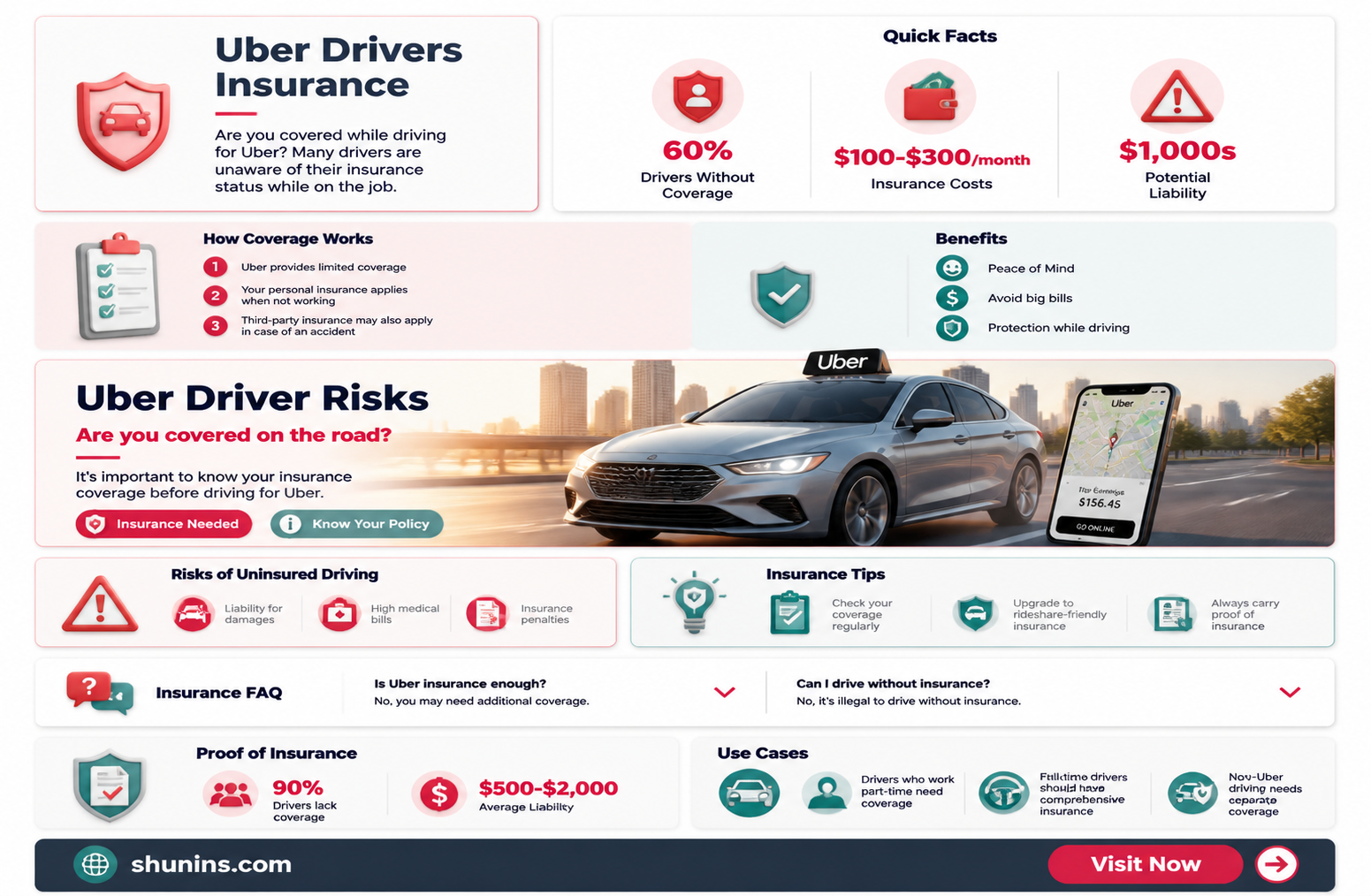

If you're an Uber driver, it's important to understand the insurance coverage you have and any potential gaps. Uber does provide insurance for its drivers, but it may not cover all scenarios, and requirements vary by location. For example, in the UK, Uber does not provide insurance, so drivers must take out their own Uber-approved policy. In the US, Uber maintains commercial auto insurance on behalf of drivers and delivery people who use the Driver app, but this may not cover all situations. To fill in these gaps, Uber drivers can purchase additional coverage, such as rideshare coverage or a rideshare endorsement, which extends their personal policy while they're working but haven't accepted a ride request. Understanding your insurance coverage as an Uber driver is crucial to ensure you're adequately protected in the event of an accident or incident.

