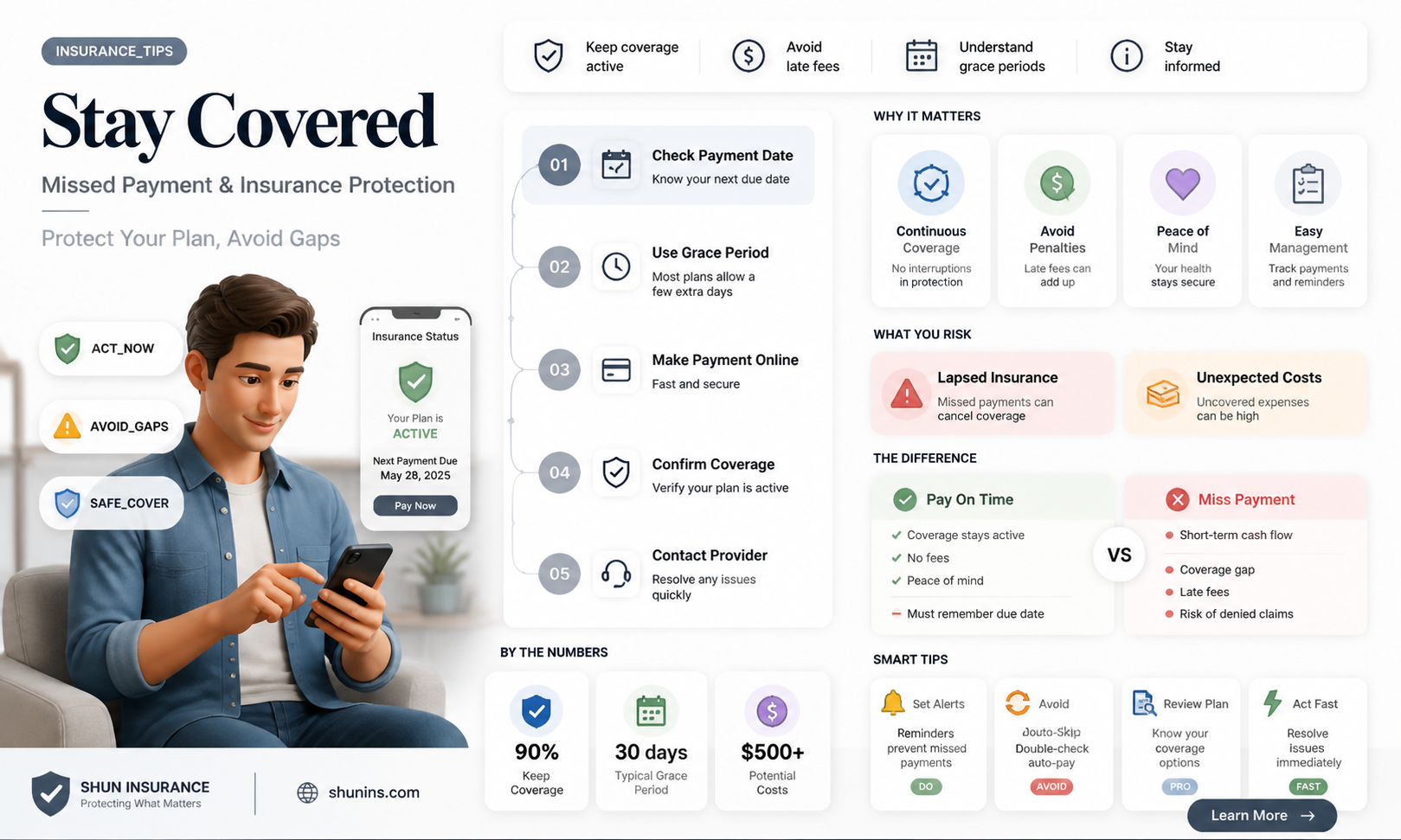

Missing an insurance payment can have serious consequences. Most insurance companies offer grace periods of seven to thirty days, during which your coverage remains active. However, if you miss payments after the grace period, your policy may be cancelled, and you could face a coverage lapse, leading to increased premiums. In addition, unpaid instalments can negatively impact your credit score and remain on your record for up to ten years. It is always best to be proactive and contact your insurer as soon as possible if you think you might miss a payment.

| Characteristics | Values |

|---|---|

| Grace period | Varies by insurer, usually 7 to 30 days |

| Policy after grace period | Cancellation or coverage lapse with increased premiums |

| Credit score impact | Negative impact |

| Future insurance | Less likely to get coverage from a new provider |

| Driving without insurance | Illegal in Canada and Ontario |

| Outstanding balance | Default registered with the Credit Reference Agency for 6 years |

| Mortgage contract | Policy cancellation may void the contract |

| High-risk category | Higher monthly costs |

Explore related products

What You'll Learn

![]()

Grace periods

During the grace period, your insurance coverage remains active, and you can pay your bill without incurring any additional fees or penalties. However, it's important to act quickly and make the payment as soon as possible, as the longer you wait, the more likely it is that your policy will be cancelled.

If you miss a payment, your insurer will typically send you a notification and inform you of the grace period you have to make the payment. They will also inform you of the consequences of failing to make the payment before the grace period ends. These consequences can include policy cancellation, a coverage lapse, or an increase in your premiums.

In some cases, missing a payment can also result in a surcharge or daily fee until the payment is made in full. It can also negatively impact your credit score and make it more difficult to obtain insurance coverage in the future. Therefore, it's important to be proactive and contact your insurer as soon as you realise you've missed a payment or may miss an upcoming payment.

Additionally, it's worth noting that if you have an outstanding car loan, your lender may require you to have comprehensive and collision insurance. Missing payments and having your insurance cancelled can result in your lender repossessing your vehicle.

