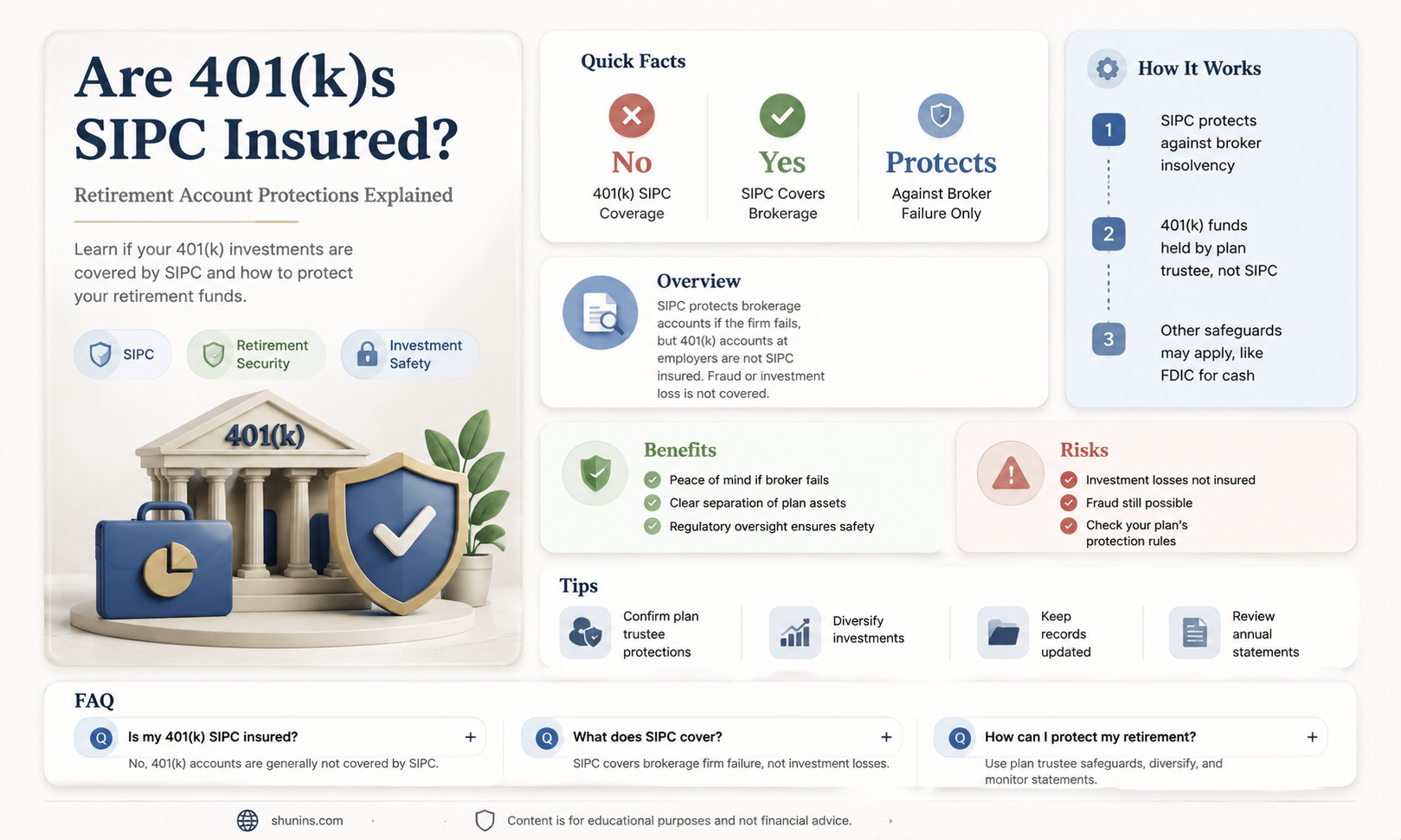

When considering the safety of retirement savings, many investors wonder whether their 401(k) plans are protected by the Securities Investor Protection Corporation (SIPC). Unlike individual brokerage accounts, 401(k)s are typically not directly covered by SIPC insurance, which primarily safeguards assets held by brokerage firms in case of their failure. Instead, 401(k) plans are generally protected by the Employee Retirement Income Security Act (ERISA) and may also be insured by the Pension Benefit Guaranty Corporation (PBGC) for defined benefit plans. Additionally, assets held in 401(k)s are often custodied by large financial institutions that have their own safeguards and insurance policies. Understanding these protections is crucial for investors seeking peace of mind about the security of their retirement funds.

