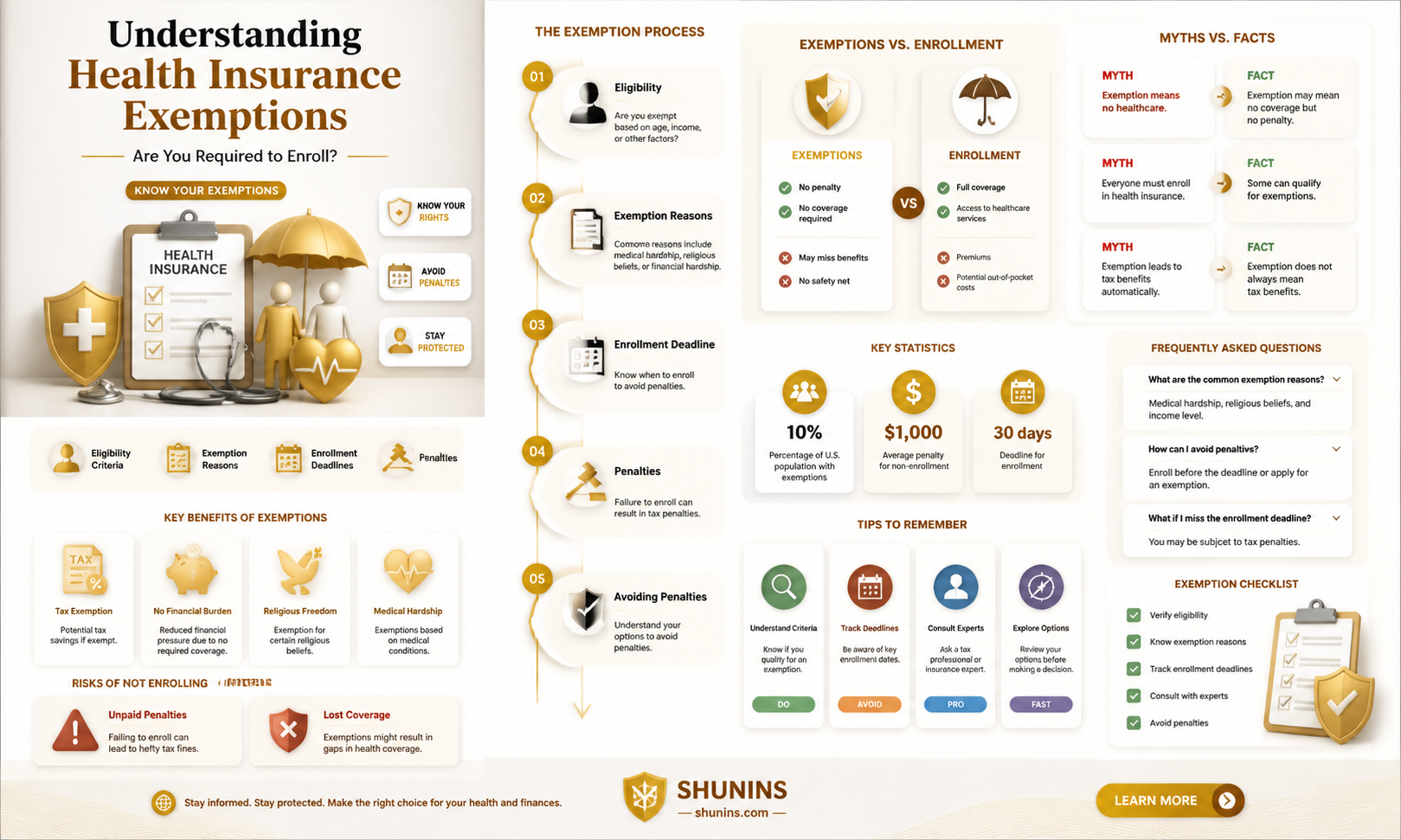

Navigating the complexities of health insurance requirements can be daunting, leaving many to wonder, Am I exempt from having health insurance? Understanding exemptions is crucial, as they vary based on factors like income, citizenship status, religious beliefs, or membership in certain groups such as Native American tribes. Additionally, some individuals may qualify for hardship exemptions if affording coverage would cause financial strain. While the Affordable Care Act (ACA) mandates most Americans to have health insurance or pay a penalty, specific circumstances can waive this obligation. Exploring these exemptions requires careful consideration of personal situations and adherence to legal guidelines, ensuring compliance while avoiding unnecessary penalties.

