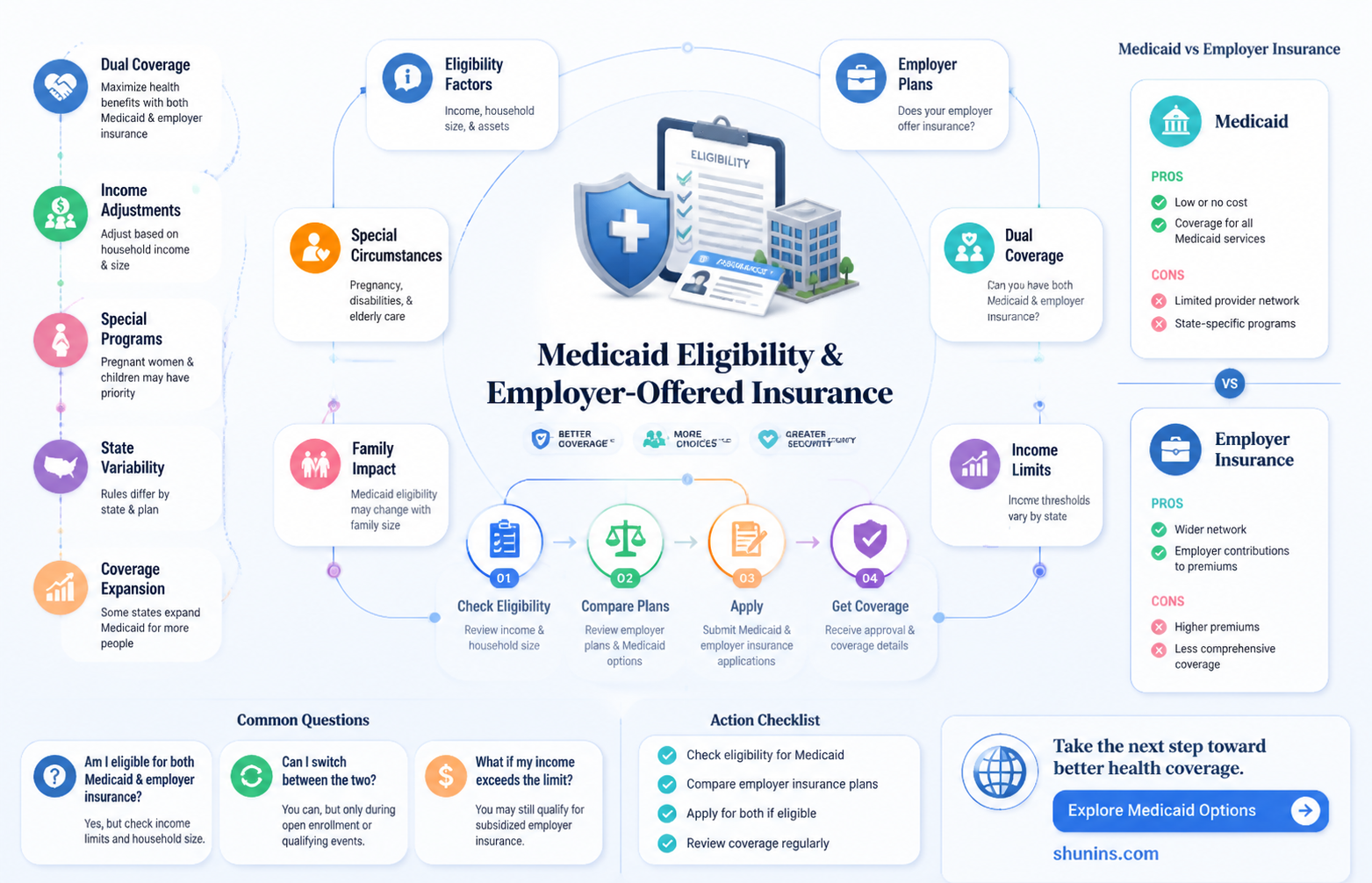

Medicaid eligibility is determined by a variety of factors, including income, age, residency, citizenship, ability, pregnancy, family size, and role in the household. If your employer offers insurance, it is still possible to qualify for Medicaid, as the two are not mutually exclusive. However, it is important to note that Medicaid serves as the last resort payer if you have coverage from another source, and it may not cover copayments charged by your primary insurance provider. Eligibility for Medicaid is based on financial and medical criteria, and applicants can assess their eligibility by considering factors such as income, family size, and residency.

