The uncertainty surrounding the potential loss of health insurance can be a significant source of stress and anxiety for many individuals and families. Whether due to changes in employment, shifts in policy regulations, or other unforeseen circumstances, the prospect of losing coverage raises important questions about financial stability, access to care, and overall well-being. Understanding the factors that may impact your health insurance status, such as job transitions, policy renewals, or legislative changes, is crucial in navigating this complex issue. Additionally, exploring alternative options, such as COBRA, private plans, or government-sponsored programs, can provide a sense of security and preparedness during this uncertain time. Addressing these concerns proactively can help mitigate risks and ensure continued access to essential healthcare services.

Explore related products

What You'll Learn

- Understanding Policy Changes: Review updates to your insurance plan for any alterations affecting coverage or eligibility

- Job Transition Impact: Assess how changing jobs or losing employment might affect your current health insurance status

- Age or Life Events: Consider how aging or life milestones (e.g., marriage, divorce) influence insurance eligibility

- Premium Payment Issues: Ensure timely payments to avoid policy lapses or termination due to missed premiums

- Legal or Policy Expiry: Check for legal changes or policy expiration dates that could end your coverage

![]()

Understanding Policy Changes: Review updates to your insurance plan for any alterations affecting coverage or eligibility

Health insurance policies aren’t static; they evolve annually through updates that can alter coverage, eligibility, or costs. Ignoring these changes may lead to unexpected gaps in care or financial strain. For instance, a plan might drop a specific prescription drug from its formulary, shift a preferred provider out of network, or introduce new eligibility criteria tied to income or employment status. Proactively reviewing these updates ensures you’re prepared for such shifts and can take corrective action before they impact your healthcare access.

Begin by locating your plan’s *Summary of Benefits and Coverage (SBC)*, typically sent annually by your insurer or employer. This document outlines key changes in plain language, including modifications to premiums, deductibles, copays, and covered services. Pay close attention to sections detailing exclusions or limitations, as these often house the most impactful updates. For example, a plan might reduce coverage for mental health visits from unlimited to 20 sessions per year, a change that could significantly affect someone with ongoing therapy needs.

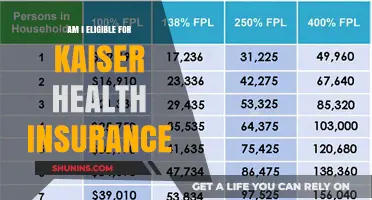

If you’re enrolled in a marketplace plan or Medicaid, eligibility changes tied to income or household size can trigger a loss of coverage. For instance, a $5,000 raise might push you above the income threshold for Medicaid, while a marketplace plan could become unaffordable if subsidies decrease. Use the annual open enrollment period to reassess your eligibility and explore alternative plans. Tools like the Healthcare.gov subsidy calculator can estimate changes in financial assistance based on updated income figures.

Employer-sponsored plans often undergo adjustments during open enrollment, but mid-year changes are also possible. If your employer switches providers, your current medications, specialists, or ongoing treatments might no longer be covered. For example, a switch from PPO to HMO could require you to select a primary care physician and obtain referrals for specialist visits. Review any *Summary Plan Description (SPD)* provided by your employer to understand these shifts and their implications for your care.

Finally, don’t overlook the power of direct communication. If policy language feels ambiguous, contact your insurer’s customer service line or your HR department for clarification. Ask specific questions, such as, “Will my current asthma medication still be covered under the new formulary?” or “How does the change in network status affect my ability to see my cardiologist?” Document these conversations, including dates and representative names, to reference if disputes arise later. Staying informed and proactive transforms policy changes from potential threats into manageable adjustments.

Liberty Mutual vs. State Farm: Which Insurance Provider is Better?

You may want to see also

Explore related products

![]()

Job Transition Impact: Assess how changing jobs or losing employment might affect your current health insurance status

Changing jobs or facing unemployment can trigger immediate concerns about health insurance continuity. If your current coverage is employer-sponsored, leaving that job typically means losing access to that plan. Under COBRA, you may continue the same policy for up to 18 months, but you’ll pay the full premium plus an administrative fee—often 102% of the total cost. For a family plan averaging $22,000 annually, this could mean over $22,440 out-of-pocket per year, a steep increase from typical employer-subsidized rates.

However, job transitions also open pathways to alternative coverage. If you’re switching employers, inquire about the new company’s waiting period for health benefits—some start coverage immediately, while others impose delays of 30 to 90 days. During gaps, short-term health plans (lasting up to 364 days) or marketplace plans under the Affordable Care Act (ACA) can bridge coverage. ACA plans offer subsidies if your income falls below 400% of the federal poverty level ($54,360 for an individual in 2023), potentially reducing monthly premiums significantly.

