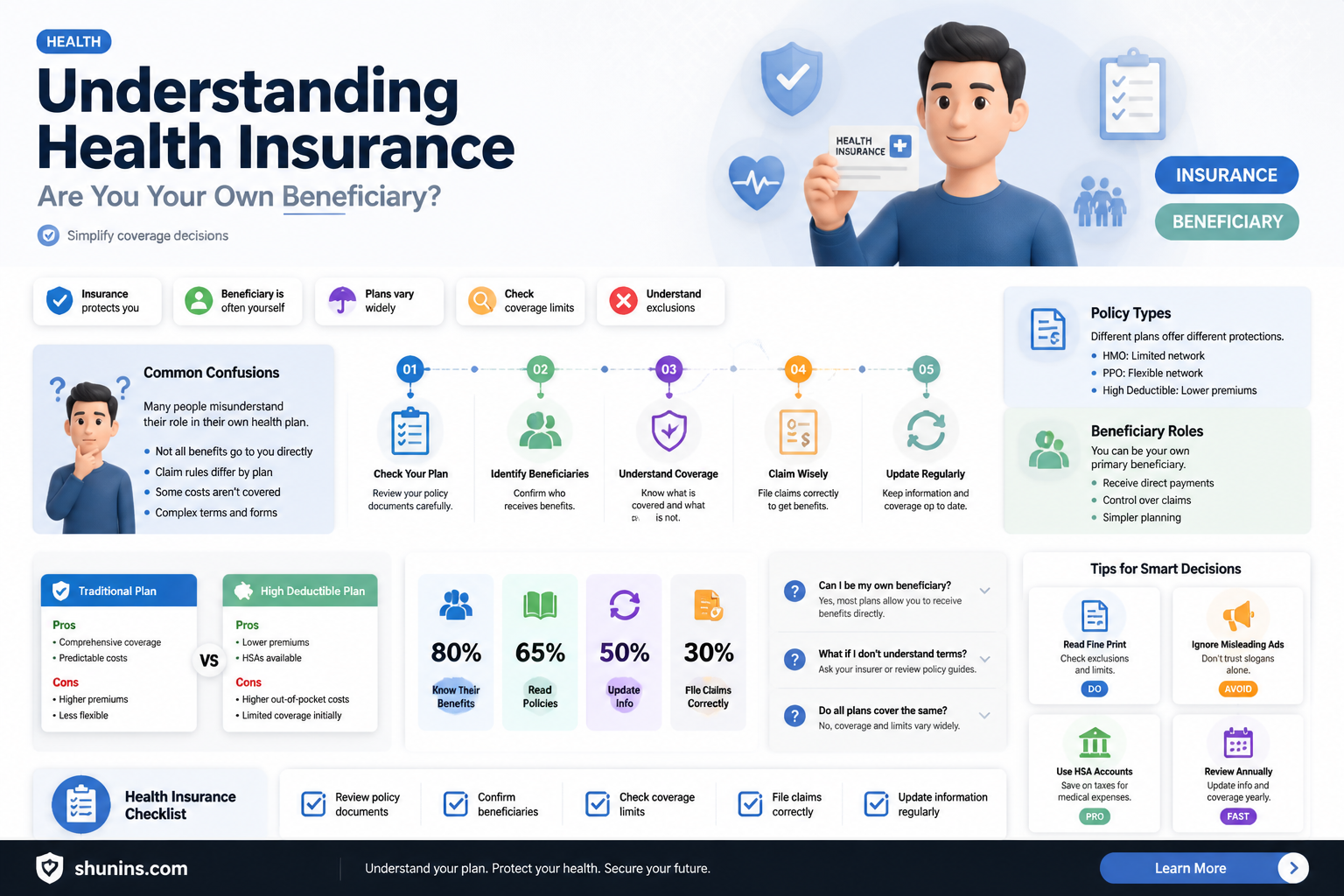

When considering health insurance, it’s essential to understand the concept of a beneficiary and whether you can be your own beneficiary. In most health insurance plans, the policyholder—typically the individual who purchases the coverage—is also the primary beneficiary, meaning they directly receive the benefits of the policy, such as medical care, treatments, and financial assistance for healthcare expenses. Unlike life insurance, where a beneficiary is designated to receive a payout upon the insured’s death, health insurance is designed to benefit the insured person directly. Therefore, in the context of health insurance, you are indeed your own beneficiary, as the coverage is intended to protect and support your own health and well-being. However, it’s always important to review your specific policy details to fully understand the terms and conditions.