| Characteristics | Values |

|---|---|

| Insurance for Uber drivers | Covered by Uber when driving without passengers in the US; no insurance provided by Uber in the UK |

| Insurance for Uber riders | Covered by Uber in the event of an accident |

| Insurance for third parties | Covered by Uber in the event of an accident |

| Personal insurance | Required for Uber drivers; may need to be extended with a rideshare endorsement to cover gaps in Uber's insurance |

| Commercial insurance | Required for commercially licensed Uber drivers |

| Rental car insurance | Included in rental offers through Uber's Vehicle Marketplace; additional insurance may be purchased |

| Reporting accidents | Through the Driver app or by calling the Safety Incident Reporting Line |

Explore related products

What You'll Learn

![]()

Uber's insurance coverage for drivers

Uber maintains insurance on behalf of its drivers to cover their liability for property damage and injuries to riders and third parties involved in an accident. This includes at least $1,000,000 for property damage and injuries to riders and third parties involved in an accident. In addition, Uber's third-party liability insurance covers the cost of injuries or damage in the amounts of $50,000 per person and $100,000 per accident for injuries. Depending on the state's laws, Uber may provide additional coverage for the driver and riders, including coverage for injuries in a hit-and-run or an accident caused by an uninsured or underinsured driver, as well as personal injury protection for medical expenses and lost wages.

It is important to note that Uber's insurance coverage for drivers has some gaps. Uber's insurance does not cover regular maintenance on the driver's car, and drivers are responsible for their vehicle maintenance. Additionally, Uber's insurance may not cover all situations, and drivers may need to rely on their personal insurance or purchase additional coverage. For example, if a driver is en route to or on a trip, their personal insurance, including comprehensive and collision coverage, will be the primary source of coverage for repairing their car.

To comply with legal requirements and ensure adequate protection, Uber drivers should consider purchasing a "rideshare endorsement" or "rideshare coverage" policy feature. This type of policy extends the driver's personal insurance coverage while they are working but have not yet accepted a ride request. Once a ride request is accepted, the coverage provided by Uber takes over. A rideshare endorsement can also provide benefits like roadside assistance and reimbursement for deductible differences.

In some countries, such as the UK, Uber does not provide any insurance coverage for drivers. In these cases, drivers must take out their own Uber-approved insurance policy, specifically private hire taxi insurance, to comply with local regulations. This type of insurance covers both the vehicles and any passengers in the event of an accident.

Auto Insurance: The Future of Protection and Coverage

You may want to see also

Explore related products

![]()

Personal insurance requirements for Uber drivers

As an Uber driver, you are an independent contractor, and Uber maintains insurance on your behalf to cover your liability for property damage and injuries to riders and third parties involved in an accident. However, this insurance does not cover regular maintenance on your car, and you are responsible for maintaining your vehicle.

While Uber provides insurance, it is essential to understand that your regular car insurance does not cover you when driving for Uber. Therefore, you need to purchase additional insurance, commonly known as "rideshare coverage" or a "rideshare endorsement," to extend your personal policy while working. This type of insurance bridges the gap when you are logged in and waiting for a ride request, ensuring your car is covered both on and off the clock.

In the United States, Uber drivers are typically covered by Uber's insurance when driving without passengers. However, once you accept a ride request, the coverage provided by Uber takes over. It is important to note that Uber's insurance does not cover maintenance on your vehicle, and you are responsible for keeping your car in good condition.

In the United Kingdom, Uber does not provide any insurance, and drivers must take out their own Uber-approved insurance policy. This insurance is typically called private hire taxi insurance and covers both the vehicle and any passengers in the event of an accident.

Additionally, some states, like Florida, have specific insurance requirements for Uber drivers. For example, in Florida, all drivers must have a minimum of $10,000 in property damage liability and personal injury protection coverage to comply with the state's no-fault insurance laws.

Auto Insurance Company Screening: What's the Deal?

You may want to see also

Explore related products

![]()

Additional insurance coverage for Uber drivers

Uber maintains commercial auto insurance on behalf of its drivers and delivery people who use the Driver app. This insurance covers motorists under specific circumstances. Uber's insurance operates in tandem with your personal auto insurance. However, driving for Uber falls under a commercial auto insurance policy, and you may need to purchase additional insurance coverage.

Uber drivers should consider purchasing an additional policy feature called "rideshare coverage" or a "rideshare endorsement." This type of policy extends your personal insurance while you're working but haven't accepted a ride request yet. Once you accept a ride request, the coverage provided by Uber takes over.

Rideshare insurance through Uber fills the gap between your personal insurance and Uber's insurance. It covers you while you're driving with the app active but haven't received a pick-up request. Although Uber provides liability coverage during this period, it doesn't protect your vehicle. Therefore, rideshare coverage is essential to extend your regular vehicle coverage while you await a ride request.

