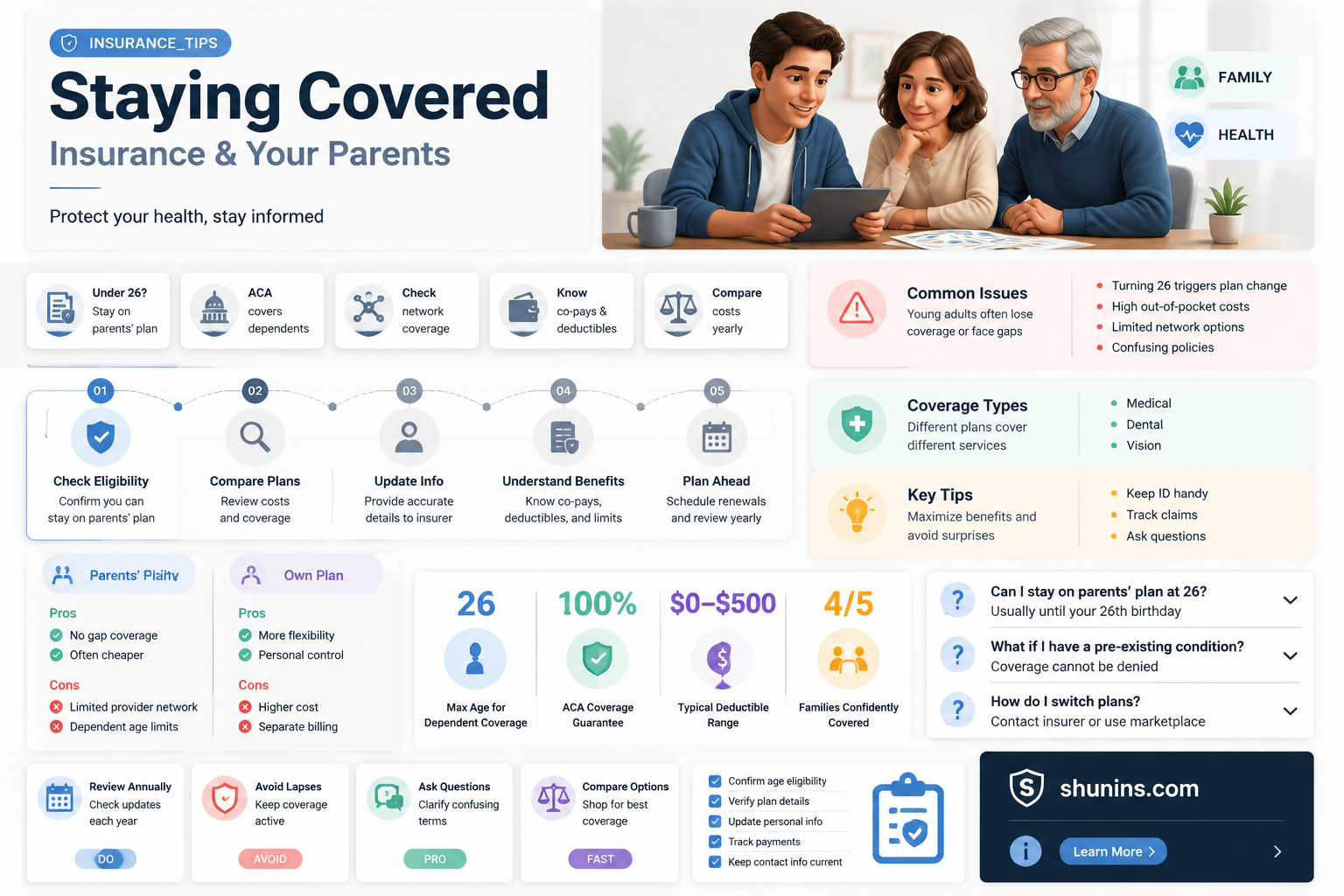

In the United States, you can typically remain on your parent's health insurance plan until you turn 26. However, the specific rules vary depending on the state you live in and the type of insurance plan your parents have. If you have coverage through your parent's employer plan, you are usually covered until the end of the month of your birthday. On the other hand, if your parents have a marketplace plan, you can stay on their insurance until December 31 of the year you turn 26. While most states require adults to obtain their own insurance by age 26, a few states, like Florida, Illinois, and New York, allow young adults to remain on their parent's plan beyond this age. Losing health insurance qualifies you for a special enrollment period, during which you can explore alternative insurance options, such as employer-sponsored plans, Affordable Care Act (ACA) marketplace plans, or Medicaid, if you meet the eligibility criteria.