Losing a job qualifies you for a Special Enrollment Period (SEP) on Healthcare.gov, allowing you to enroll in an ACA plan outside the annual open enrollment window. Act within 60 days of losing coverage to avoid gaps. Medicaid is another option if your income drops below state-specific thresholds (e.g., $20,120 for an individual in states expanding Medicaid). Eligibility varies, but the application process is year-round, providing immediate relief for those who qualify.

For freelancers or those joining companies without benefits, consider joining a spouse’s plan or purchasing individual coverage. Compare costs carefully—a Bronze ACA plan might offer lower premiums ($300–$400/month) with higher deductibles, while Gold plans ($500–$700/month) provide better cost-sharing. Use tools like Healthcare.gov’s subsidy calculator to estimate expenses and ensure compliance with the individual mandate, avoiding tax penalties for lacking coverage.

Finally, document all transitions meticulously. Notify your insurer of job changes, retain proof of prior coverage (e.g., COBRA election notices), and track enrollment deadlines. Missteps can lead to denied claims or coverage lapses. Proactive planning—whether through COBRA, ACA, Medicaid, or private plans—ensures continuity in healthcare access during turbulent employment shifts.

Emergency Room Visits: Medical Insurance Coverage Explained

You may want to see also

Explore related products

$164.06 $245.95

![]()

Age or Life Events: Consider how aging or life milestones (e.g., marriage, divorce) influence insurance eligibility

Aging and life milestones can significantly alter your health insurance landscape, often in ways you might not anticipate. For instance, turning 26 means you’re no longer eligible to stay on a parent’s health plan, unless you qualify as a dependent under specific IRS rules. This age-based cutoff forces many young adults to seek alternative coverage, whether through an employer, the Health Insurance Marketplace, or a short-term plan. Similarly, reaching age 65 opens the door to Medicare eligibility, but it also requires careful planning to avoid gaps in coverage or penalties for late enrollment. Understanding these age-specific thresholds is crucial to maintaining continuous insurance.

Life events like marriage or divorce act as catalysts for insurance changes, often triggering special enrollment periods (SEPs) outside the typical open enrollment window. Getting married allows you to join your spouse’s employer-sponsored plan or add them to yours, provided you do so within 30 to 60 days of the event. Conversely, divorce can lead to the loss of coverage if you were previously on your ex-spouse’s plan. In this case, you have 60 days to enroll in a new plan through the Marketplace or COBRA, which temporarily extends your existing coverage but often at a higher cost. Failing to act within these timelines can leave you uninsured until the next open enrollment period.

Retirement marks another critical juncture, as leaving an employer-sponsored plan requires a transition to Medicare, a private plan, or COBRA. If you retire before age 65, you’ll need to secure coverage through the Marketplace or a spouse’s plan until Medicare eligibility kicks in. Retiring at or after 65 involves coordinating Medicare Part A, Part B, and potentially a supplemental Medigap or Medicare Advantage plan. Missteps here, such as delaying Part B enrollment, can result in lifelong penalties and coverage gaps. Early planning, including estimating healthcare costs in retirement, is essential to avoid financial strain.

Practical tips for navigating these transitions include keeping detailed records of life events and their dates, as insurers often require documentation to process SEP requests. Additionally, familiarize yourself with the specifics of COBRA, which can provide temporary coverage but is typically more expensive than Marketplace plans. For those nearing Medicare age, attend informational sessions or consult a licensed insurance broker to understand your options. Finally, leverage online tools like the Healthcare.gov subsidy calculator to estimate costs and determine if you qualify for financial assistance during transitions. Proactive management of these age and life-event triggers ensures you remain insured without unnecessary expenses.

How Insurance Companies Control Healthcare Decisions and Patient Outcomes

You may want to see also

Explore related products

![]()

Premium Payment Issues: Ensure timely payments to avoid policy lapses or termination due to missed premiums

Missed premium payments are the most common reason for health insurance policy lapses or terminations. Unlike a forgotten utility bill, the consequences here extend far beyond a late fee. A single missed payment can trigger a cascade of issues, from a temporary loss of coverage to a permanent termination of your policy, leaving you vulnerable to unexpected medical expenses.

Understanding the gravity of this situation is crucial. Health insurance companies operate on a system of pooled risk, relying on consistent premium payments to cover the costs of claims. When payments are missed, it disrupts this delicate balance, forcing insurers to take action to protect their financial stability.

The Slippery Slope of Missed Payments:

Think of premium payments as the foundation of your health insurance coverage. Each missed payment weakens this foundation, increasing the risk of collapse. Most policies have a grace period, typically 30 days, during which you can make a late payment without penalty. However, exceeding this grace period can lead to policy suspension, meaning your coverage is temporarily halted. If payments remain outstanding, the insurer may ultimately terminate your policy entirely, leaving you uninsured.

This scenario is particularly perilous for individuals with pre-existing conditions or those requiring ongoing medical care. Reinstating a terminated policy can be difficult and often comes with higher premiums or exclusions for pre-existing conditions.