Explore related products

What You'll Learn

- Religious Exemptions: Certain faiths may qualify for exemptions from health insurance mandates

- Financial Hardship: Low income or high costs can exempt individuals from penalties

- Short Coverage Gaps: Brief periods without insurance may not incur penalties

- Non-Citizen Status: Some non-citizens are exempt from health insurance requirements

- Member-Share Programs: Health care sharing ministries can qualify as exemptions

![]()

Religious Exemptions: Certain faiths may qualify for exemptions from health insurance mandates

In the United States, the Affordable Care Act (ACA) mandates that most individuals have health insurance or pay a penalty, but certain religious groups can claim exemption. This exemption applies to those who are members of recognized religious sects with religious objections to insurance, including medical care provided by the government or private insurers. To qualify, individuals must formally request an exemption by filing Form 8965 with their federal tax return, providing documentation of their religious affiliation and objections. This exemption is not automatic; it requires active participation and adherence to specific IRS guidelines.

Consider the case of the Amish, a religious group known for their simple living and self-sufficiency. Many Amish communities rely on mutual aid societies instead of traditional insurance, pooling resources to cover medical expenses. The IRS recognizes this practice as a valid basis for exemption, provided it has been continuously maintained since December 31, 2014. Other faiths, such as certain Christian Scientists who rely on prayer for healing, may also qualify if they can demonstrate consistent adherence to their beliefs. The key is proving that the objection to insurance is rooted in longstanding religious practice, not personal preference or financial convenience.

However, claiming a religious exemption is not without risks. Exempt individuals forgo the financial protections of insurance, leaving them vulnerable to catastrophic medical expenses. For example, a major surgery or chronic illness could result in significant out-of-pocket costs. Additionally, the exemption does not cover dependents, meaning family members may still be subject to the individual mandate unless they also qualify. Before pursuing this route, individuals should carefully weigh the ideological benefits against the practical consequences, possibly consulting a tax professional or legal advisor to ensure compliance with IRS rules.

To successfully claim a religious exemption, follow these steps: 1) Confirm your religious sect’s eligibility by reviewing IRS criteria. 2) Gather documentation, such as church membership records or statements from religious leaders, to prove your affiliation and objections. 3) Complete Form 8965 accurately, detailing your religious practices and how they conflict with insurance. 4) File the form with your tax return annually to maintain exemption status. Remember, this exemption is not a loophole but a provision for those whose faith genuinely prohibits insurance participation. Misuse can result in penalties, so honesty and thoroughness are essential.

In conclusion, religious exemptions from health insurance mandates offer a pathway for those whose faith conflicts with insurance requirements, but they demand careful consideration and adherence to strict guidelines. By understanding the specifics—such as the need for continuous practice since 2014 and the exclusion of dependents—individuals can make informed decisions. While this exemption preserves religious freedom, it also shifts financial risk onto the individual, making it a choice that balances spiritual conviction with practical reality. For those who qualify, it is a testament to the intersection of faith and law in modern society.

Cheapest Full-Time RV Insurance Rates: Top Companies Compared

You may want to see also

Explore related products

![]()

Financial Hardship: Low income or high costs can exempt individuals from penalties

Financial hardship can be a legitimate reason for individuals to seek exemption from health insurance penalties. The Affordable Care Act (ACA) recognizes that for some, the cost of insurance premiums, even with subsidies, may still be prohibitively expensive. This is where the concept of the affordability exemption comes into play. If the cheapest available health plan in your area would cost more than 8.5% of your household income, you may qualify for this exemption. To determine eligibility, you’ll need to compare your income to the federal poverty level (FPL) and calculate the premium for the lowest-cost bronze plan in your region. For instance, if your income is $25,000 and the cheapest plan costs $2,125 annually (8.5% of $25,000), you’d be exempt from the penalty.

Navigating this exemption requires careful documentation and planning. Start by gathering proof of income, such as tax returns or pay stubs, and use the Healthcare.gov subsidy calculator to estimate your premium costs. If you find that the cheapest plan exceeds the 8.5% threshold, you can apply for the exemption directly through the marketplace or when filing your taxes. Keep in mind that this exemption is not automatic; you must actively claim it. Additionally, if your income fluctuates during the year, monitor your eligibility quarterly to avoid unexpected penalties.