| Characteristics | Values |

|---|---|

| SIPC Insurance Coverage | 401(k) plans are not covered by the Securities Investor Protection Corporation (SIPC). SIPC insurance typically protects assets held in brokerage accounts, but it does not extend to retirement plans like 401(k)s. |

| Type of Protection | 401(k) plans are generally protected by the Employee Retirement Income Security Act (ERISA), which sets standards for retirement plans, including fiduciary responsibilities and participant rights. |

| FDIC Insurance | If a 401(k) includes cash holdings in a bank account, that portion may be insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 per depositor, per insured bank. |

| Additional Safeguards | Many 401(k) plans are also protected by fiduciary bonds or ERISA bonds, which provide additional insurance against fraud or mismanagement by plan administrators. |

| Investment Risks | While the principal in a 401(k) is protected from brokerage failure, the investments within the plan (e.g., stocks, bonds) are subject to market risks and are not insured against losses. |

| Plan Sponsor Responsibility | Employers or plan sponsors are responsible for ensuring compliance with ERISA and selecting reputable financial institutions to manage 401(k) assets. |

| Participant Protections | Participants have legal recourse under ERISA if plan assets are mismanaged or if fiduciaries breach their duties. |

| SIPC vs. ERISA | SIPC focuses on brokerage account protection, while ERISA provides broader oversight and protection for retirement plans like 401(k)s. |

Explore related products

What You'll Learn

- SIPC Coverage Limits: SIPC insures up to $500,000 per customer, including $250,000 for cash

- (k) Exclusion: SIPC does not cover 401(k) plans; they are protected by ERISA and FDIC

- Brokerage vs. Retirement: SIPC covers brokerage accounts, not retirement accounts like 401(k)s

- Theft vs. Market Loss: SIPC protects against theft or brokerage failure, not market losses

- Alternative Protections: 401(k)s are safeguarded by ERISA and FDIC insurance for cash holdings

![]()

SIPC Coverage Limits: SIPC insures up to $500,000 per customer, including $250,000 for cash

The Securities Investor Protection Corporation (SIPC) provides a crucial safety net for investors, but it’s important to understand its coverage limits and how they apply to different types of accounts, including 401(k)s. SIPC insures up to $500,000 per customer at a brokerage firm, with a maximum of $250,000 of that coverage allocated for cash claims. This protection is designed to safeguard investors in the event a brokerage firm fails and customer assets are missing. However, SIPC coverage does not apply to 401(k) plans because these retirement accounts are typically held by banks, mutual fund companies, or other financial institutions, not brokerage firms. Instead, 401(k)s are protected by the Employee Benefits Security Administration (EBSA) and the Federal Deposit Insurance Corporation (FDIC) or the Pension Benefit Guaranty Corporation (PBGC), depending on the type of assets held.

SIPC coverage is specifically tailored to brokerage accounts, where investors buy and sell securities like stocks, bonds, and mutual funds. The $500,000 limit per customer includes both securities and cash, with the $250,000 cap on cash claims ensuring that investors have protection for both asset types. For example, if a brokerage firm fails and an investor has $300,000 in securities and $200,000 in cash, SIPC would cover the full amount. However, if the investor had $400,000 in cash, only $250,000 of that would be covered, with the remaining $150,000 potentially at risk. This structure highlights the importance of understanding SIPC’s limits and how they apply to your investments.

While SIPC coverage is robust for brokerage accounts, it’s essential to recognize that 401(k) plans operate under different protections. Most 401(k)s are not held at brokerage firms, so SIPC insurance does not apply. Instead, these plans are often covered by the FDIC for cash holdings or the PBGC for pension benefits. For instance, if a 401(k) includes a cash balance, the FDIC insures up to $250,000 per depositor, per insured bank. Similarly, the PBGC provides insurance for defined benefit pension plans, ensuring participants receive their promised benefits if the plan sponsor fails. Understanding these distinctions is critical for investors to ensure their retirement savings are adequately protected.

