Whether insurance payments are made pre- or post-tax depends on a variety of factors, including the type of insurance, the nature of employment, and the specific insurance plan. In the context of health insurance, the distinction between pre-tax and after-tax premiums is crucial as it influences employees' tax obligations and eligibility for other benefits. Pre-tax health insurance premiums, which are deducted from gross pay, effectively lower taxable income and result in higher take-home pay. Conversely, after-tax premiums are paid from disposable income, and employees may be able to deduct these expenses when filing income taxes. Employers typically offer pre-tax health insurance plans, such as Section 125 cafeteria plans, which provide employees with a choice between benefits like cash and health coverage. However, not all health insurance plans are pre-tax, and it is essential to consult with insurance providers to understand the specifics of each plan.

| Characteristics | Values |

|---|---|

| Are all insurance payments pre-tax? | No, not all insurance payments are pre-tax. |

| Who decides if insurance payments are pre-tax? | The employer decides if insurance payments are pre-tax. |

| What are the benefits of pre-tax insurance payments? | Pre-tax insurance payments reduce the total amount of taxable income, increasing take-home pay. |

| What are the different types of pre-tax insurance plans? | Section 125 cafeteria plans, Health Reimbursement Arrangements (HRAs), Individual Coverage Health Reimbursement Arrangements (ICHRAs), Excepted Benefit Health Reimbursement Arrangements (EBHRAs), and Flexible Spending Accounts (FSAs). |

| Can employees choose their insurance plan? | Yes, employees can choose their insurance plan and may opt for pre-tax or post-tax payments depending on the plan. |

| Are there any tax implications for employees who choose pre-tax insurance? | Yes, pre-tax insurance may affect an employee's Social Security payments at retirement. |

Explore related products

$20.17 $20.17

What You'll Learn

![]()