A comparative analysis reveals that low-income individuals often face a Catch-22: they need health insurance but cannot afford it, even with subsidies. For example, a single adult earning $18,000 annually might qualify for a premium tax credit but still find the remaining cost burdensome. In contrast, someone earning just above the Medicaid eligibility threshold in their state may fall into the "coverage gap," where they earn too much for Medicaid but too little to afford private insurance. In such cases, the affordability exemption serves as a critical safety net, ensuring that financial hardship doesn’t compound into legal penalties.

Persuasively, it’s worth noting that this exemption isn’t just a loophole—it’s a recognition of economic reality. High healthcare costs disproportionately affect low-income households, often forcing them to choose between insurance and basic necessities like rent or groceries. By allowing exemptions based on financial hardship, the ACA acknowledges that access to healthcare should not come at the expense of overall well-being. However, critics argue that this approach may discourage enrollment, potentially undermining the broader goals of the ACA. The takeaway? While the exemption provides relief, it also highlights the need for more comprehensive solutions to make healthcare truly affordable for all.

Practically, if you’re facing financial hardship, take proactive steps to explore all available options. Beyond the affordability exemption, consider Medicaid, short-term health plans, or community health centers for low-cost care. For those with slightly higher incomes, health savings accounts (HSAs) paired with high-deductible plans can offer flexibility. Finally, stay informed about policy changes, as eligibility criteria and thresholds may evolve. Financial hardship doesn’t have to mean forgoing healthcare—it means finding the right path to protection within your means.

Medicaid Eligibility: Subsidies for Health Insurance Coverage?

You may want to see also

Explore related products

![]()

Short Coverage Gaps: Brief periods without insurance may not incur penalties

Brief lapses in health insurance coverage, often referred to as short coverage gaps, can occur due to life transitions such as changing jobs, moving, or waiting for a new policy to take effect. These gaps, typically lasting less than three consecutive months, may not trigger penalties under the Affordable Care Act (ACA). The ACA’s individual mandate includes a "short coverage gap exemption," which allows individuals to go without insurance for less than three months without facing a tax penalty. This provision acknowledges the practical realities of navigating insurance transitions and provides a buffer for those who experience temporary disruptions in coverage.

Understanding the specifics of this exemption is crucial for avoiding unnecessary financial strain. For instance, if you lose your job and COBRA coverage is too expensive, you might go uninsured for a month while waiting for a new employer’s plan to begin. This one-month gap would qualify for the exemption. However, if you remain uninsured for three months or more, you could face penalties unless you qualify for another exemption. Tracking your coverage timeline is essential—mark key dates on a calendar or set reminders to ensure you stay within the three-month window.

A comparative analysis of short coverage gaps versus longer lapses highlights the importance of minimizing uninsured periods. While a two-month gap might be exempt, a four-month gap could result in penalties unless you meet other exemption criteria, such as experiencing a hardship or having income below the tax filing threshold. Additionally, some states have their own insurance mandates, so even if you avoid federal penalties, you might still face state-level consequences. For example, California, New Jersey, and Massachusetts impose penalties for residents without coverage, regardless of the duration of the gap.

Practical tips for managing short coverage gaps include exploring temporary insurance options, such as short-term health plans or COBRA coverage, even if only for a month or two. Short-term plans, while limited in benefits, can provide a safety net during transitions. Another strategy is to align life changes with open enrollment periods or qualifying life events to minimize gaps. For example, if you’re leaving a job, coordinate your new insurance start date to overlap with your old plan’s end date. Finally, consult a tax professional or use online tools to confirm your eligibility for the short coverage gap exemption, ensuring compliance with both federal and state regulations.

In conclusion, short coverage gaps of less than three months offer a reprieve from ACA penalties, but proactive management is key. By understanding the rules, tracking your coverage timeline, and exploring temporary insurance options, you can navigate transitions without unnecessary financial or health risks. This exemption is a practical acknowledgment of life’s unpredictability, but it requires vigilance to stay within its parameters.

Optometrists and Medical Insurance: What's Covered and What's Not

You may want to see also

Explore related products

![]()

Non-Citizen Status: Some non-citizens are exempt from health insurance requirements

Non-citizens in the United States often face unique challenges when navigating health insurance requirements. While the Affordable Care Act (ACA) mandates that most individuals have health coverage, certain non-citizen categories are exempt from this rule. Understanding these exemptions is crucial for avoiding unnecessary penalties and ensuring compliance with federal regulations.

Categories of Exempt Non-Citizens:

- Undocumented Immigrants: Undocumented individuals are not eligible to purchase health insurance through the ACA Marketplace and are therefore exempt from the individual mandate. However, they may still access emergency Medicaid in some states.