| Characteristics | Values |

|---|---|

| Definition | In health insurance, the policyholder is typically the primary beneficiary, meaning you are your own beneficiary unless you designate someone else. |

| Default Beneficiary | Yourself (as the insured individual) |

| Applicability | Applies to most individual health insurance plans, including employer-sponsored plans where the employee is the policyholder. |

| Exceptions | Group plans where the employer is the policyholder, or if you explicitly designate a different beneficiary (e.g., family member). |

| Benefits Received | Direct access to health insurance benefits, including coverage for medical expenses, treatments, and preventive care. |

| Claim Process | You file claims and receive benefits directly, unless incapacitated, in which case a designated representative may act on your behalf. |

| Portability | Benefits are tied to you as the policyholder, allowing you to maintain coverage even if you change jobs or move (in some cases). |

| Tax Implications | Premiums paid by you (or your employer) may be tax-deductible or pre-tax, depending on the plan and jurisdiction. |

| Legal Rights | As the beneficiary, you have the right to appeal denied claims, choose providers (within network limits), and access plan details. |

| Dependents | You can add dependents (spouse, children) as beneficiaries, but they are not the primary beneficiary unless specified. |

| End-of-Life Considerations | If you pass away, any unused benefits typically do not transfer, unless a secondary beneficiary is designated. |

| Policy Control | You have full control over the policy, including the ability to change coverage, add/remove dependents, or cancel the plan. |

Explore related products

What You'll Learn

- Understanding Beneficiary Designation: Who receives health insurance benefits if you're incapacitated or deceased

- Self as Primary Beneficiary: Can you name yourself as the primary beneficiary for health insurance

- Dependent Coverage Rules: Are family members automatically beneficiaries under your health insurance policy

- Policy Payout Conditions: When and how does health insurance pay out to beneficiaries

- Updating Beneficiary Details: How to change or verify beneficiary information on your health insurance plan

![]()

Understanding Beneficiary Designation: Who receives health insurance benefits if you're incapacitated or deceased?

Health insurance policies often include provisions for beneficiary designation, a critical yet overlooked aspect of coverage. This designation determines who receives benefits if you're incapacitated or deceased, ensuring financial protection for your loved ones during challenging times. Typically, beneficiaries are individuals or entities you name to receive insurance proceeds, such as spouses, children, or trusts. However, the concept of being your own beneficiary is generally inapplicable in health insurance, as benefits are designed to cover your medical expenses while you're alive.

In the context of health insurance, the primary focus is on providing coverage for your healthcare needs, not distributing assets upon your death. When you're incapacitated, benefits are paid directly to healthcare providers or used to reimburse you for covered expenses. Upon your death, any outstanding claims or reimbursements may be paid to your estate, but this is not the same as a beneficiary designation. It's essential to distinguish between health insurance and other policies, like life insurance, where beneficiary designation plays a central role in asset distribution.

To ensure your wishes are carried out, review your health insurance policy and related documents, such as advance directives or living wills. These documents can specify how your healthcare decisions should be made if you're unable to do so. For instance, a durable power of attorney for healthcare allows you to appoint someone to make medical decisions on your behalf. While not directly related to beneficiary designation, these tools work in tandem with your insurance coverage to provide comprehensive protection.

Consider the following scenario: a 45-year-old policyholder with a family history of heart disease wants to ensure their spouse and children are financially secure if they become incapacitated or pass away. Although they cannot name themselves as beneficiaries for health insurance, they can take proactive steps. First, they should verify their policy covers pre-existing conditions and critical illnesses. Next, they can purchase supplemental policies, like critical illness or disability insurance, which often allow beneficiary designation. By layering coverage, they create a safety net that addresses both healthcare needs and financial security for their loved ones.

In summary, while you cannot be your own beneficiary for health insurance, understanding beneficiary designation and related concepts is crucial for comprehensive planning. Focus on maximizing your policy's benefits during your lifetime, and consider additional coverage options to protect your family's financial well-being. Regularly review and update your documents, ensuring they align with your current circumstances and wishes. By taking these steps, you can achieve peace of mind, knowing you've prepared for the unexpected.

What Health Insurance Doesn't Cover: Surprising Exclusions Explained

You may want to see also

Explore related products

![]()

Self as Primary Beneficiary: Can you name yourself as the primary beneficiary for health insurance?

Health insurance policies typically designate a beneficiary to receive benefits in the event of the insured's death or, in some cases, to manage claims on their behalf. However, the concept of naming oneself as the primary beneficiary for health insurance is often misunderstood. In most health insurance plans, the insured individual is inherently the primary beneficiary, as the policy is designed to cover their medical expenses directly. The term "beneficiary" in health insurance differs from its use in life insurance, where it refers to who receives the payout upon the insured's death.