Emirates ID: Check Your Daman Insurance Status

You may want to see also

Explore related products

$14.97 $30

![]()

Policy cancellation

In the event of policy cancellation, individuals may face higher insurance rates and limited payment options when seeking new coverage. Insurers may view those with a history of non-payment as high-risk policyholders, leading to increased premiums. Additionally, missed payments can remain on an individual's record for up to 10 years, making it challenging to obtain coverage from new providers.

Before cancelling a policy, insurance companies typically follow a specific process. They will send notifications of missed payments and provide a grace period, which can range from 7 to 30 days or even up to 3 months in some cases, such as with health insurance. During this time, policyholders can make the payment without penalties. However, if the payment remains unpaid, the insurer will send additional notices before eventually cancelling the policy.

To avoid policy cancellation, it is essential to be proactive. Contacting the insurer as soon as a missed payment is anticipated can be helpful. Additionally, individuals can consider scheduling automatic withdrawals, using text or email payment reminders, and shopping around for lower insurance rates if necessary. Maintaining timely insurance payments is crucial to avoid the consequences of policy cancellation, which can extend beyond increased rates and include legal and financial repercussions.

Wells Fargo: Mortgage, Insurance, and You

You may want to see also

Explore related products

![]()

Credit score impact

Most insurance policies do not impact your credit score if you miss a payment. However, if you pay your car insurance monthly, missing a payment can affect your credit score. This is because, when you buy car insurance, you usually have to do it for a whole year, but if you want to pay month by month, your insurance provider gives you a loan for the yearly amount, and you enter a credit agreement with them. This can mean that a hard check is run on your credit file, which stays on your file for up to 2 years and can hurt your credit score.

If you miss a payment, your insurer may offer a grace period, but if you don't pay during this time, your coverage will end. Driving during a car insurance lapse may result in legal and financial consequences. If you miss a payment, it's important to pay it back before your account goes into default, which is 14 days after the default notice is sent. If your policy is cancelled, not only do you lose insurance, but the default is also recorded in your credit report, which can cost you up to 350 points out of a maximum of 1000, according to Experian. A default will stay on your credit report for six years, and can only be removed if it was an error.

If you continue to let your bill go unpaid, your insurer may send it to a collection agency, at which point your credit score will be affected. A collection entry on your credit report will remain for seven years from the date of the missed payment, and will lower your credit score for as long as it appears, although its impact will lessen over time.

Missing an insurance payment can also impact your insurance rates in the future. Many insurers will not insure clients with missed payments, and your current insurer may increase your premium when it's time to renew your policy or decide not to renew it at all.

Reviewing Your National Insurance Record: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Driving without insurance

Missing an insurance payment can put you at risk of losing your insurance coverage. While insurance companies typically offer grace periods of 7 to 30 days, during which your coverage remains active, failure to make the payment within this period can lead to policy cancellation. It is important to review your insurance policy or contact your insurance company to understand their specific late payment policy and grace period terms.

If your policy is cancelled due to non-payment, you will be categorized as a high-risk driver. This can result in higher insurance rates and limited payment options when seeking new coverage. Additionally, missed payments can remain on your record for up to 10 years, making it challenging to find insurers willing to offer you coverage.

The consequences of driving without insurance go beyond legal and financial penalties. Without valid insurance, you are not protected in the event of an accident or incident. If you damage another vehicle, person, or property while uninsured, you may face significant financial burdens and even jail time. Therefore, it is crucial to stay up to date with your insurance payments and maintain continuous coverage to avoid the risks associated with driving without insurance.

Check Vehicle Insurance Status in Telangana: A Quick Guide

You may want to see also

Explore related products

![]()

Switching insurance providers

Missing an insurance payment can have serious consequences, and it's important to act quickly to remedy the situation. While some companies offer grace periods of up to 30 days, others do not, and a missed payment may result in immediate policy cancellation. Even if there is a grace period, failure to pay within this time can lead to coverage lapses and increased premiums.

If you are facing financial difficulties and think you may miss an insurance payment, it is best to be proactive and contact your insurance company as soon as possible. They may be able to offer a payment plan or other solutions to help you maintain your coverage. Additionally, you can make changes to your policy online, such as setting up automatic payments or changing the payment account to one that you use more frequently.

If you are unable to come to an agreement with your current insurance provider, you may need to consider switching to a new provider. When shopping for a new insurance policy, it is important to compare quotes from multiple reputable companies to find the best rates and coverage for your needs. Keep in mind that missed payments can stay on your record for up to 10 years, and some insurers may be hesitant to offer coverage to clients with a history of missed payments. However, with careful planning and proactive communication, you can work to mitigate the risks associated with missed insurance payments and ensure that you maintain the coverage you need.

In addition to switching insurance providers, there are a few other options to consider if you are struggling to make payments. One option is to review your policy and see if there are any adjustments you can make to lower your current rates. You can also consider using an insurance broker, who can help you shop around for lower rates. Finally, if you are facing financial hardship, you may qualify for a Special Enrollment Period for health insurance, which can provide additional options for coverage.

Credit Checks: Progressive's Rental Insurance Requirements

You may want to see also

Frequently asked questions

If you miss an insurance payment, your policy may be cancelled, and you may be charged a surcharge or daily fee until your payment is made in full. Your rates may also increase. It is best to get in touch with your insurer as soon as possible.

Missing an insurance payment will not immediately affect your credit score, as insurance companies do not report payments to credit bureaus. However, if the debt remains unpaid, your account may be transferred to a debt collection agency, which will negatively impact your credit score and remain on your record for up to 10 years.

Yes, insurance companies typically offer grace periods of 7 to 30 days, during which your coverage remains active. However, it is important to check your insurance company's policy, as some insurers do not have grace periods and may cancel your policy immediately after a missed payment.