| Characteristics | Values |

|---|---|

| Until what age can one be under their parent's insurance? | Until the age of 26. However, some states allow parents to keep their children on their plans longer, such as Florida, Illinois, Nebraska, New Jersey, New York, Pennsylvania, South Dakota, and Wisconsin. |

| What are the types of insurance that allow this? | ACA/Marketplace/Healthcare.gov plans. |

| What are the alternatives after turning 26? | Employer-sponsored benefits, Affordable Care Act (ACA) marketplace plan, catastrophic health insurance plan, or Medicaid. Student health plans are also available for those under 30. |

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

What You'll Learn

![]()

Getting your own insurance

In the United States, you can usually be added to your parents' health insurance plan and remain on it until you turn 26. However, once you turn 26, you will need to purchase your own health insurance plan. Here are some options for getting your own insurance:

- Job-based health insurance plan: If you are employed, you may be able to enrol in your job's health insurance plan. Employers typically pay a portion of the premium, but you will be responsible for paying the remaining amount. It is recommended to contact your job's human resources department to understand your options and next steps.

- Health Insurance Marketplace Plan: The federal government operates the Health Insurance Marketplace, and some states have their own marketplaces as well. You can apply for a plan through HealthCare.gov or your state's marketplace website. The open enrollment period for marketplace plans is typically from November 1 to January 15 each year.

- Medicaid or the Children's Health Insurance Program (CHIP): Depending on your income level, you may be eligible for Medicaid or CHIP. These plans are independent of your employer, so you will need to pay the premium yourself. You can find out if you qualify for these programs during the application process for a marketplace plan.

- Student Health Plans: If you are under 30 and enrolled in school, you may be eligible for a student health plan. Contact your school's health services department to explore this option.

- Special Enrollment Period: If you are currently on your parent's job-based plan, you may qualify for a Special Enrollment Period. This allows you to enrol in or change marketplace plans outside of the open enrollment period. The Special Enrollment Period starts 60 days before you lose coverage and ends 60 days after.

It is important to note that health insurance regulations can vary by state, so it is recommended to review the specific rules and options available in your state. Additionally, be cautious of products that are not considered health insurance, such as health care sharing ministries (HCSMs), discount plans, or risk-sharing plans, as they may not provide the same level of consumer protection as insurance plans.

Insurers: Tort Reform Opponents?

You may want to see also

Explore related products

$19.13 $19.95

![]()

Special Enrollment Period

In the United States, you can usually be added to your parent's health insurance plan as a dependent and remain on their plan until you turn 26. When you lose coverage on your 26th birthday, you qualify for a Special Enrollment Period. This is a period of time outside of the yearly Open Enrollment Period when you can enrol in or change Marketplace plans.

The Special Enrollment Period lets you sign up for a health plan directly through providers such as Cigna Healthcare or on the Health Insurance Marketplace. You can qualify for a Special Enrollment Period if you've had certain life events, including losing health coverage, moving, getting married, having a baby, or adopting a child.

If you lose your health coverage through your employer or the employer of a family member, you may qualify for a Special Enrollment Period. This includes losing health coverage through a parent because you're no longer a dependent. If you choose to drop the coverage you have as a dependent, that alone doesn't qualify you for a Special Enrollment Period. However, you may qualify if you also had a decrease in household income or a change in your previous coverage that made you eligible for savings on a Marketplace plan.

Your special enrollment period for choosing a health insurance plan is a 4-month window. Ask your parents to check their employee handbooks or ask their HR department when your coverage will end. You can also contact the health insurance company directly to ask when coverage ends. If you've been covered by your parents' Affordable Care Act (ACA) plan, your coverage will not end until the last day of the calendar year. However, you can purchase your own health insurance during open enrollment, which is typically between November and the end of January.

Term Life Insurance: Do You Have Coverage?

You may want to see also

Explore related products

![]()

Student health plans

In the United States, if your parent's health insurance plan covers dependents, you can usually be added to their plan and remain on it until you turn 26. Once you turn 26, you will need to find your own health insurance coverage.

If you are a student, you may be eligible for a student health plan if you are enrolled in school and under 30. Contact your school's health services department to explore this option. Most universities offer health insurance, as it is required for students on campus to have it. You can also purchase private insurance, which will be subsidized by the government if you cannot afford it.

