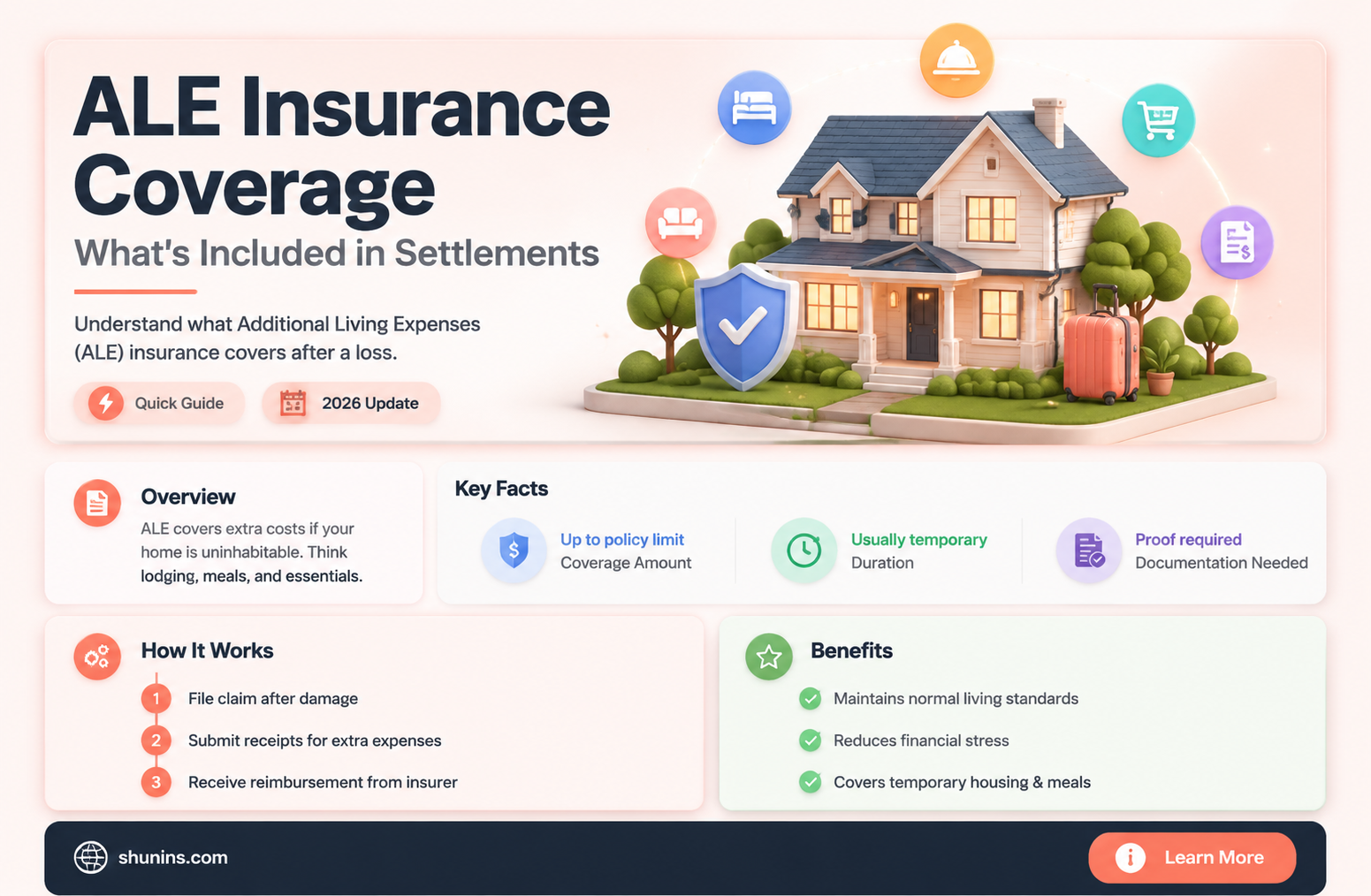

Additional living expense (ALE) insurance is an important component of insurance settlements, providing coverage for expenses incurred when an insured person is temporarily displaced from their home. ALE reimburses policyholders for the additional costs of maintaining their pre-loss standard of living, including temporary housing, increased food expenses, transportation costs, and laundry services. It is essential for policyholders to understand the nuances of ALE coverage, as it can vary between renters and homeowners insurance policies and is subject to specific conditions and exclusions. Proper documentation and organisation of receipts are crucial for successful ALE claims, ensuring reimbursement for the full extent of additional living expenses incurred during the recovery process.

| Characteristics | Values |

|---|---|

| Definition | Additional Living Expenses (ALE) coverage in homeowners insurance reimburses policyholders for extra expenses incurred when a covered event forces them to leave their home temporarily. |

| Coverage | ALE covers expenses such as hotel stays, rental accommodations, increased food expenses, transportation costs, laundry services, pet boarding, commuting costs, and lost rental income during repairs. |

| Exclusions | ALE does not cover expenses related to regular maintenance, wear and tear, uninsured events (e.g., earthquakes or floods), preventable losses, or illegal activities. Planned renovations or voluntary moves are also not eligible for ALE coverage. |

| Conditions | To be eligible for ALE, the loss must be covered under the policy and comply with its conditions. The property must be deemed "uninhabitable," requiring occupants to leave the residence due to factors such as structural damage, lack of utilities, or compliance issues with local codes. |

| Monetary Cap | ALE coverage may or may not have a monetary cap. Policyholders should verify the specifics of their policy. |

| Reimbursement Process | Policyholders should keep detailed records of expenses, separate bank accounts, and organize receipts to facilitate the reimbursement process. Only the additional costs incurred due to displacement are eligible for reimbursement. |

Explore related products

What You'll Learn

![]()

ALE covers temporary housing costs

Additional Living Expenses (ALE) coverage is a part of homeowners insurance policies. It covers temporary housing costs if your home is uninhabitable due to a covered loss. This includes situations where your home is damaged by a fire, storm, water damage, or smoke damage, and is deemed unsafe to live in or perform everyday tasks. ALE provides reimbursement for expenses that exceed your normal living costs, such as temporary housing, hotel stays, rental accommodations, increased food expenses, transportation costs, and laundry services. It is important to note that ALE does not cover regular expenses such as utility bills or groceries, and there are limits to the reimbursement amounts.