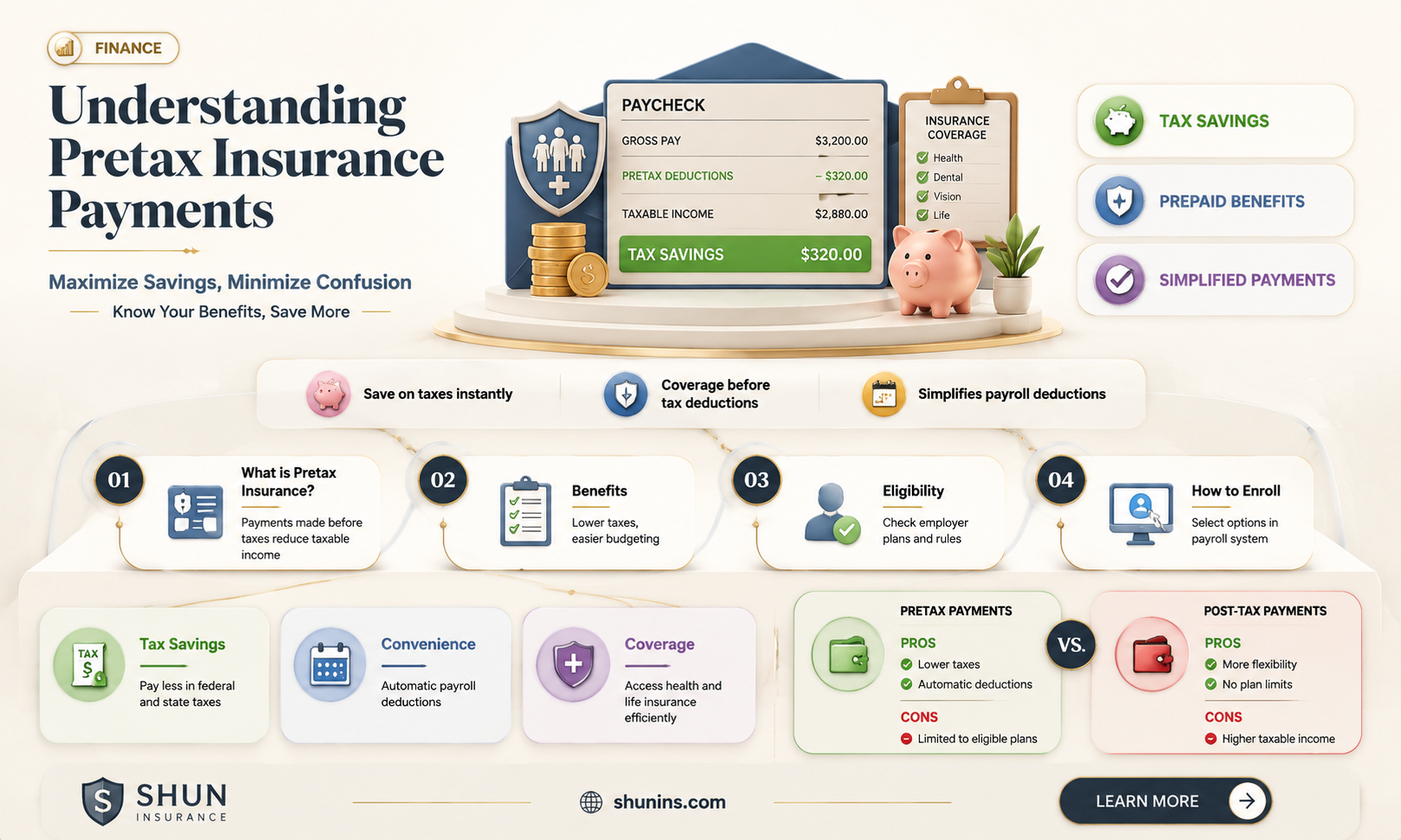

Pre-tax insurance payments reduce taxable income

Pre-tax insurance payments reduce an individual's taxable income. This means that the amount deducted to pay for medical insurance premiums will not be subject to certain taxes, such as Social Security taxes. As a result, there will be a decrease in the total amount of taxable income, leading to lower income tax deductions and increased take-home pay.

There are various ways to benefit from pre-tax insurance payments. Firstly, employer-sponsored health reimbursement arrangements (HRAs) allow employees to have pre-tax benefits while paying for their premiums with post-tax dollars. Employers can reimburse employees for medical costs, including insurance premiums, using non-taxable funds. Secondly, employees can choose to have more money deducted from their paychecks to cover the cost of benefits, including insurance premiums, on a pre-tax basis. These voluntary payroll deductions require the employee's written consent and can result in tax savings.

Additionally, certain types of health insurance plans, such as Section 125 cafeteria plans, offer pre-tax benefits. Under these plans, employees can choose between different benefits, including cash and qualified benefits, which are not included in gross income. This allows employees to pay for their health insurance premiums with pre-tax dollars, reducing their taxable income.

It is important to note that not all health insurance plans are pre-tax, and there may be exceptions, such as health insurance for owners of S-Corporations. Therefore, it is essential to carefully review the terms of the insurance plan and consult with a tax professional or insurance broker to understand the specific tax implications.

By taking advantage of pre-tax insurance payments, individuals can effectively reduce their taxable income, resulting in potential tax savings and increased disposable income. However, it is always recommended to seek professional tax advice to ensure compliance with applicable laws and regulations.

Insurance Checks: Are They Part of Speeding Fines?

You may want to see also

Explore related products

$20.94 $20.94

![]()

Post-tax insurance payments are deductible

There are several types of health reimbursement arrangements (HRAs) that allow employees to have pre-tax benefits while paying for their premiums with post-tax dollars. A Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) is available for small employers who are not required to purchase company health insurance under the Affordable Care Act (ACA). A small employer under the ACA is defined as one with fewer than 50 full-time equivalent (FTE) employees. Another type of HRA is the Individual Coverage Health Reimbursement Arrangement (ICHRA), which allows employers to reimburse employees without contribution limits. All applicable large employers (ALEs) as defined by the ACA must ensure the plan is affordable. ALEs are employers with 50 or more FTEs. The third type of HRA is the Excepted Benefit Health Reimbursement Arrangement (EBHRA). The employer contribution to an EBHRA for 2025 is $2,150.

Additionally, most self-employed taxpayers (including business owners) can deduct health insurance premiums using Schedule 1 for Line 162 on Form 1040. If you paid your premiums with pre-tax dollars, you don't qualify for this credit since you already received a tax break when your employer deducted your premium from your paycheck. You can also list premiums as an itemized deduction when you file your income taxes for all medical expenses and premiums that exceed 7.5% of your income.

Finally, if you don't want to participate in your employer's pre-tax plan or if your employer doesn't offer a pre-tax plan, you may be able to deduct your medical premiums on an after-tax basis.

FDIC Insurance: Current Status and Future Outlook

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

Employers can offer different health insurance plans

One option for employers is to set up a premium-only plan (POP) or a Section 125 cafeteria plan, where insurance premium contributions are deducted from employees' payroll on a pre-tax basis. Alternatively, employers can offer a standalone Health Reimbursement Arrangement (HRA), such as a Qualified Small Employer HRA (QSEHRA) or Individual Coverage HRA (ICHRA). With an HRA, employers reimburse employees for their monthly premiums and other eligible medical expenses, providing tax benefits similar to a traditional pre-tax plan. Another option is a group coverage HRA (GCHRA), which assists employees with out-of-pocket costs like deductibles and copays.

Employers can also consider offering a health stipend, a taxable benefit that provides flexibility in reimbursing employees for their healthcare expenses. Additionally, most self-employed taxpayers can deduct health insurance premiums using Schedule 1 for Line 162 on Form 1040. It is important to note that employees can still deduct premiums as an itemized deduction when filing income taxes if they meet certain criteria.