If you have a job, you may be able to get insurance through your employer. If you do not make enough to qualify for insurance through your employer, you can apply for Medicaid through your state, which is free if you qualify.

If you are on your parent's Marketplace plan, your coverage will end on December 31 of the year you turn 26. If you want to enroll in your own Marketplace plan, you can do so during open enrollment (November 1 - January 15 every year). You can apply for Marketplace coverage on your own or with your parent. However, if you apply with your parent, you may need to choose a separate plan because you are 26 or older.

The Health Insurance Marketplace provides several options for those under 30, allowing you to be in control of your coverage and care.

Gassaway Allied Insurance: The Ultimate Guide to Coverage

You may want to see also

Explore related products

![]()

State-specific rules

In the United States, federal law allows children to remain on their parents' health insurance plans until they turn 26. This applies to all plans in the individual market and to all employer plans. However, there may be state-specific variations and exceptions to this rule.

In some states, children can remain on their parents' health insurance plans beyond the age of 26. For example, New York and Florida allow coverage until the child turns 30. Other states, such as Colorado, do not allow coverage past the age of 26. It's important to note that certain requirements must be met in these states, such as being unmarried, a veteran, or living with your parents.

Additionally, some states allow disabled dependents to remain on their parents' health insurance plans indefinitely. This provision varies depending on the state and its specific laws.

If you are approaching your 26th birthday and are currently covered by your parents' insurance, it is essential to understand the specific rules and regulations of your state. Losing coverage at 26 is considered a qualifying life event (QLE), allowing you to qualify for a special enrollment period (SEP) and enroll in a new plan right away.

To summarize, while federal law sets the minimum age limit for dependent coverage at 26, certain states have adopted their own requirements and exceptions. These variations can include extending coverage beyond 26 or accommodating special circumstances, such as disability. Therefore, it is advisable to consult your parents' insurance provider and state laws to understand the specific coverage details applicable to your situation.

Disputing Life Insurance Denials: Your Options Explained

You may want to see also

Explore related products

![Report on the effectiveness of financing and selected eligibility, job search, and benefit payment operations of the unemployment insurance program : State of Montana, Department of La [Leather Bound]](https://m.media-amazon.com/images/I/81nNKsF6dYL._AC_UY218_.jpg)

![]()

Losing coverage at 26

In the United States, if your parent's health insurance plan covers dependents, you can usually be added to their plan and remain on it until you turn 26. However, once you reach the age of 26, you will need to take action to secure your own health coverage. The specific steps you need to take will depend on your individual circumstances and the state in which you reside.

If you are on your parent's Marketplace plan, your coverage will typically end on December 31 of the year you turn 26, regardless of your birthday. To ensure continuous coverage, you should enroll in your own Marketplace plan during the open enrollment period, which runs from November 1 to January 15 every year. You qualify for a Special Enrollment Period, which is a period outside of Open Enrollment when you can enroll in or change Marketplace plans. This Special Enrollment Period starts 60 days before you lose coverage and ends 60 days after, allowing you to avoid any gaps in coverage.

If you are on your parent's employer-based plan, your coverage will generally last through the month of your 26th birthday. For example, if your birthday is on May 1, your coverage will be effective until May 31. In this case, you should contact your parent's employer to confirm the exact date your coverage will end. Additionally, if your employer offers health insurance, you may qualify to enroll outside of their yearly Open Enrollment period if you lost your parent's coverage due to turning 26. Reach out to your company's human resources department before your birthday to understand your options and next steps.

It is important to note that some states and plans have different rules regarding dependent coverage. Therefore, it is always a good idea to check with the insurance provider or your parent's employer to confirm the specific details of your coverage. Additionally, if you are a student, you may have additional options, such as student health plans offered by your university or college. These plans can provide affordable coverage specifically designed for students.

Life Insurance Payouts After Suicide: What Spouses Need to Know

You may want to see also

Frequently asked questions

Yes, you can typically stay on a parent’s health insurance until you turn 26.

When you turn 26, you may lose health insurance immediately, at the end of the month, or at the end of the year depending on the plan and state. You can enroll in your own insurance plan during the open enrollment period (Nov 1 – Jan 15 every year).

Yes, eight states allow young adults to apply to stay on their parent’s plan beyond age 26. These states are Florida, Illinois, Nebraska, New Jersey, New York, Pennsylvania, South Dakota, and Wisconsin.