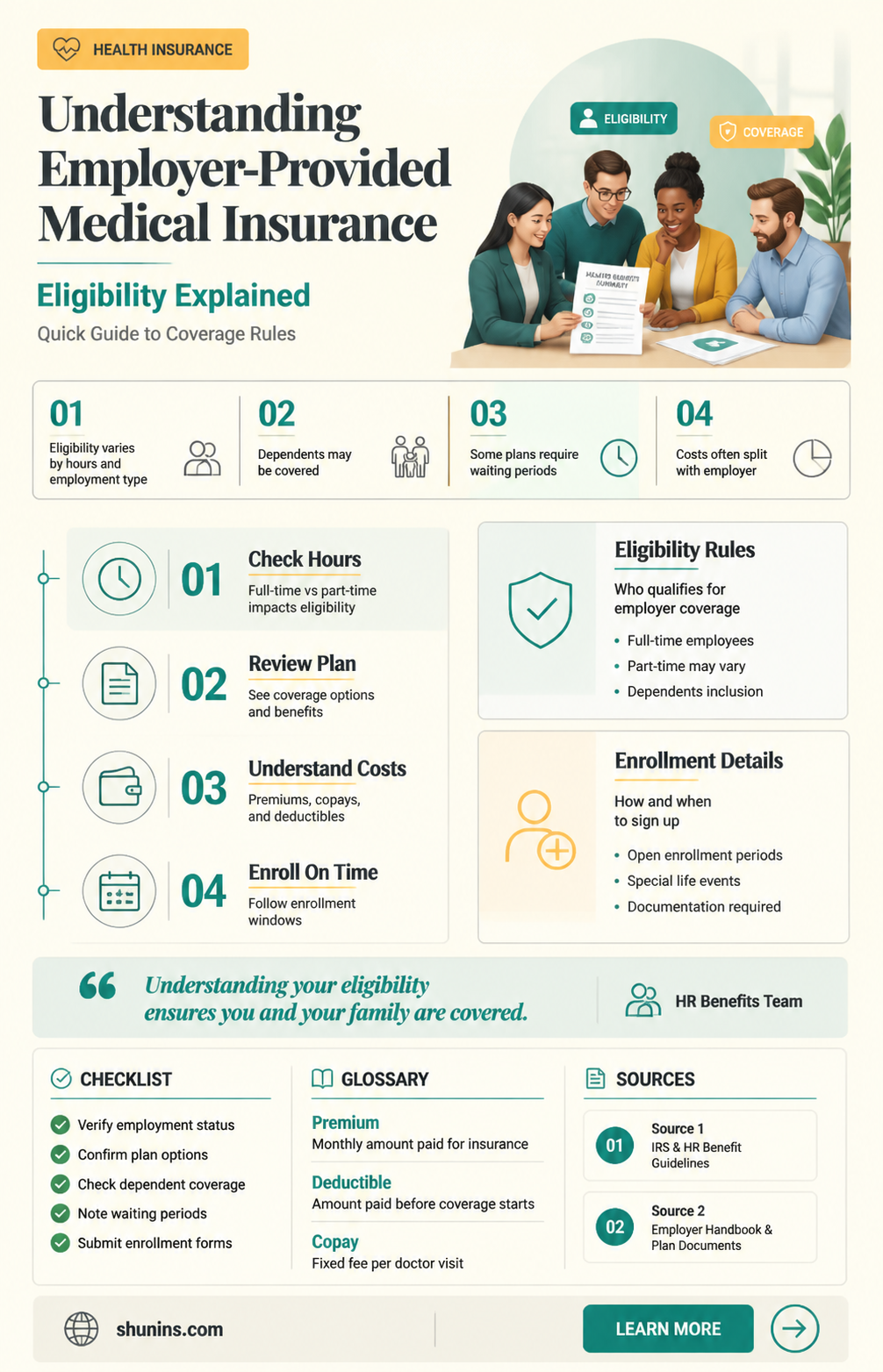

If you're wondering whether you're eligible for medical insurance from your employer, there are a few things to consider. Firstly, it's important to understand that employers are not mandated to provide medical insurance to their employees. However, applicable large employers, generally those with 50 or more full-time employees, are required to offer coverage to at least 95% of their full-time employees and dependents. Small employers with fewer than 50 full-time employees may be eligible for tax credits and other benefits to help cover the cost of providing insurance. If your employer offers medical insurance, they will typically cover most of the monthly premium, while you will pay the remaining cost. The affordability of the plan is determined by whether the premium you pay is less than a certain percentage of your household income, which varies slightly depending on the state and year.