Investors should also be aware that SIPC coverage does not protect against market losses or fraudulent activities like theft or misappropriation of funds. Its primary purpose is to restore missing assets when a brokerage firm becomes insolvent. For 401(k) holders, the focus should be on the protections offered by the FDIC, PBGC, or other regulatory bodies overseeing retirement plans. Regularly reviewing the insurance coverage for your specific accounts and diversifying investments across protected institutions can further safeguard your financial future.

In summary, SIPC coverage limits of up to $500,000 per customer, including $250,000 for cash, are a vital protection for brokerage account holders. However, 401(k) plans are not SIPC-insured and instead rely on other forms of protection like FDIC insurance or PBGC guarantees. Understanding these differences ensures investors can make informed decisions about where and how to safeguard their retirement savings. Always verify the specific protections for your accounts and consult with a financial advisor if you have questions about coverage limits.

Insurable Interest: Life Insurance's Core Principle Explained

You may want to see also

Explore related products

![]()

401(k) Exclusion: SIPC does not cover 401(k) plans; they are protected by ERISA and FDIC

When considering the safety of retirement savings, it’s crucial to understand the protections in place for different types of accounts. One common question is whether 401(k) plans are insured by the Securities Investor Protection Corporation (SIPC). The straightforward answer is no: 401(k) plans are not covered by SIPC. SIPC insurance is specifically designed to protect customers of brokerage firms in the event of the firm’s failure, covering cash and securities up to $500,000 (including $250,000 for cash). However, 401(k) plans fall outside this scope because they are governed by different regulatory frameworks.

Instead of SIPC, 401(k) plans are primarily protected by the Employee Retirement Income Security Act (ERISA). ERISA is a federal law that sets minimum standards for most voluntarily established retirement and health plans in private industry. It ensures that plan participants receive information about their plans, sets fiduciary responsibilities for those managing the plans, and provides safeguards to protect plan assets. For example, ERISA requires that 401(k) plans be managed prudently and in the best interest of participants, reducing the risk of mismanagement or fraud. While ERISA does not provide insurance like SIPC, it establishes a legal framework to hold plan sponsors and fiduciaries accountable.

In addition to ERISA, certain assets within a 401(k) plan may be protected by the Federal Deposit Insurance Corporation (FDIC). For instance, if a 401(k) plan holds cash in a bank account or invests in FDIC-insured products like certificates of deposit (CDs), those assets are insured up to $250,000 per depositor, per insured bank. However, this protection is limited to cash and cash equivalents held in FDIC-insured institutions and does not extend to stocks, bonds, or mutual funds within the 401(k). It’s important to note that FDIC insurance is not a blanket protection for all 401(k) assets but rather a specific safeguard for qualifying cash holdings.

The exclusion of 401(k) plans from SIPC coverage highlights the importance of understanding the specific protections associated with different types of retirement accounts. While SIPC is relevant for individual brokerage accounts, 401(k) plans rely on ERISA and, in some cases, FDIC insurance for their safeguards. Investors should carefully review their plan documents and consult with financial advisors to fully grasp the protections in place for their retirement savings. This knowledge ensures informed decision-making and peace of mind regarding the security of long-term financial goals.

In summary, 401(k) plans are not SIPC-insured but are instead protected by ERISA and, for certain cash holdings, FDIC insurance. This distinction underscores the need to recognize the regulatory frameworks governing different retirement accounts. By understanding these protections, investors can better navigate the complexities of retirement planning and ensure their savings are safeguarded against potential risks.

Life Insurance 101: Understanding Basc Beneficiaries and Their Rights

You may want to see also

![]()

Brokerage vs. Retirement: SIPC covers brokerage accounts, not retirement accounts like 401(k)s

When considering the safety of your investments, it’s crucial to understand the role of the Securities Investor Protection Corporation (SIPC) and the types of accounts it covers. SIPC is a nonprofit membership corporation that protects investors against financial loss in the event their brokerage firm fails. However, SIPC coverage is not applicable to retirement accounts like 401(k)s. Instead, SIPC primarily insures brokerage accounts, which are distinct from retirement accounts in both structure and purpose. This distinction is vital for investors to grasp, as it directly impacts the level of protection their assets receive.

