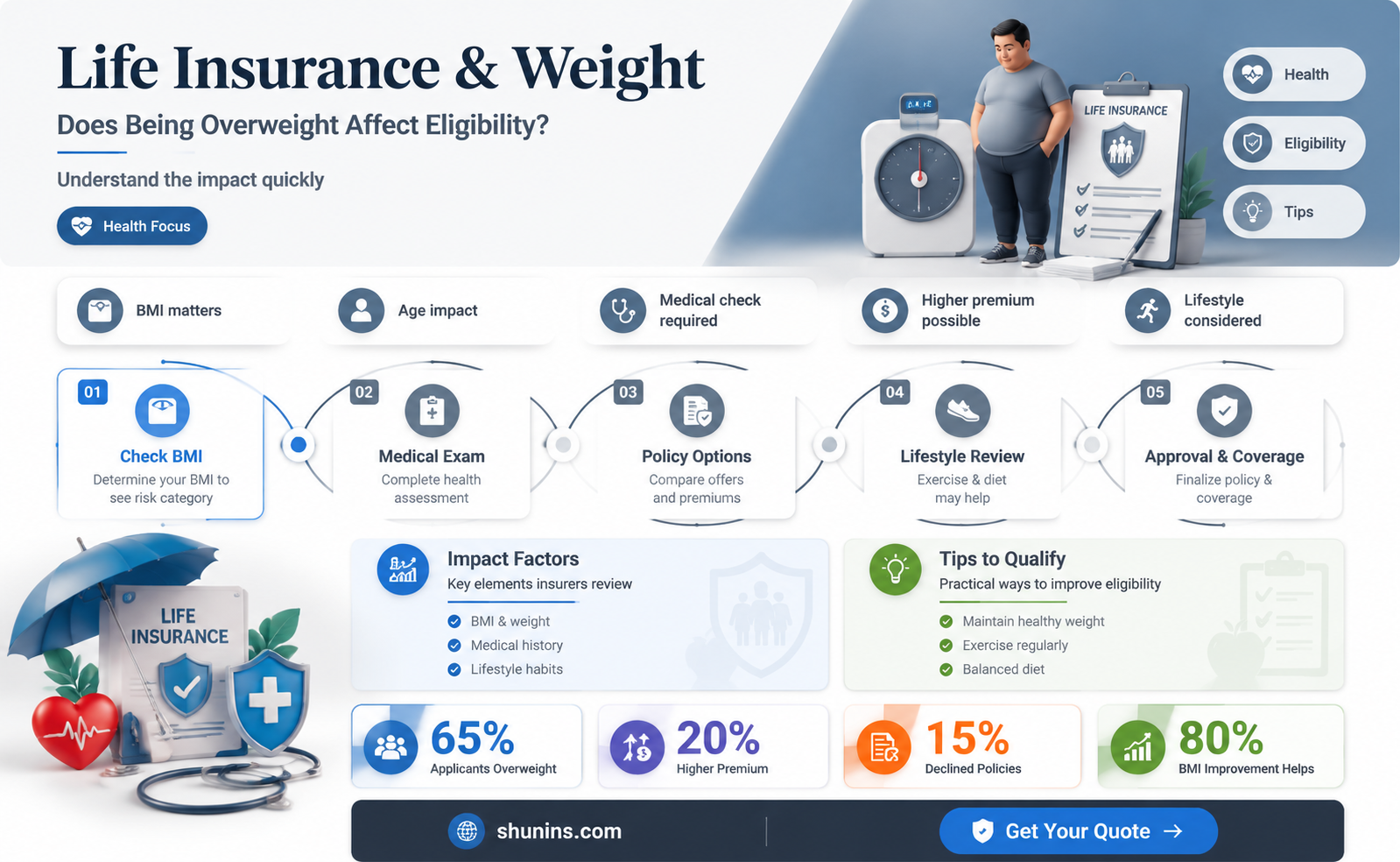

Being overweight doesn't automatically disqualify you from getting life insurance, but it might affect the rate and type of policy you qualify for. Life insurance companies evaluate an applicant and offer a rate based on their risk, but each company calculates risk differently. Some companies may consider overweight individuals to be more likely to suffer from diseases that can shorten life expectancy, such as diabetes, heart disease, and certain types of cancer. They may offer a higher rate, especially if a life insurance medical exam shows that you have other health issues.