| Characteristics | Values |

|---|---|

| Affordability | A health plan is considered affordable if the premium is not more than 8.39% of the employee's household income for 2024. For 2025, a job-based health plan is considered "affordable" if the employee's share of the monthly premium in the lowest-cost plan is less than 9.02% of their household income. |

| Minimum Value Standard | A health plan meets the minimum value standard if it covers at least 60% of the total medical costs and provides sufficient coverage for hospital and doctor services. |

| Eligibility for Financial Help | If an employer-sponsored health plan meets the minimum value standard and is considered affordable, the employee will not qualify for financial help to lower the cost of a health plan. |

| Employer Mandate | Applicable large employers, generally those with 50 or more full-time employees, are required to offer coverage to at least 95% of full-time employees and dependents. Employers that do not comply may be subject to penalties. |

| Small Business Health Care Tax Credit | Small employers with fewer than 25 full-time employees may be eligible for a tax credit to help cover the cost of providing health coverage. |

Explore related products

What You'll Learn

![]()

What is considered affordable medical insurance?

When it comes to affordable medical insurance, there are a few key factors to consider. Firstly, it's important to assess your current and future healthcare needs. For instance, are you planning to start a family, do you require prescription medications, or are there any upcoming medical procedures you need to factor in? These considerations will help you decide if a high-deductible health plan (HDHP) is suitable for you. HDHPs typically have lower premiums but higher out-of-pocket expenses when you require healthcare services.

The affordability of health insurance is relative to an individual's income. According to Healthcare.gov, as of 2025, a job-based health plan is deemed "affordable" if the employee's share of the monthly premium for the lowest-cost plan offered by their employer is less than 9.02% of their household income. This plan must also meet the minimum value standard. If the plan is considered affordable for the employee but not for other household members, only those members may qualify for savings. Additionally, if the premiums are not affordable for the employee and the household, they may be eligible for savings through a Marketplace plan.

When comparing insurance providers, it's worth looking into companies like Kaiser Permanente, which offers competitive average monthly costs and programs to help manage various health conditions. Aetna is another option, particularly beneficial for those seeking to save on prescription costs, as they offer the lowest copayments and coinsurance for medications. However, their premiums and deductibles are relatively high, so for those who don't require many prescriptions, they may not be the most cost-effective choice. Blue Cross Blue Shield (BCBS) offers a diverse range of plans, while Molina Healthcare has been recognized for its affordable overall costs, customer complaints, and plan options.

Ultimately, the definition of "affordable" medical insurance will vary depending on your income, healthcare needs, and the specific offerings of insurance providers. It's important to thoroughly research and compare different plans and providers to find the one that best suits your requirements and budget.

Secondary Medical Insurance: Understanding Your Backup Coverage

You may want to see also

Explore related products

![]()

How does employer-based insurance affect my taxes?

Employer-based insurance can affect your taxes in several ways. Firstly, if your employer pays for your health insurance plan, their payments are typically exempt from federal income and payroll taxes, including social security, Medicare, and FUTA taxes. This exclusion lowers the after-tax cost of health insurance for employees, making it a valuable benefit.

However, the impact of employer-sponsored health insurance on Social Security taxable wages is more complex. Rising health insurance contributions can influence the distribution of money wages and the percentage of wages below the "taxable maximum," which is the earnings level at which the payroll tax is capped. As a result, changes in the average cost and distribution of employer-sponsored health insurance (ESHI) costs can affect both wage distribution and the percentage of wages subject to payroll tax.

Additionally, if you have job-based insurance, you generally won't qualify for savings or financial assistance on a Marketplace plan. A job-based health plan is typically considered "affordable" if your share of the monthly premium is less than a certain percentage of your household income, and it meets minimum value standards. If your employer's plan is considered affordable and meets the minimum value standard, you won't be eligible for premium tax credits if you purchase a Marketplace insurance plan instead.

It's worth noting that family members of employees may have different considerations. In some cases, they may qualify for tax credits or financial assistance even if the employee doesn't. Affordability for family members is determined based on the cost of family coverage, and if the cost exceeds a certain percentage of household income, they may be eligible for financial help.

Accessing Weight Loss Medication sans Insurance: Options and Strategies

You may want to see also

Explore related products

![]()

Can I still buy private insurance if my employer offers insurance?

If your employer offers health insurance, you are not obligated to accept it. You can still purchase private insurance, but you should carefully weigh the pros and cons of each option. Employer-sponsored plans are often the most cost-effective option for regular medical needs or families due to lower costs from employer contributions. They also provide comprehensive coverage and access to a broad network of providers. However, they may not cover all specific health needs and offer limited flexibility with network and plan options.