Brokerage accounts are taxable investment accounts where individuals can buy and sell securities such as stocks, bonds, and mutual funds. These accounts are typically used for short-term or long-term investment goals outside of retirement planning. SIPC coverage applies to brokerage accounts, providing protection of up to $500,000 per customer, including a $250,000 limit for cash claims, in case the brokerage firm goes bankrupt. This coverage ensures that investors can recover their assets if the firm fails, though it does not protect against market losses. In contrast, retirement accounts like 401(k)s are designed for long-term savings and are subject to different regulatory protections.

Retirement accounts, including 401(k)s, IRAs, and pension plans, are not covered by SIPC. Instead, these accounts are often protected by the Employee Benefits Security Administration (EBSA) and may be insured by the Pension Benefit Guaranty Corporation (PBGC) for defined benefit plans. Additionally, assets held in 401(k)s are typically safeguarded by the Employee Retirement Income Security Act (ERISA), which sets standards for fiduciary responsibility and ensures that plan participants receive their benefits. While these protections provide a safety net, they operate differently from SIPC and do not cover the same types of risks.

The key difference between brokerage and retirement accounts lies in their purpose and regulatory framework. Brokerage accounts are more flexible and used for general investing, while retirement accounts are tax-advantaged and strictly regulated to ensure long-term savings for retirement. Since SIPC coverage is limited to brokerage accounts, investors with 401(k)s or other retirement accounts should not assume their assets are protected under SIPC. Instead, they should rely on the specific protections provided by ERISA, EBSA, or other relevant agencies.

In summary, understanding the difference between brokerage and retirement accounts is essential for investors to know what protections apply to their assets. SIPC covers brokerage accounts, offering a safety net in case of brokerage firm failure, but it does not extend to retirement accounts like 401(k)s. Retirement accounts have their own set of protections under federal laws and agencies, ensuring that participants’ savings are safeguarded. By recognizing these distinctions, investors can make informed decisions about where to hold their assets and how to maximize their financial security.

Longer-Term Life Insurance: Cheaper Option?

You may want to see also

![]()

Theft vs. Market Loss: SIPC protects against theft or brokerage failure, not market losses

When considering the protection of your 401(k) investments, it’s crucial to understand the role of the Securities Investor Protection Corporation (SIPC). SIPC insurance is designed to protect investors against financial loss in the event of brokerage firm failure or theft, but it does not cover market losses. This distinction is vital for 401(k) holders, as it clarifies what risks are mitigated and which remain the investor’s responsibility. SIPC coverage ensures that if a brokerage firm goes bankrupt or assets are stolen, investors can recover their cash and securities, up to $500,000 per customer, with a $250,000 limit for cash. However, this protection does not extend to fluctuations in the market that cause the value of your investments to decline.

Theft and brokerage failure are specific risks that SIPC addresses. For instance, if a brokerage firm misappropriates client funds or collapses due to mismanagement, SIPC steps in to restore investors’ assets. This safeguard is particularly relevant for individual investors who rely on brokerage firms to manage their retirement accounts. However, it’s important to note that 401(k) plans are typically held by plan administrators or recordkeepers, not individual brokerage accounts. As a result, SIPC coverage generally does not apply directly to 401(k)s, as these plans are protected under different federal laws, such as ERISA, which provides fiduciary oversight and insurance through the Pension Benefit Guaranty Corporation (PBGC) for defined benefit plans, though not for investment losses.

Market losses, on the other hand, are inherent risks of investing and are not covered by SIPC. When the value of your 401(k) investments drops due to economic downturns, poor market performance, or other external factors, SIPC insurance does not provide reimbursement. This is a critical point for investors to understand, as it emphasizes the importance of diversification and informed decision-making to manage market risks. While SIPC protects against the failure of the institution holding your investments, it cannot shield you from the volatility of the markets themselves.