Proactive Measures to Avoid Lapses:

- Set Up Automatic Payments: Most insurers offer automatic payment options, ensuring your premiums are deducted directly from your bank account or credit card on the due date. This eliminates the risk of forgetting to pay and provides peace of mind.

- Utilize Payment Reminders: Many insurers send email or text reminders before your payment is due. Take advantage of these reminders and set up additional alerts on your calendar or phone to ensure you don't miss the deadline.

- Communicate with Your Insurer: If you're facing financial difficulties and anticipate difficulty making a payment, contact your insurer immediately. They may be able to offer payment plans or temporary extensions to help you avoid a lapse in coverage.

- Review Your Policy Carefully: Understand the grace period and termination procedures outlined in your policy. Knowing the specific timelines and consequences will empower you to take proactive steps to prevent a lapse.

The Cost of Inaction:

The consequences of a policy lapse extend far beyond the immediate loss of coverage. Reinstating a lapsed policy often involves paying back missed premiums, potentially with penalties or late fees. Additionally, you may face a waiting period before coverage resumes, leaving you vulnerable during that time. In some cases, a lapse can even lead to higher premiums upon reinstatement, as insurers may view you as a higher risk.

The most significant cost, however, is the potential for being left without health insurance when you need it most. Medical emergencies can be financially devastating, and being uninsured can lead to overwhelming debt and long-term financial hardship.

Timely premium payments are the lifeblood of your health insurance coverage. By understanding the consequences of missed payments and implementing proactive measures, you can safeguard your policy and ensure continuous protection for yourself and your loved ones. Remember, communication with your insurer is key – don't hesitate to reach out if you're facing financial challenges. Taking these steps will help you avoid the costly and stressful consequences of a policy lapse.

Will AAA Contact the Other Insurance Company After an Accident?

You may want to see also

Explore related products

![]()

Legal or Policy Expiry: Check for legal changes or policy expiration dates that could end your coverage

Health insurance policies aren't eternal contracts. They operate within a legal framework subject to change and have defined expiration dates. Ignoring these realities can leave you vulnerable to unexpected coverage gaps.

Think of it like a lease agreement: you wouldn't assume your apartment rental continues indefinitely without checking the lease terms. The same vigilance applies to your health insurance.

Understanding Legal Shifts: Government policies and regulations surrounding healthcare are constantly evolving. Changes in laws can directly impact your coverage. For instance, modifications to the Affordable Care Act (ACA) could alter eligibility criteria, benefit structures, or even the availability of certain plans. Stay informed by subscribing to updates from reputable healthcare news sources or directly from government agencies like Healthcare.gov.

Even seemingly minor legal tweaks can have significant consequences. A change in the definition of a pre-existing condition, for example, could affect your ability to maintain coverage or the cost of your premiums.

Policy Expiration Dates: Not Just for Milk Cartons Every health insurance policy has a defined term, typically a year. Mark your calendar with your policy's expiration date and initiate renewal discussions with your provider well in advance. Don't wait until the last minute, as processing times can vary. Some insurers offer automatic renewal options, but it's crucial to review the terms carefully. Automatic renewals might come with premium increases or changes in coverage, so don't assume continuity without scrutiny.

Proactive Steps to Avoid Lapses:

- Review Your Policy Annually: Treat your annual policy review as a non-negotiable health checkup. Scrutinize the fine print for any changes in coverage, exclusions, or renewal procedures.

- Stay Informed: Follow reputable healthcare news sources and government websites to stay abreast of legal changes that could impact your coverage.

- Communicate with Your Insurer: Don't hesitate to contact your insurance provider with questions or concerns. They are obligated to provide clear information about your policy and any upcoming changes.

- Explore Alternatives: If your current policy is expiring or facing significant changes, research alternative plans. Compare coverage, costs, and provider networks to find the best fit for your needs.

Remember, being proactive about understanding legal changes and policy expiration dates is crucial for maintaining continuous health insurance coverage. Don't let bureaucratic details catch you off guard.

Medicaid-Friendly Pharmacies in Indiana: A Comprehensive Guide

You may want to see also

Frequently asked questions

Not necessarily. You can explore options like COBRA, your new employer’s plan, or the Health Insurance Marketplace to maintain coverage during transitions.

Yes, failing to pay premiums on time can result in loss of coverage, though insurers typically provide a grace period before termination.

If you were covered under your spouse’s plan, you may lose coverage after divorce. You can enroll in an individual plan or explore options like COBRA.

If your income changes, you may no longer qualify for certain subsidies or Medicaid. However, you can update your information on the Marketplace to find alternative coverage.

If you retire before 65, you may lose employer-sponsored coverage. Options include COBRA, private plans, or early retirement health insurance until Medicare eligibility.