA defines "affordable" employer coverage as costing no more than 9.83% of your household income for the employee's share of the premium for self-only coverage in 2023. If your employer's plan meets this affordability threshold and provides minimum value (covering at least 60% of expected healthcare costs), you're generally ineligible for subsidies. This rule aims to prevent individuals from dropping employer coverage for potentially cheaper marketplace plans with subsidies.

Navigating the Nuances

It's crucial to carefully evaluate your employer's plan details. Even if the self-only coverage is affordable, family coverage might not be. In such cases, you may still qualify for subsidies to help cover your dependents' premiums on the marketplace. Additionally, if your employer's plan doesn't meet the minimum value requirement, you can explore marketplace options and potentially receive subsidies.

Strategic Considerations

If you're close to the income threshold for subsidy eligibility, consider the following:

- Spousal Coverage: If your spouse's employer offers more affordable coverage, enrolling in their plan might make you ineligible for subsidies.

- Part-Time Work: Working part-time might reduce your income to a level where employer coverage becomes unaffordable, opening up subsidy eligibility.

- Early Retirement: Retiring before age 65 and losing employer coverage can make you eligible for marketplace subsidies until Medicare eligibility begins.

Seeking Professional Guidance

Given the complexities of the Employer Coverage Effect, consulting a certified insurance broker or utilizing online subsidy calculators can be invaluable. They can help you accurately assess your eligibility based on your specific circumstances, ensuring you make informed decisions about your healthcare coverage. Remember, understanding this effect is crucial for maximizing your access to affordable health insurance.

The High Cost of Individual Medical Insurance Plans

You may want to see also

Frequently asked questions

Eligibility for health insurance subsidies is primarily based on income and household size. Generally, individuals and families earning between 100% and 400% of the Federal Poverty Level (FPL) may qualify for subsidies through the Health Insurance Marketplace.

To determine eligibility, calculate your Modified Adjusted Gross Income (MAGI) and compare it to the current Federal Poverty Level guidelines. You can use the Marketplace’s subsidy calculator or consult with a navigator for assistance.

If your employer offers affordable health insurance that meets minimum value standards, you are generally not eligible for subsidies through the Marketplace. However, if the employer’s plan is unaffordable or doesn’t meet minimum requirements, you may qualify for subsidies.

While U.S. citizens and lawfully present immigrants are eligible for subsidies, undocumented immigrants are not. Some states may offer separate assistance programs regardless of immigration status, but federal subsidies are restricted to those with lawful status.