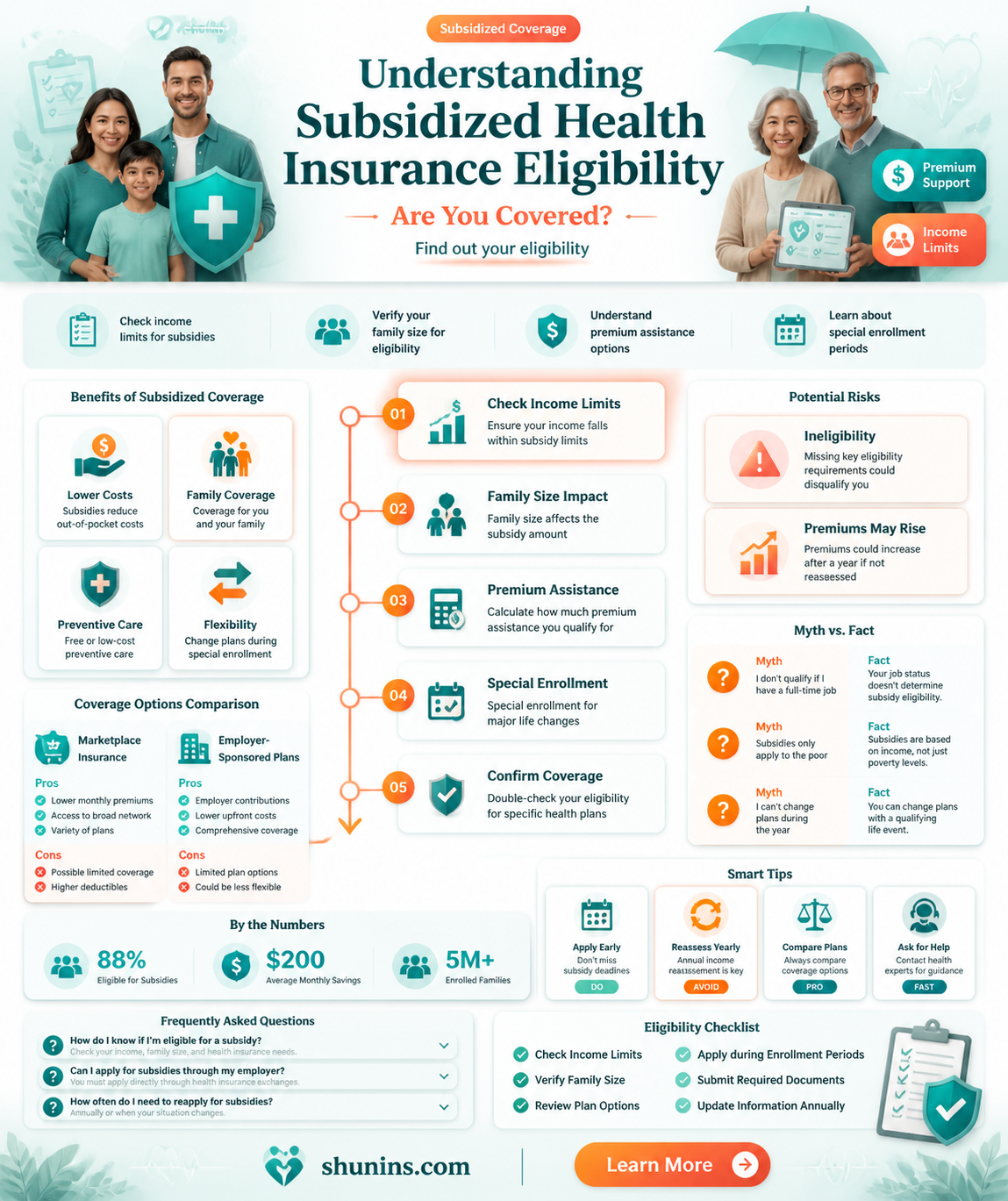

Navigating the complexities of health insurance can be daunting, especially when trying to determine eligibility for subsidized plans. Subsidized health insurance, often available through government programs like the Affordable Care Act (ACA) in the United States, is designed to make coverage more affordable for individuals and families with lower incomes. Eligibility is typically based on factors such as household income, family size, and citizenship or immigration status. To qualify, your income must fall within a certain range of the Federal Poverty Level (FPL), and you generally cannot have access to affordable employer-sponsored insurance. Additionally, eligibility may vary by state, as some have expanded Medicaid programs under the ACA. Understanding these criteria is crucial, as it can significantly reduce your healthcare costs and ensure you have access to essential medical services.