| Characteristics | Values |

|---|---|

| Medicaid eligibility | Based on income, age, residency, citizenship, ability, pregnancy, family size, and role in the household |

| Employer-sponsored insurance eligibility | Based on affordability, comprehensiveness, and minimum value |

| Affordability | If the cost of coverage is no greater than 9.02% of annual household income |

| Medicaid application | Can be done at any time |

| Medicaid coverage | Varies by state |

| Medicaid as a secondary payer | Covers smaller amounts like coinsurance or co-pay |

Explore related products

What You'll Learn

![]()

Medicaid eligibility and income

Medicaid is a health insurance program that provides coverage for individuals with low incomes. The eligibility criteria for Medicaid vary by state, but there are some general guidelines that apply in most cases. Firstly, individuals must meet certain non-financial eligibility criteria, such as being a resident of the state in which they are applying for Medicaid, and being either a U.S. citizen or a qualified non-citizen. Additionally, some eligibility groups are limited by age, pregnancy, or parenting status.

To determine financial eligibility for Medicaid, states use the Modified Adjusted Gross Income (MAGI) methodology, which considers taxable income and tax filing relationships. The income limits vary depending on factors such as family size, marital status, and the type of Medicaid being applied for. For example, in North Carolina, individuals with incomes up to $1,507 to $4,625 per month, depending on family size, may be eligible for AHCCCS, a Medicaid program for those who are not eligible for other Medicaid programs. In Arizona, individuals with higher incomes may still qualify for Medicaid if they meet certain criteria, such as being pregnant or having a family with children.

It is important to note that Medicaid eligibility is not solely based on income. There are also asset limits and level of care requirements that must be met. Additionally, if an individual's employer offers health insurance, Medicaid may serve as a secondary payer for costs not covered by the primary insurance. However, if the employer-provided insurance is considered unaffordable or does not meet minimum value standards, individuals may be eligible for financial assistance through programs like Maryland Health Connection to lower the cost of coverage.

To determine specific eligibility requirements and income limits, it is recommended to refer to the Medicaid website or contact the relevant state agency, as eligibility rules and income limits may vary by state and change over time.

Understanding Gap Medical Insurance Coverage: Filling the Gaps

You may want to see also

Explore related products

![]()

Employer-provided insurance affordability

If your employer offers health insurance, you may still be eligible for Medicaid. Medicaid eligibility is based on where you live, your income, your age, your residency, your citizenship, your ability, your pregnancy status, your family size, and the role you play in your household. In 2025, a job-based health plan is considered "affordable" if your share of the monthly premium in the lowest-cost plan offered by the employer is less than 9.02% of your household income. If your employer's insurance is considered affordable and provides minimum value, you are not eligible for a government subsidy to purchase your own insurance.

In the state of Arizona, Medicaid is the last resort payer if you have coverage through another agency. If you are 19 or older, you might have to make small copayments for Medicaid-covered services. You will not have to cover copayments if you are 18 or younger, pregnant, in hospice care, or exempt under certain other conditions.

In the state of Maryland, you can purchase a private health plan through Maryland Health Connection if you have employer coverage. You will only be eligible for financial assistance to lower the cost of coverage if your employer coverage is considered unaffordable or does not meet some basic standards, known as providing minimum value. Employer coverage is considered affordable if the cost you pay annually for coverage is no greater than 9.02% of your annual household income.

If you are pregnant or have a family with children, you may earn more and still qualify for Medicaid. Additionally, if you are enrolled in COBRA insurance after losing your job, you can still apply for and enroll in Medicaid at any time. If you qualify for Medicaid, you can drop your COBRA coverage.

Understanding Blue Cross Blue Shield: Medicaid or Medicare?

You may want to see also

Explore related products

$12.99 $12.99

![]()

Medicaid and employer insurance coverage

Medicaid eligibility is determined by factors such as income, age, residency, citizenship, ability, pregnancy, family size, and role within the household. It is not tied to employment status, so one can apply for and enroll in Medicaid at any time, even if they have job-based insurance. However, Medicaid is typically considered the last resort for those who cannot afford other insurance options.

In some cases, individuals with employer-sponsored insurance may still be eligible for Medicaid. This typically occurs when the employer's insurance is deemed unaffordable or insufficient. For instance, in Maryland, employer coverage is considered affordable if the annual cost to the employee does not exceed 9.02% of their annual household income. If the employer's coverage is deemed unaffordable or fails to meet basic standards, individuals may be eligible for financial assistance to supplement their coverage or enroll in Medicaid.