Checking Your Driving Record: Lower Insurance Premiums

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![]()

Employees can open an FSA regardless of their health insurance plan

Employees can open a Flexible Spending Account (FSA) regardless of their health insurance plan. An FSA is a benefit that allows employees to use pre-tax dollars to pay for out-of-pocket health insurance or dependent care expenses. There are two types of FSAs: Healthcare and Dependent Care FSA. With an FSA, an employee enrols during the open enrolment period and chooses how much they would like to set aside pre-tax for the year. This amount is then deducted evenly from each paycheck for the remainder of the year. Employees can then use these funds for different IRS-approved health care expenses. It is important to note that health insurance premiums are not considered eligible expenses.

Healthcare FSAs are associated with the employer's plan and not the individual employee. This means that employees can elect the full IRS limit amount with each new employer, regardless of their previous contributions to an FSA at a different company. For example, if an employee enrols in a Healthcare FSA on January 1st and elects to defer $500 for the year, they can spend the entire $500 on the first day the plan is effective. FSA deferrals will then continue to be spread out for the rest of the year.

Dependent Care FSAs, on the other hand, function slightly differently. With a Dependent Care FSA, employees can only use the funds as they contribute them. For instance, if an employee elects to defer $2,400 across 24 pay periods, they will only have $100 available to use after the first pay period. It is worth noting that employees cannot usually decrease or increase their FSA contribution amount after its effective date, unless certain exceptions apply.

Employers have the flexibility to offer an FSA as part of their benefits package, regardless of whether the employee is enrolled in the company's health insurance plan. This can be a lucrative benefit, helping to attract and retain talented employees without significantly increasing the employer's costs. Additionally, employers can choose to contribute to employees' FSAs, but it is not mandatory. By offering an FSA, employers can assist employees in managing their healthcare costs and improving their financial wellness.

Shipt Insurance: What You Need to Know

You may want to see also

Explore related products

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![]()

Self-employed people are responsible for their own insurance

When it comes to insurance, self-employed individuals face a unique set of challenges and considerations. Unlike traditional employees, who often have access to group insurance plans and employer-sponsored benefits, those who are self-employed must navigate the insurance landscape on their own. This includes understanding the tax implications of insurance payments and ensuring that they have adequate coverage to protect their business and personal finances.

One of the key things that self-employed people need to understand is that they are typically responsible for their own insurance payments. This includes health insurance, liability insurance, and any other type of coverage that they may need to protect themselves and their business. The cost of these insurance premiums is generally tax-deductible, which can help offset the expense. This is an important consideration, as self-employed individuals often have to manage their own finances and ensure that they are compliant with all relevant tax laws.

In terms of pre-tax payments, the situation can vary depending on the type of insurance and the specific circumstances of the self-employed individual. Health insurance premiums, for example, are generally considered a personal expense and are not tax-deductible as a business expense. However, as mentioned earlier, self-employed individuals may be able to deduct these premiums when calculating their taxable income, thus reducing their overall tax liability. This can be done whether the individual is enrolled in a private health insurance plan or through the Health Insurance Marketplace.

On the other hand, certain types of insurance payments made by self-employed individuals may be classified as business expenses and could be tax-deductible before calculating taxable income. For example, if a self-employed person takes out insurance to protect their business equipment or inventory, the premiums may be deductible as a business expense. Similarly, liability insurance, which protects the business in the event of lawsuits or claims, may also qualify for a tax deduction. It's important to keep accurate records of all insurance payments and to consult with a tax professional to ensure that deductions are claimed correctly and in compliance with the latest tax laws and regulations.

Overall, while the specifics can vary depending on factors such as the type of insurance and the tax laws in the individual's country or region, self-employed people generally need to be proactive and diligent when it comes to managing their insurance needs and understanding the tax implications. By staying informed and seeking professional advice when needed, they can ensure that they have the necessary coverage in place while also taking advantage of any applicable tax benefits. This helps to protect their business, their finances, and their peace of mind.

Root Insurance: Credit Checks and You

You may want to see also

Frequently asked questions

No, not all insurance payments are pre-tax. It depends on the type of insurance plan and whether it is employer-sponsored. Generally, employer-based health insurance is pre-tax and deducted from wages before taxes. However, there are exceptions, such as health insurance for owners of S-Corporations.

You can check your pay stub for a column titled "Deductions" or something similar. If your health premium is listed there and deducted from your gross pay, it is a pre-tax premium.

Pre-tax insurance premiums reduce your taxable income, resulting in lower Social Security and income taxes. This leads to an increase in your take-home pay. Additionally, with pre-tax premiums, you receive the full tax benefit as all your premiums are tax-free.

Yes, you may be able to deduct your insurance premiums as an itemized deduction when you file your income taxes. However, this only applies if they exceed a certain percentage of your income, and you must not be enrolled in an employer-sponsored pre-tax health plan.

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)

![TurboTax Deluxe 2024 Tax Software, Federal Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71QcK4dsRbL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/512dhP2BIfL._AC_UL320_.jpg)