Explore related products

What You'll Learn

![]()

Income Limits for Subsidized Health Insurance

To calculate your eligibility, start by determining your household’s Modified Adjusted Gross Income (MAGI), which includes wages, salaries, tips, and other taxable income. Certain deductions, such as contributions to retirement accounts, are not subtracted from this figure. Once you have your MAGI, compare it to the current FPL guidelines for your household size. Online calculators and tools provided by healthcare.gov can simplify this process, offering instant estimates of potential subsidies. Keep in mind that income limits vary by state, as some states have expanded Medicaid eligibility to cover individuals earning up to 138% of the FPL, further broadening access to affordable coverage.

A common misconception is that earning above 400% of the FPL automatically disqualifies you from any assistance. While it’s true that premium tax credits are capped at this level, other cost-saving measures may still apply. For instance, individuals with high medical expenses or those living in areas with elevated insurance costs might find plans with reduced out-of-pocket maximums or lower deductibles. Additionally, some states offer their own subsidy programs or reinsurance funds to lower premiums for all enrollees, regardless of income. Exploring these options can uncover hidden opportunities for savings.

For those nearing the income threshold, strategic financial planning can make a difference. If your income is slightly above 400% of the FPL, consider contributing more to tax-advantaged accounts like a Health Savings Account (HSA) or increasing retirement savings to reduce your MAGI. Alternatively, if you’re self-employed, business expenses can sometimes be optimized to lower taxable income. However, it’s crucial to balance these strategies with long-term financial goals, as over-deducting could impact your overall financial health. Consulting a tax professional or financial advisor can provide tailored guidance in these scenarios.

Finally, income limits are not set in stone and can fluctuate based on life changes such as job loss, marriage, divorce, or the birth of a child. If your income drops mid-year, you may qualify for increased subsidies or Medicaid, depending on your state’s rules. Conversely, if your income rises, you might need to adjust your premium tax credits to avoid repaying excess subsidies at tax time. Reporting income changes promptly to the marketplace ensures your coverage remains accurate and affordable. Staying informed and proactive about these limits empowers you to maximize your eligibility for subsidized health insurance, regardless of your financial situation.

Top Health Insurance Providers Offering Plans in Pennsylvania: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Family Size Impact on Eligibility

Family size plays a pivotal role in determining eligibility for subsidized health insurance, as it directly influences the calculation of your household income relative to the Federal Poverty Level (FPL). For instance, a family of four with an annual income of $100,000 may qualify for subsidies, while an individual earning the same amount might not. This is because the FPL threshold increases with each additional family member, allowing larger households to access subsidies at higher income levels. Understanding this dynamic is crucial for accurately assessing your eligibility and maximizing potential benefits.

To illustrate, consider the 2023 FPL guidelines: a family of one has a threshold of $14,580, while a family of four is set at $30,000. Subsidies are typically available for households earning up to 400% of the FPL. Using these figures, a family of four earning $120,000 (400% of $30,000) would still qualify for subsidies, whereas an individual earning $58,320 (400% of $14,580) would exceed the limit. This example highlights how family size can significantly expand eligibility, even at higher income brackets.

When applying for subsidized health insurance, it’s essential to include all household members in your calculations, even if they are not seeking coverage. Dependents, spouses, and children under 26 (if claimed as dependents) are typically counted. However, be cautious: failing to report all household members or inaccurately estimating income can lead to incorrect subsidy amounts and potential repayment obligations. Use the Healthcare.gov subsidy calculator or consult a certified navigator to ensure precision.

A persuasive argument for larger families is the disproportionate impact of healthcare costs. With more individuals to insure, out-of-pocket expenses can quickly escalate. Subsidies act as a financial buffer, making comprehensive coverage more affordable. For example, a family of six might face premiums exceeding $2,000 monthly without assistance, but subsidies could reduce this to a manageable $500–$800, depending on income. This underscores the importance of leveraging family size to secure financial relief.

Finally, consider the long-term implications of family size on eligibility. As your household grows or shrinks (e.g., through marriage, divorce, or children aging out), your subsidy eligibility may change. Regularly update your Marketplace application to reflect these shifts, as failing to do so could result in overpaying or losing subsidies altogether. Proactive management ensures continuous access to affordable coverage tailored to your family’s evolving needs.