- Certain Visa Holders: Individuals on specific visa types, such as A, G, and NATO visas (diplomatic and international organization visas), are exempt from the ACA's individual mandate. This exemption also applies to their dependents.

- Individuals with a Short Stay: Non-citizens who are in the U.S. for less than 31 days in a row are exempt from the health insurance requirement.

- Those with Income Below the Tax Filing Threshold: Non-citizens whose income falls below the minimum threshold for filing federal taxes are also exempt from the individual mandate.

Important Considerations:

It's essential to note that exemptions from the individual mandate do not equate to ineligibility for health insurance. Many non-citizens, even those exempt, may still qualify for coverage through employer-sponsored plans, Medicaid (in certain states), or private insurance purchased outside the Marketplace.

Practical Tips:

- Consult an Immigration Attorney: Given the complexities of immigration status and healthcare regulations, consulting an immigration attorney can provide personalized guidance on eligibility and exemptions.

- Explore State-Specific Programs: Some states offer health insurance programs specifically designed for non-citizens, regardless of their exemption status. Researching these options can be beneficial.

- Maintain Documentation: Keep accurate records of your immigration status, income, and any health insurance coverage you obtain. This documentation may be necessary for tax purposes or to demonstrate compliance with regulations.

Understanding the nuances of non-citizen health insurance exemptions is crucial for navigating the U.S. healthcare system effectively. By staying informed and seeking appropriate guidance, non-citizens can make informed decisions about their healthcare coverage and avoid potential penalties.

ER Visits: Which Insurers Allow Balance Billing Practices?

You may want to see also

Explore related products

![]()

Member-Share Programs: Health care sharing ministries can qualify as exemptions

Health care sharing ministries (HCSMs) offer a unique alternative to traditional health insurance, and they can qualify as exemptions from the individual mandate under the Affordable Care Act (ACA). These member-share programs are rooted in religious or ethical beliefs, where members pool resources to cover each other’s medical expenses. To qualify for the exemption, the HCSM must meet specific IRS criteria, such as being in existence continuously since December 31, 1999, and sharing medical expenses among members according to established guidelines. If you’re considering this route, verify that the HCSM you’re joining is recognized by the IRS to ensure you’re exempt from penalties.

Joining an HCSM isn’t just about avoiding insurance requirements—it’s a commitment to a community-based approach to healthcare. Members typically pay a monthly share amount, which is then distributed to cover eligible medical expenses of other members. Unlike insurance, HCSMs don’t guarantee coverage for all medical needs; they often exclude pre-existing conditions, mental health services, or certain types of care. Before enrolling, carefully review the program’s guidelines and limitations to ensure it aligns with your healthcare needs and values.

One practical tip for evaluating HCSMs is to compare their cost structure to traditional insurance premiums. While monthly shares may be lower, consider the out-of-pocket costs for uncovered services. For example, if you require frequent specialist visits or prescription medications, an HCSM might not provide sufficient coverage. Additionally, HCSMs often require members to adhere to specific lifestyle standards, such as abstaining from tobacco or alcohol. Assess whether these requirements fit your lifestyle before committing.

A key advantage of HCSMs is their flexibility in sharing expenses across a like-minded community. For instance, some programs allow members to negotiate directly with healthcare providers for discounted rates, which can reduce overall costs. However, this approach requires proactive involvement in managing your healthcare. If you’re comfortable with this level of engagement and align with the program’s values, an HCSM could be a viable exemption option. Always consult with a tax professional or healthcare advisor to ensure compliance with legal requirements.

In conclusion, member-share programs through health care sharing ministries can provide a legitimate exemption from the health insurance mandate, but they come with distinct trade-offs. They offer a community-driven, cost-sharing model but lack the comprehensive coverage of traditional insurance. By carefully weighing the benefits, limitations, and personal alignment with HCSM principles, you can determine if this exemption is the right choice for your healthcare and financial needs.

Understanding COBRA Insurance: Coverage and Costs Explained

You may want to see also

Frequently asked questions

You may qualify for a hardship exemption if you cannot afford health insurance, even after financial assistance. This exemption must be applied for through the Health Insurance Marketplace.

Yes, some individuals who are members of recognized religious sects with religious objections to insurance can apply for a religious conscience exemption through the Health Insurance Marketplace.

Yes, U.S. citizens living abroad for at least 330 days per year are exempt from the individual mandate to have health insurance.

Yes, undocumented immigrants are not required to have health insurance under the Affordable Care Act (ACA) and are exempt from the individual mandate.