Many personal auto insurers offer additional insurance for rideshare drivers, but this isn't required to sign up for Uber. However, it's crucial to inform your insurance company that you drive for a ride-sharing service. Without rideshare coverage, you risk not only paying out of pocket for a claim but also being dropped by your insurance company.

In addition, depending on your state, you may have the option to purchase Optional Injury Protection insurance. This provides extra coverage for your medical expenses, disability, and survivor benefits while you're online, en route, or on a trip.

Credit Card Auto Insurance: Understanding Your Coverage for Zipcar Rentals

You may want to see also

Explore related products

![]()

How to report an accident as an Uber driver

As an Uber driver, you are covered by Uber's insurance policy when you are online and available for a trip. This third-party liability insurance covers the cost of injuries or damage to riders and third parties involved in the accident. The coverage amounts to at least $50,000 per person and $100,000 per accident for injuries. Additionally, Uber provides at least $1,000,000 for property damage.

In 42 states, Uber offers Optional Injury Protection for $0.024 per mile ($0.022 per mile in Washington). This insurance provides benefits for medical expenses, disability, loss of life, and dismemberment while you are online or on a trip.

Now, here is a step-by-step guide on how to report an accident as an Uber driver:

- Take photos of the accident scene: Capture images of any damage to the vehicles involved, including your own. Ensure you also take pictures of the accident location if it is safe to do so.

- Exchange information: Obtain the contact and insurance details of the other drivers and riders involved in the accident.

- Report the accident to Uber: Use the Driver app on your phone to report the crash. Go to the Safety Toolkit by tapping the blue shield symbol in the bottom left corner of the map, then select "Report a crash." Describe what happened and submit your claim. Alternatively, you can speak with Uber's support staff by choosing "Safety" from the Help section of the app and then selecting the "Safety Incident Reporting Line."

- Complete the process promptly: It is important to report the accident as soon as it is reasonable to do so. After submitting your claim, a notification will appear on your Driver app homepage directing you to the Crash Center.

- Work with the claims support team: Uber's claims support team will guide you through the claims process and crash reporting to the insurance coverage provider in your state. They will also reach out to confirm everyone's well-being and gather any additional information needed.

- Understand your insurance coverage: Depending on your state and the specific circumstances of the accident, you may be covered by Uber's insurance or your personal insurance policy. If you are a commercially licensed and insured driver, you should also contact your commercial automobile insurance provider.

Get Auto Insurance for Your New Vehicle: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Insurance for Uber drivers in the UK

Uber drivers in the UK are responsible for arranging their own insurance. As an Uber driver, you are classed as an independent contractor, so it's your job to ensure you have the right level of commercial private hire taxi insurance, including third-party liability and cover for personal use.

Types of Insurance

There are two main types of insurance you need as an Uber driver in the UK: commercial private hire insurance (also known as Hire and Reward insurance) and public liability insurance.

Commercial Private Hire Insurance

Commercial private hire insurance allows you to carry pre-booked passengers from one place to another in exchange for money. This is different from standard private car insurance, which does not cover the risks associated with carrying passengers for hire and reward.

Public Liability Insurance

Public liability insurance covers the cost of any claims made against you by members of the public. This could include compensation for personal injuries or damage to property that you might have caused while driving for work. For example, if a passenger trips while getting out of your car and makes an injury claim against you, public liability insurance will cover any fees or legal expenses.

Uber-Approved Insurance

In December 2021, Uber released a list of 'Uber-approved' insurers for their London-based drivers. This list contained just eight insurance companies. It is worth checking if your insurer is Uber-approved, as this will make the process smoother.

Cost of Insurance

The cost of insurance for Uber drivers in the UK varies depending on the level of cover, your driving history, and the type of vehicle you own. On average, private hire drivers with a good driving record can expect to pay around £180 for a 30-day policy or £1,600 for an annual policy. Annual insurance tends to be cheaper, with drivers saving around £500 over a 12-month period compared to a rolling monthly policy.

Auto Insurance: How Much Coverage Do You Need?

You may want to see also

Frequently asked questions

You need commercial auto insurance or private hire insurance.

Uber maintains insurance on behalf of its drivers to cover liability for property damage and injuries to riders and third parties involved in an accident. However, this does not cover regular maintenance on your car. Uber also offers optional injury protection in 42 states.

All rental offers available through Uber's Vehicle Marketplace include insurance. Some partners also offer the option to purchase additional insurance.

If you are commercially licensed to operate commercial vehicles, you are required to have your own commercial auto insurance.

Take photos of any damage to the vehicles involved and get the contact and insurance information of other drivers and riders. You can report the crash through the Driver app.