| Characteristics | Values |

|---|---|

| Weight a factor? | Yes, but only one of many. |

| Height-to-weight ratio | Used to determine if you are overweight or obese. |

| Body Mass Index (BMI) | Used by insurers to determine eligibility and rate. |

| Weight loss | Can lower your premiums. |

| Weight gain | Can increase your premiums. |

| No-exam life insurance | An option for those with health issues, but more expensive. |

| High BMI | Likely to result in more expensive rates. |

| Low BMI | May also result in more expensive rates. |

| Morbid obesity | Could result in rejection for coverage. |

| Athletic build | May qualify for credits from an insurance company. |

| High BMI with no health issues | Unlikely to be rejected for coverage. |

| High BMI with health issues | Likely to be charged a higher rate. |

Explore related products

What You'll Learn

![]()

How does weight affect life insurance rates?

Life insurance companies use a variety of health and lifestyle factors to assess how risky you are to insure and determine the cost of your policy. One of these factors is your height-to-weight ratio, which is used to calculate your Body Mass Index (BMI). A high BMI can indicate a higher risk of developing serious health conditions like heart disease, type 2 diabetes and sleep apnea, and life insurance companies typically consider applicants with a high BMI to be high-risk.

However, BMI is not a perfect tool. It doesn't take body composition into account, so a muscular athlete may have a BMI that indicates they are overweight, even if they are healthy. This is why insurance companies also use their own "build charts" to determine how your BMI will affect your eligibility and rate. These build charts are similar to BMI charts, but they also take into account factors such as age and gender.

If your BMI falls into the obese range, long-term weight loss can lower your premiums. However, insurers will typically only give you credit for half the weight you've lost in the past 12 months, as they want to know that your weight loss is sustained. If you've lost weight through surgical methods, you may face higher premiums or even be denied coverage due to the risk of complications from the procedure.

If you are overweight but otherwise healthy, you will likely qualify for a policy with a relatively low rate. If you have weight-related or other health complications, you may pay more for coverage. Each insurance company calculates risk differently, so it's worth shopping around to find the lowest rates for your weight and overall health profile.

Life Insurance: Does It Expire or End?

You may want to see also

Explore related products

![]()

What is a pre-existing condition?

A pre-existing condition is a medical issue that has been diagnosed or treated before applying for life insurance. Each insurer has its own underwriting process to assess applicants' risk profiles, and some are more flexible about certain health conditions than others.

In general, you'll raise a red flag if you have one or more of the following pre-existing conditions:

- High blood pressure

- Heart disease

- Diabetes

- Cancer

- Asthma

- Previous injuries (depending on their severity and any lasting effects)

- Mental health conditions (depression, anxiety, etc.)

The impact a pre-existing condition has on your life insurance premium will mostly depend on its severity. The more severe a condition is, the more you can expect it to impact your premium.

Insurers typically group applicants into rate classes based on their health, such as standard, preferred, or super preferred. The goal is to categorize the risk of insuring you based on your life expectancy. Most people qualify for preferred or standard rates, but if you have a serious health condition, you may only qualify for substandard rates, or the insurer may deny coverage altogether.

Life Insurance and Compound Interest: How Are They Linked?

You may want to see also

Explore related products

![]()

What is no medical exam life insurance?

No medical exam life insurance is a type of life insurance policy that allows you to skip the medical exam that is usually required when applying for a life insurance policy. This type of insurance is meant as an alternative for individuals who may have trouble qualifying for a traditional insurance policy.

The most common no-exam life insurance policies include simplified issue, guaranteed issue, and employer-sponsored life insurance. Simplified issue life insurance is the most common type, where you complete a short health questionnaire and get covered immediately. Guaranteed issue life insurance offers limited coverage amounts for a predictable premium, and may not be enough to meet your family's needs, but can help cover final expenses. Employer-sponsored life insurance is offered as part of an employee benefits package and is highly affordable or free, and doesn't require a medical exam. However, these policies may only be active while you are still with the employer and typically offer limited coverage.

No-exam life insurance is often chosen by those with pre-existing medical conditions or those in high-risk occupations, such as firefighters, construction workers, or racecar drivers. It is also a good option for those with a fear of needles or anxiety about visiting the doctor.

The pros of no-exam life insurance include no medical tests, faster approval, and more accessibility. However, there are also cons to this type of insurance. It is typically more expensive than traditional insurance, and the coverage is often more limited.