On the other hand, private insurance plans offer the most flexibility in choosing plan options and providers. You can tailor them to specific health needs not covered by other plans. However, these plans usually come with higher costs and do not qualify for subsidies, making them potentially more expensive. Additionally, the coverage may be less comprehensive than employer or Marketplace options.

If you decide to purchase a Marketplace plan instead of accepting your employer's insurance, you should be aware that your employer will not help pay your premiums. You may also not qualify for savings or premium tax credits if your employer's insurance is considered affordable and meets minimum standards. Affordability is determined by whether your share of the monthly premium in the lowest-cost plan offered by your employer is less than a certain percentage of your household income. The specific percentage varies by state and year, but it is generally around 8-9%.

It is important to consider your personal health needs, the coverage offered by each plan, and the associated costs when deciding between employer-sponsored insurance and private insurance. You should also be aware of any state-specific tax penalties or exemptions for not having health insurance.

Staying Covered: Understanding Parental Insurance Limits

You may want to see also

Explore related products

![]()

What if I missed my employer's open-enrollment period?

If you missed your employer's open enrollment period, you could lose coverage for yourself and your loved ones, and you could be subject to a fine imposed by the Affordable Care Act (ACA). You may also be unable to make changes or enroll in benefits until the next open enrollment period.

However, there are some options to consider if you missed your employer's open enrollment period. Firstly, contact your HR manager to discuss your options and find out if there are any exceptions that may apply. Some circumstances may allow employees to retroactively register for benefits outside the standard enrollment window. Secondly, certain life events, such as getting married or divorced, having or adopting children, or losing eligibility for other health coverage, can trigger a special enrollment period (SEP) and grant you mid-year enrollment and plan changes. Thirdly, you can explore short-term health insurance plans, which are typically cheaper than traditional health plans but may not provide sufficient coverage. These plans can be purchased year-round and can serve as a temporary solution until the next open enrollment period. Finally, you can purchase a private health plan through independent insurance agencies or state-based marketplaces like Covered California or Maryland Health Connection. However, you may have to pay full price unless your employer-sponsored coverage is considered unaffordable or does not meet minimum value standards.

To avoid missing the open enrollment period, it is essential to be proactive and mark deadlines on your calendar. Employers also have a responsibility to notify employees about benefits-related deadlines, so staying informed about your company's healthcare plans and policies is crucial.

Get Medical Insurance in Texas: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

What if my employer doesn't offer insurance?

If your employer does not offer insurance, you will need to create your own benefits package, similar to someone who is self-employed or working for a small business without health coverage. You can select from any available plan in your area, and your employer may still contribute towards the cost through a QSEHRA or ICHRA. A QSEHRA, or Qualified Small Employer Health Reimbursement Arrangement, is a system where your employer reimburses you a certain amount of money each month to cover some or all of the costs of a self-purchased health insurance plan. With a QSEHRA, you may also be eligible for premium tax credits, although the tax credit amount will be reduced by the amount your employer contributes.

ICHRA, or Individual Coverage Health Reimbursement Arrangement, is similar to QSEHRA in that your employer will reimburse you for some or all of the costs of your self-purchased insurance plan. However, if you accept an ICHRA, you will not be eligible for a premium tax credit.

If you are enrolled in a Marketplace plan and then gain access to job-based insurance, you will no longer qualify for savings on your Marketplace plan. Your job-based insurance is considered "affordable" if your share of the monthly premium in the lowest-cost plan offered by the employer is less than 9.02% of your household income.

When deciding on an insurance plan, consider your lifestyle and medical history. If you are young, healthy, and do not engage in risky activities, you may want to opt for a lower-cost plan with a higher deductible. However, if you have a family history of medical problems or engage in risky activities, you may want to pay a higher premium for a lower deductible.

Get Medical Insurance Quickly: A Step-by-Step Guide

You may want to see also

Frequently asked questions

A job-based health plan meets the minimum value standard if it covers at least 60% of medical costs and offers substantial coverage of hospital and doctor services.

A job-based health plan is considered "affordable" if your share of the monthly premium in the lowest-cost plan offered by the employer is less than 9.02% of your household income.

You may want to cancel your Marketplace plan and enroll in the job-based insurance. You won't qualify for savings if you're enrolled in a job-based plan.

You can change to a Marketplace plan, but you won't qualify for savings if your job-based plan is considered "affordable" and meets the minimum value standard.