It is important to note that Medicaid eligibility varies by state, and each state offers different plans to cater to the diverse needs of its residents. For example, Arizona's Medicaid program includes ALTCS (Arizona Long-Term Care System), which provides services at little to no cost for the blind, elderly, and disabled. Therefore, it is advisable to research the specific Medicaid programs and requirements of your state.

If you have employer-sponsored insurance but find it inadequate or overly expensive, you may consider purchasing a private health plan through services like Maryland Health Connection. However, you will only be eligible for financial assistance to lower the cost of coverage if your employer's insurance is deemed unaffordable or does not meet minimum value standards.

Lastly, it is worth mentioning that job-based health plans are considered affordable if the employee's share of the monthly premium in the lowest-cost plan is less than 9.02% of their household income. This standard of minimum coverage applies to most job-based health plans, and if met, disqualifies the employee from receiving a premium tax credit if they purchase a Marketplace insurance plan.

The High Cost of Medical Insurance: Why So Expensive?

You may want to see also

Explore related products

![]()

Medicaid eligibility and family

Medicaid eligibility is based on income and family size. It provides health coverage to individuals and families, including children, parents, pregnant women, elderly people with certain incomes, and people with disabilities. In the state of Arizona, Medicaid is the last resort payer if you have coverage through another agency. If your employer offers health insurance, they are also required to provide the same coverage to your children who are 25 or younger. Your spouse may also be allowed to join your health insurance plan, but this is not a legal requirement.

In Utah, Medicaid eligibility was expanded in 2019 to include adults whose annual income is up to 138% of the federal poverty level ($17,608 for an individual or $36,156 for a family of four). The federal government covers 90% of the costs, with the state covering the remaining 10%.

In Maryland, Medicaid applicants can qualify for different types of financial help depending on their income and household size. Pregnant women and families with children may earn more and still qualify. If you have employer coverage, you can purchase a private health plan through Maryland Health Connection. You will only be eligible for financial assistance to lower the cost of coverage if your employer coverage is considered unaffordable or if it does not meet certain basic standards. Employer coverage is considered affordable if the cost you pay annually for coverage is no greater than 9.02% of your annual household income.

In general, if you have job-based coverage, you won't qualify for savings on a Marketplace plan. A job-based health plan is considered "affordable" if your share of the monthly premium in the lowest-cost plan offered by the employer is less than 9.02% of your household income. If your employer's plan meets this standard and is considered "affordable," you won't qualify for a premium tax credit if you buy a Marketplace insurance plan instead.

Envita Medical Center: Insurance Coverage and Your Treatment Options

You may want to see also

Explore related products

![]()

Medicaid eligibility and employment status

Medicaid eligibility is based on several factors, including income, age, residency, citizenship, ability, pregnancy, family size, and role within the household. It is also dependent on where you live, as different states have different rules and plans. For example, in Arizona, Medicaid is known as AHCCCS, and it covers individuals who earn a maximum of $1,507 to $4,625 monthly, depending on their family size. In Maryland, employer coverage is considered affordable if the annual cost to the employee is no greater than 9.02% of their annual household income.

Medicaid is not tied to employment status, so you can still have it even if you lose your job. If you find a new job, your eligibility will be re-evaluated based on your new financial situation. If your employer offers health insurance, you are not required to accept it, and you can choose to purchase a private health plan through the Marketplace instead. However, if your employer's insurance is considered affordable and provides minimum value, you are typically not eligible for a government subsidy to purchase your own insurance.

If you are enrolled in a job-based health plan, you will not qualify for savings or premium tax credits if you purchase a Marketplace insurance plan. However, if you are enrolled in COBRA insurance after losing your job, you can still apply for and enroll in Medicaid, and you can drop your COBRA coverage if you qualify for Medicaid.

It is important to note that Medicaid is always the last resort payer if you have coverage through another agency. This means that it covers smaller amounts, such as coinsurance or co-pay, while primary insurance covers more significant costs.

Chase Sapphire: Travel with Peace of Mind

You may want to see also

Frequently asked questions

Medicaid eligibility is based on where you live, your income, age, residency, citizenship, ability, pregnancy, family size, and the role you play in your household. If your employer's insurance is considered affordable and provides minimum value, you are not eligible for a government subsidy to buy your own insurance.

If your employer's insurance is not considered affordable, you may be eligible for a subsidy in the Marketplace, depending on your household income.

You can check to see if you're eligible for Medicaid. You may meet the financial requirements necessary to receive benefits.