Self-Insured Medical Plans: Do They Include Prescription Rebates?

You may want to see also

Explore related products

![]()

Citizenship and Immigration Status Requirements

In the United States, citizenship and immigration status are pivotal determinants of eligibility for subsidized health insurance programs, such as Medicaid and the Children’s Health Insurance Program (CHIP). U.S. citizens, regardless of age or income, may qualify for these programs based on state-specific guidelines. For instance, in states that have expanded Medicaid under the Affordable Care Act (ACA), individuals earning up to 138% of the federal poverty level (FPL) are eligible. However, non-citizens face stricter criteria, often requiring a five-year wait after obtaining qualified immigration status before accessing Medicaid or CHIP, though exceptions exist for emergency services and pregnant individuals.

For lawfully present immigrants, eligibility varies by visa category and state policies. Refugees, asylees, and certain parolees, for example, are immediately eligible for Medicaid and CHIP without a waiting period. Conversely, undocumented immigrants are generally excluded from federal programs, though some states, like California and New York, offer limited state-funded coverage for specific groups, such as children or pregnant women. Understanding these distinctions is critical, as misinterpreting eligibility rules can lead to unnecessary financial strain or missed opportunities for affordable healthcare.

The ACA’s marketplace subsidies, available through Healthcare.gov or state exchanges, are another pathway to subsidized insurance. Lawfully present immigrants, including those with green cards, DACA recipients, and certain visa holders, can access these subsidies if their income falls between 100% and 400% of the FPL. However, undocumented immigrants are explicitly excluded from marketplace plans and subsidies. To apply, individuals must provide documentation proving their immigration status, such as a passport, I-94 form, or Employment Authorization Document (EAD).

Navigating these requirements demands careful attention to detail. For instance, mixed-status families—where some members are citizens and others are not—may face complex scenarios. Citizen children in such families are eligible for Medicaid or CHIP, even if their parents are undocumented. Similarly, pregnant women with lawful status can access prenatal care regardless of their income level in many states. Practical tips include using online eligibility tools provided by Healthcare.gov or consulting local community health centers, which often offer assistance in multiple languages.

In conclusion, citizenship and immigration status significantly shape access to subsidized health insurance in the U.S. While citizens and certain lawfully present immigrants have clear pathways to coverage, undocumented individuals face substantial barriers. Staying informed about state-specific policies and leveraging available resources can help individuals maximize their eligibility and secure affordable healthcare. For those in doubt, seeking guidance from certified application counselors or immigration attorneys can provide clarity and ensure compliance with evolving regulations.

Medicaid Insurance Options: Understanding the Different Plan Names

You may want to see also

Explore related products

![]()

State-Specific Eligibility Criteria Explained

Eligibility for subsidized health insurance varies dramatically by state, reflecting each state's unique economic landscape, political priorities, and Medicaid expansion decisions. For instance, in expansion states like California and New York, adults earning up to 138% of the Federal Poverty Level (FPL) qualify for Medicaid, while non-expansion states like Texas and Florida limit eligibility to parents earning as little as 17% FPL. This disparity means a family of three earning $28,000 annually could qualify in Illinois but not in Alabama, despite identical incomes. Understanding your state’s stance on Medicaid expansion is the first step in determining your eligibility for subsidized coverage.

Beyond Medicaid expansion, states impose additional criteria that can either broaden or restrict access. For example, some states require asset tests for certain populations, such as pregnant women or children, while others waive them entirely. In Minnesota, individuals aged 65+ must meet specific asset limits to qualify for Medical Assistance, whereas Colorado focuses solely on income. Age-based rules also differ: in Washington, young adults up to 26 can remain on their parents’ Medicaid if the parents qualify, but in Georgia, this provision is not enforced. These nuances highlight the importance of consulting state-specific guidelines rather than relying on federal rules alone.

Income thresholds for subsidized Marketplace plans also vary by state, influenced by whether they’ve expanded Medicaid. In Kentucky, a single adult earning $18,000 qualifies for subsidies because the state expanded Medicaid, but in Mississippi, the same individual would likely fall into the “coverage gap”—earning too much for Medicaid but too little for Marketplace subsidies. To navigate this, use the Healthcare.gov subsidy calculator, which accounts for state-specific benchmarks. For example, in 2023, the subsidy cutoff for a single adult in a non-expansion state is roughly $13,590, while in expansion states, it’s $18,754.