For 401(k) investors, the lack of SIPC coverage for market losses means that their primary protection against investment declines lies in prudent financial planning. Diversifying assets, regularly reviewing portfolio allocations, and understanding the risks associated with different investments are essential strategies. Additionally, 401(k) plans often include additional safeguards, such as fiduciary protections and oversight, to ensure that plan administrators act in the best interests of participants. However, these measures do not guarantee against market losses, which remain an unavoidable aspect of investing.

In summary, SIPC insurance is a valuable safeguard against theft and brokerage failure, but it does not protect 401(k) investors from market losses. Understanding this distinction is key to managing expectations and risks effectively. While 401(k) plans are not directly covered by SIPC, they benefit from other regulatory protections. Investors should focus on educating themselves about market risks and adopting strategies to minimize potential losses, recognizing that SIPC’s role is limited to specific scenarios of institutional failure or fraud. By grasping these nuances, 401(k) holders can make more informed decisions to secure their retirement savings.

Best Value Life Insurance: Maximum Coverage, Minimum Dollars

You may want to see also

![]()

Alternative Protections: 401(k)s are safeguarded by ERISA and FDIC insurance for cash holdings

While 401(k)s are not protected by the Securities Investor Protection Corporation (SIPC), as SIPC insurance primarily covers brokerage accounts holding stocks, bonds, and other securities, these retirement plans have alternative safeguards in place to protect participants' assets. One of the primary protections is the Employee Retirement Income Security Act (ERISA), a federal law that sets minimum standards for most voluntarily established retirement and health plans in private industry. ERISA requires plans to engage in fiduciary practices, meaning those managing the plan must act in the best interest of participants and beneficiaries. This includes prudent management of assets and avoidance of conflicts of interest. Additionally, ERISA mandates that plans provide participants with important information about their rights and features, ensuring transparency and accountability.

Another layer of protection for 401(k)s comes from the Federal Deposit Insurance Corporation (FDIC) insurance, but this applies specifically to cash holdings within the plan. If a 401(k) plan holds cash in a bank account, such as in a money market fund or stable value fund, that cash is insured by the FDIC up to $250,000 per depositor, per insured bank, for each account ownership category. This ensures that even if the bank fails, the cash portion of the 401(k) remains protected. However, it’s important to note that FDIC insurance does not cover investments in stocks, bonds, or mutual funds, which are the primary components of most 401(k) portfolios.

ERISA also provides a mechanism for additional protection through bond requirements for plan fiduciaries. Fiduciaries, including those who handle plan funds, are often required to be bonded to protect against losses due to fraud or dishonesty. This bonding acts as a form of insurance, ensuring that participants are compensated if a fiduciary mismanages or steals plan assets. While this does not protect against market losses, it adds a critical layer of security against internal malfeasance.

Furthermore, many 401(k) plans offer additional safeguards through the selection of reputable investment providers and custodians. These entities often have their own internal controls and insurance policies to protect assets. For example, custodians may carry private insurance to cover losses beyond what ERISA or FDIC insurance provides. Participants should review their plan documents to understand the specific protections offered by their plan’s custodian or administrator.

In summary, while 401(k)s are not SIPC insured, they are protected by a robust framework of alternative safeguards. ERISA ensures fiduciary responsibility, transparency, and participant rights, while FDIC insurance covers cash holdings up to certain limits. Additional protections, such as fiduciary bonding and custodial insurance, further enhance the security of these retirement plans. Understanding these layers of protection can provide participants with confidence in the safety of their 401(k) investments.

Life Insurance: Third-Party Administrators Explained

You may want to see also

Frequently asked questions

No, 401(k) plans are not insured by the Securities Investor Protection Corporation (SIPC). SIPC insurance typically covers brokerage accounts, not retirement plans like 401(k)s.

401(k) plans are protected by federal laws, such as ERISA (Employee Retirement Income Security Act), and are often covered by fiduciary insurance or bonds held by plan administrators to safeguard assets.

SIPC insurance generally applies to brokerage accounts, including IRAs held at SIPC-member firms, but not to employer-sponsored plans like 401(k)s.

If a 401(k) plan provider goes bankrupt, your assets are typically held in a trust separate from the provider’s assets, ensuring they remain protected and accessible to you.