No-exam life insurance is a good option for those who need a small amount of coverage to help their family with final expenses and don't want to complete an insurance exam, or for those with health issues that may disqualify them from traditional insurance.

Freedom Life Insurance: Hernia Surgery Coverage Explained

You may want to see also

Explore related products

![]()

Should you lose weight before buying life insurance?

Whether you should lose weight before buying life insurance depends on your unique situation and needs. If you're concerned about the cost of your premium, losing weight could help you secure a lower rate. However, it's important to consider the potential drawbacks of delaying your purchase.

Pros of Losing Weight Beforehand

If you're looking to get the best rate possible, losing weight can be an effective strategy. Insurance companies often use height and weight to assess your body mass index (BMI) and determine your risk level. A lower BMI may result in a lower premium. Additionally, losing weight can improve other health factors that insurers consider, such as blood pressure and cholesterol levels.

Cons of Delaying Your Purchase

Waiting to purchase life insurance leaves you and your loved ones unprotected in the event of an unexpected death. Life insurance becomes more expensive as you age, so delaying your purchase could result in higher premiums in the long run. Additionally, losing weight can be challenging, and if you struggle to lose weight or keep it off, you may end up postponing your life insurance coverage indefinitely.

Other Factors to Consider

It's important to remember that weight is just one factor among many that insurers consider when determining your eligibility and rates. Other factors include your age, gender, medical history, family history, and lifestyle choices such as smoking or drinking. Even if you're overweight, if you're otherwise healthy and don't have any weight-related complications, you may still qualify for a policy with a relatively low rate.

Recommendations

If you need life insurance, it's generally recommended to apply and get the coverage you need as soon as possible. If losing weight is part of your health plans and you're concerned about the potential impact on your insurance rates, you can always reconsider your policy and apply for a new one after achieving your weight loss goals. Consulting a licensed life insurance agent can help you better understand your options and make an informed decision about whether to buy a policy now or wait.

How to Get Life Insurance for Your Husband

You may want to see also

Explore related products

![Obesity Medicine Board Review Questions 2025 [ABOM Inspired]: 575+ In-Depth Q&A to Ensure Your Exam Success](https://m.media-amazon.com/images/I/61Zu-Q+yJeL._AC_UL320_.jpg)

![]()

What are the best life insurance companies for overweight people?

While being overweight or obese can increase your life insurance rates, it's unlikely that you'll be rejected for coverage unless you have severe weight-related health issues. If you're in good health, there are several companies that offer competitive rates for overweight people. Here are some of the best life insurance companies for overweight individuals:

- Banner Life Insurance Company: Known for their superior rates for people who are overweight and obese, along with a quick application process, and 35 and 40-year level term policies. They are also a good choice for type II diabetics seeking affordable term life insurance.

- Protective Life Insurance: Offers a wide range of products, both term and permanent, and affordable rates for overweight and obese individuals. They also specialise in applicants with circulatory issues or heart disease.

- AIG (American General): Offers excellent underwriting practices for people with health conditions, mostly term life insurance with great customisation, riders, and benefits. They are also a great choice for females over 60 due to their competitive rates.

- Pacific Life: Provides some of the best life insurance rates for obese people, with a quick and easy online application process, offering both term and multiple types of permanent life insurance. Their rates are among the least expensive in the industry.

- Prudential: Known for their affordable life insurance rates for people with pre-existing conditions, including diabetes and heart disease, especially for those under 65. They also have lenient build guidelines, which can be beneficial for overweight individuals.

It's important to note that rates and policies can vary significantly between companies, so it's recommended to work with an independent agent who can help you compare quotes and find the best option for your specific needs and circumstances.

Shelter Insurance: Life Insurance Options and Availability

You may want to see also

Frequently asked questions

Weight is just one aspect of your health. A person who is overweight but otherwise healthy will probably still be able to get coverage. If you are overweight and have other medical issues or complicating factors such as a pre-existing condition, risky hobbies, or a history of smoking, you may face issues in terms of obtaining coverage.

Life insurance is extremely personalized. Insurance experts recommend exploring your options to see which life insurance provider offers the best coverage and pricing for your medical condition. Your weight might not affect which type of coverage you choose, but your other circumstances might.

You should always be truthful when filling out a life insurance application. If you are purchasing a policy that requires a medical exam, the insurance company will find out about your weight anyway. Intentionally lying about your weight to avoid paying a higher premium for overweight life insurance could result in your application being denied.