To clarify, when you purchase health insurance, you are the direct recipient of the benefits, whether it’s coverage for doctor visits, hospitalization, or prescription medications. The policyholder (you) is automatically the primary beneficiary because the purpose of health insurance is to protect your own health and finances. There’s no need to formally designate yourself as a beneficiary, as the policy structure assumes you are the one benefiting from the coverage. This is a fundamental difference from other types of insurance, such as life or disability insurance, where beneficiaries are explicitly named to receive payouts.

One exception to this rule arises in specific scenarios, such as with Health Savings Accounts (HSAs) or certain employer-sponsored plans. For instance, an HSA allows you to designate a beneficiary who would inherit the account balance upon your death. In this case, you could name yourself as the primary beneficiary during your lifetime, but this is more about account ownership than health insurance coverage. Similarly, in family health plans, the policyholder (often the primary earner) may be considered the "primary beneficiary" in terms of managing the policy, but all covered family members still receive direct benefits.

Practical tip: Review your health insurance policy to understand its structure and how benefits are distributed. If you have an HSA or a similar account tied to your health plan, ensure your beneficiary designations align with your estate planning goals. For example, if you’re over 65 or have dependents, consider naming a spouse or child as the beneficiary for your HSA to ensure seamless transition of funds after your death.

In conclusion, while you cannot formally name yourself as the primary beneficiary for health insurance in the traditional sense, you are inherently the primary recipient of its benefits. The confusion often stems from conflating health insurance with other types of insurance where beneficiaries are explicitly designated. Understanding this distinction simplifies policy management and ensures you maximize the benefits of your coverage. Always consult your policy documents or an insurance professional for clarity on specific terms and conditions.

Employee Rights: Suing for Poor Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Dependent Coverage Rules: Are family members automatically beneficiaries under your health insurance policy?

Health insurance policies often include provisions for dependent coverage, but the rules governing who qualifies as a beneficiary can vary widely. A common misconception is that family members are automatically covered under your policy. In reality, most plans require explicit enrollment of dependents, whether they are spouses, children, or other eligible relatives. This process typically involves providing documentation, such as birth certificates or marriage licenses, to verify the relationship. Failure to enroll dependents formally can result in denied claims, leaving you financially responsible for their medical expenses.

The Affordable Care Act (ACA) mandates that health insurance plans allow children to remain on their parents’ policy until age 26, regardless of marital status, financial dependency, or student status. However, this rule applies only to children and does not extend to other family members like parents or siblings. For spouses, coverage is usually available but not automatic. You must actively add them to your policy during open enrollment or a qualifying life event, such as marriage. Some plans may also cover domestic partners, but this varies by insurer and state regulations.

Employer-sponsored plans often have specific guidelines for dependent coverage, including age limits for children and definitions of eligible family members. For instance, stepchildren or adopted children are typically covered, but grandchildren or nieces/nephews may not be unless they meet certain legal dependency criteria. It’s crucial to review your plan’s Summary Plan Description (SPD) to understand these rules. Additionally, some plans require dependents to reside with the policyholder, while others may allow coverage for those living elsewhere, such as college students.

From a practical standpoint, ensuring your family members are properly enrolled as beneficiaries involves proactive steps. First, review your policy’s dependent coverage rules annually, especially if your family situation changes. Second, keep accurate records of enrollment forms and verification documents. Third, take advantage of open enrollment periods or qualifying life events to update your coverage. Ignoring these steps can lead to gaps in coverage, leaving your family vulnerable to unexpected medical costs. By staying informed and taking action, you can maximize the benefits of your health insurance policy for yourself and your loved ones.

Will I Lose My Health Insurance? Understanding Coverage Risks and Options

You may want to see also

Explore related products

![]()

Policy Payout Conditions: When and how does health insurance pay out to beneficiaries?

Health insurance policies are designed to provide financial protection against medical expenses, but the conditions under which payouts occur can vary widely. Understanding these conditions is crucial to ensuring you receive the benefits you’re entitled to. Payouts typically occur when covered medical services are rendered, but the specifics depend on factors like the type of plan, network restrictions, and whether the service is deemed medically necessary. For instance, a PPO (Preferred Provider Organization) may pay out-of-network claims at a lower rate, while an HMO (Health Maintenance Organization) might require in-network care for any payout. Always review your policy’s Explanation of Benefits (EOB) to understand how and when payments are made.