Practical tips can streamline the eligibility process. First, gather documentation proving income, citizenship, and residency—pay stubs, tax returns, and utility bills are commonly required. Second, leverage state-run marketplaces like Covered California or New York State of Health, which often provide clearer guidance than federal platforms. Third, if your income fluctuates, report changes immediately; failure to do so could result in overpayments or loss of coverage. Finally, consider working with a certified navigator or broker who specializes in your state’s programs—their expertise can uncover eligibility you might otherwise miss.

The takeaway is clear: eligibility for subsidized health insurance is not one-size-fits-all. Each state’s criteria are shaped by its policies, demographics, and resources, creating a patchwork of opportunities and barriers. By understanding your state’s specific rules—from Medicaid expansion status to income thresholds and asset tests—you can maximize your chances of securing affordable coverage. Whether you’re a young professional in Oregon or a retiree in Florida, the key to unlocking subsidies lies in deciphering the fine print of your state’s system.

Insurance Support: Navigating Your Accident Journey

You may want to see also

Explore related products

![]()

How to Apply for Subsidized Plans

Applying for subsidized health insurance begins with understanding the marketplace, specifically Healthcare.gov in the U.S., which serves as the gateway to Affordable Care Act (ACA) plans. These plans are income-based, with subsidies available to individuals earning between 100% and 400% of the federal poverty level (FPL). For 2023, this translates to an annual income range of $13,590 to $54,360 for a single person, adjusted proportionally for larger households. If your income falls within this bracket, you’re likely eligible for premium tax credits, which reduce your monthly premiums, or cost-sharing reductions, which lower out-of-pocket costs like deductibles and copays.

Once eligibility is confirmed, the application process involves creating an account on Healthcare.gov or your state’s exchange, if applicable. You’ll need to provide personal information, including income details, Social Security numbers, and immigration status documentation. Accuracy is critical; discrepancies can delay approval or result in incorrect subsidy amounts. For example, if you estimate your income too high, you might pay more in premiums than necessary, while underestimating could lead to repaying excess subsidies at tax time. Pro tip: Gather recent pay stubs, tax returns, and W-2 forms beforehand to streamline the process.

After submitting your application, the marketplace will verify your information and determine your subsidy eligibility. If approved, you’ll receive a summary of available plans, each with a clear breakdown of costs after subsidies. Here’s where comparison becomes key: Bronze plans often have lower premiums but higher out-of-pocket costs, while Gold plans offer lower deductibles at a higher monthly cost. Consider your healthcare needs—frequent doctor visits or prescription medications may justify a higher-tier plan. Additionally, open enrollment typically runs from November 1 to January 15, but qualifying life events (e.g., job loss, marriage) allow for special enrollment periods.

A common pitfall is overlooking cost-sharing reductions (CSRs), which are only available if you enroll in a Silver plan and earn less than 250% of the FPL. CSRs can significantly reduce out-of-pocket expenses, making Silver plans more cost-effective than Gold plans for some individuals. For instance, a Silver plan with CSRs might offer a $500 deductible instead of $3,000, depending on your income level. This detail underscores the importance of selecting the right plan based on both premiums and potential out-of-pocket costs.

Finally, stay informed about policy changes and extensions, such as the American Rescue Plan Act of 2021, which increased subsidies and expanded eligibility through 2025. These updates can affect your application strategy, making it worthwhile to consult a navigator or broker for personalized guidance. Applying for subsidized health insurance requires attention to detail, but the potential savings make it a worthwhile endeavor. With the right approach, you can secure comprehensive coverage tailored to your financial situation.

Penalties for Ignoring Medical Insurance Fraud

You may want to see also

Frequently asked questions

Subsidized health insurance is financial assistance provided by the government to help lower the cost of health insurance premiums and out-of-pocket expenses. It is typically for individuals and families with low to moderate incomes who meet specific eligibility criteria.

Eligibility is primarily based on your household income and size, compared to the Federal Poverty Level (FPL). Generally, if your income falls between 100% and 400% of the FPL, you may qualify for subsidies through the Health Insurance Marketplace.

Yes, immigration status matters. To qualify for subsidized health insurance, you must be a U.S. citizen, a lawfully present immigrant, or meet specific immigration criteria. Undocumented immigrants are not eligible for subsidies.

If your employer offers affordable health insurance that meets minimum value standards, you may not qualify for subsidies through the Marketplace. However, if the employer’s plan is unaffordable or doesn’t meet the criteria, you may still be eligible for subsidies.