One critical aspect of policy payout conditions is the concept of the beneficiary. In most health insurance plans, the policyholder is also the primary beneficiary, meaning they directly receive the benefits in the form of covered medical services or reimbursements. However, in cases like life insurance riders or dependent coverage, a designated beneficiary (such as a spouse or child) may receive payouts. For example, if a policy includes accidental death coverage, the named beneficiary would receive a lump sum. Health insurance, though, rarely pays out directly to beneficiaries unless it’s a supplemental policy like critical illness insurance, which provides a cash benefit upon diagnosis of a covered condition.

The timing of payouts is another key consideration. Health insurance typically operates on a reimbursement model, where the insured pays upfront and is later reimbursed by the insurer. However, many plans now use direct payment systems, where the insurer pays the healthcare provider directly after applying deductibles, copays, or coinsurance. For instance, if a policy has a $1,000 deductible, the insured pays the first $1,000 of covered services out-of-pocket before the insurer begins payouts. Understanding these thresholds and payment structures can help you plan for out-of-pocket costs and avoid unexpected expenses.

Lastly, policy payout conditions often include exclusions and limitations that dictate when a claim will not be paid. Common exclusions include cosmetic procedures, experimental treatments, and pre-existing conditions (though the latter is less common under the Affordable Care Act). For example, a policy might exclude coverage for weight-loss surgery unless it’s deemed medically necessary. Additionally, some policies require pre-authorization for certain procedures, such as MRIs or surgeries, to qualify for payout. Failing to obtain pre-authorization could result in denied claims, leaving you responsible for the full cost. Always verify coverage details before proceeding with treatment to ensure compliance with payout conditions.

Optometrist Billing: Medical Insurance Coverage and Claims

You may want to see also

Explore related products

![]()

Updating Beneficiary Details: How to change or verify beneficiary information on your health insurance plan

You might assume you’re automatically your own beneficiary for health insurance, but this isn’t always the case. Health insurance policies typically designate beneficiaries for specific benefits, like life insurance payouts or certain end-of-life expenses. While you’re the primary policyholder, ensuring your beneficiary details are accurate is crucial for seamless claim processing and financial protection for your intended recipients.

Steps to Update or Verify Beneficiary Information:

- Locate Your Policy Documents: Start by reviewing your health insurance policy or summary of benefits. Look for sections titled "Beneficiary Designation" or "Policy Beneficiaries."

- Contact Your Insurer: Reach out to your insurance provider via phone, online portal, or email. Most insurers require a formal request to update beneficiary details, often accompanied by a signed form.

- Provide Required Documentation: Be prepared to submit identification (e.g., driver’s license) and proof of relationship for the new beneficiary, if applicable. For example, a birth certificate for a child or marriage certificate for a spouse.

- Confirm the Update: After submitting changes, request written confirmation from your insurer. Verify the details are correct to avoid future complications.

Cautions to Keep in Mind:

- Life Changes Trigger Updates: Marriage, divorce, birth of a child, or the death of a beneficiary are critical moments to review and update your information.

- Avoid Assumptions: Don’t assume your insurer will automatically update beneficiaries based on external records (e.g., marriage certificates). Proactive action is essential.

- Multiple Beneficiaries: Some policies allow you to designate primary and contingent beneficiaries. Clearly specify percentages or conditions for each recipient.

Practical Tips for Smooth Updates:

- Set Reminders: Schedule annual reviews of your beneficiary details, especially if your life circumstances change frequently.

- Keep Copies: Store physical and digital copies of your updated beneficiary forms and confirmation letters in a secure location.

- Inform Your Beneficiaries: Let your designated beneficiaries know they’ve been named and where to find relevant documentation if needed.

By staying proactive and informed, you ensure your health insurance benefits are directed to the right individuals, providing peace of mind for both you and your loved ones.

Trampoline-Friendly Insurance: Companies That Allow Trampoline Coverage

You may want to see also

Frequently asked questions

Yes, in most cases, you are the primary beneficiary of your health insurance, as the coverage is designed to provide medical benefits directly to you.

Health insurance typically does not allow naming a beneficiary like life insurance does, as the benefits are meant for your own medical care, not financial payout to others.

No, being your own beneficiary does not affect claims. You can still file claims for covered medical services as per your policy terms.

Health insurance does not provide a death benefit. Any outstanding medical bills would be handled separately, often through your estate or other insurance like life insurance.

Health insurance policies generally do not have a beneficiary designation option, as the benefits are inherently for your own use.