ALE coverage aims to maintain your pre-loss standard of living without enhancing it. For example, if you previously cared for your pet at home and now need to pay for pet boarding, the entire amount is typically reimbursable. Similarly, if your temporary housing increases your commute, additional fuel or transportation costs will be covered. ALE may also compensate for lost rental income during repairs if you rented out a part of your home that is now uninhabitable due to a covered loss.

It is important to carefully review your insurance policy to understand the specific terms and coverage limits of your ALE benefits. The amount of reimbursement for temporary housing costs under ALE is typically a percentage of your homeowners insurance dwelling coverage. Standard ALE coverage is around 20% of the dwelling coverage, but this may vary, and you may be able to increase this amount.

When it comes to choosing temporary housing, ALE Solutions is a trusted provider of technology-based temporary housing solutions for displaced policyholders. They work with insurance adjusters to find comfortable and cost-effective temporary housing options, including extended-stay hotels and long-term housing. Policyholders can also use the MyALE HOME app to manage their temporary housing arrangements and expenses easily.

Overall, ALE coverage plays a crucial role in alleviating the financial burden of temporary living costs when individuals are forced to leave their homes due to unforeseen events. By providing reimbursement for expenses beyond normal living costs, ALE helps individuals maintain their standard of living during challenging times.

Life Insurance: Loss Ratios and Their Absence Explained

You may want to see also

Explore related products

![]()

ALE covers increased food expenses

Additional Living Expenses (ALE) coverage is a critical component of homeowners' and renters' insurance policies, offering financial support to policyholders facing temporary displacement from their residences. It is designed to maintain an individual's standard of living by covering the additional costs incurred when they cannot live in their primary residence due to an insured disaster or covered peril.

ALE coverage is often included in homeowners' insurance policies and, in some cases, renters' insurance policies. It is meant to alleviate the financial strain of temporary living costs, ensuring that individuals can maintain their normal standard of living while their primary residence is being repaired or rebuilt. This coverage is typically triggered by specific events, such as fire, smoke damage, water damage, or other insured incidents that render a home uninhabitable.

One of the key aspects of ALE coverage is that it includes increased food expenses. When individuals are forced to leave their homes and stay in temporary accommodations, they may not have access to cooking facilities. As a result, they may need to dine out or purchase meals more frequently, leading to increased food expenses beyond what they would typically spend.

ALE coverage recognises this additional financial burden and provides reimbursement for dining out or purchasing meals when temporary housing lacks cooking facilities. It is important to note that ALE only covers the incremental costs above what an individual would normally spend on food. Proper documentation and receipts are crucial for claiming reimbursement, allowing policyholders to provide evidence of their increased food expenses.

In summary, ALE coverage plays a vital role in helping individuals maintain their standard of living during challenging times. By including increased food expenses, it ensures that individuals can access meals and maintain their nutritional needs without incurring excessive financial strain while they are temporarily displaced from their homes.

Wire Transfer Insurance: What's Covered and What's Not

You may want to see also

Explore related products

![]()

ALE covers transportation costs

Additional living expense (ALE) insurance covers the additional costs incurred by a policyholder who is temporarily displaced from their residence. It is a standard component of many homeowners', condominium owners', and renters' insurance policies. ALE is also known as "loss of use" coverage, and it reimburses policyholders for extra expenses that exceed their normal living costs.

ALE coverage is typically set at a percentage of the dwelling coverage in a homeowner's insurance policy. For example, if the dwelling coverage is $200,000, the ALE coverage limit is often 20%, or $40,000. Policyholders should be aware of this limit, as it caps the amount an insurer will reimburse for incurred additional living expenses due to a covered loss.

To be eligible for ALE coverage, the homeowner's insurance policy must include it, often found under the \"loss of use\" section. To file an ALE insurance claim, contact your insurance provider and inform them about the covered event and your displacement. Submit the necessary documentation, such as receipts and evidence of the loss, to support your claim.

Drunk Driving and Insurance: What's Covered?

You may want to see also

Explore related products

![]()

ALE covers laundry costs

Additional Living Expenses (ALE) coverage is part of your insurance settlement. It is designed to alleviate the financial burden of temporary living costs incurred when a covered event forces you to leave your home temporarily. ALE covers expenses such as hotels, car rentals, meals, and other costs you may incur while your home is being repaired.

It is important to note that not every inconvenience qualifies for ALE coverage. Insurance companies typically require a clear, covered event, such as a kitchen fire, storm damage, water damage, or smoke damage, to trigger the benefit. ALE reimburses reasonable expenses that exceed your normal living costs, so it is essential to understand the specific terms and conditions of your insurance policy to determine what is covered.

The cost of laundry services can vary depending on the provider and the specific services offered. Some companies offer standard or express laundry services, with prices ranging from $1/lb to $2/lb, respectively. There may also be additional charges for oversized items or minimum order requirements. It is recommended to review the pricing and services offered by different laundry providers to find the best option for your needs.

By understanding the coverage provided by ALE and the costs associated with laundry services, you can effectively manage your expenses during temporary displacement from your home. ALE is designed to help maintain your pre-loss standard of living, ensuring that you are reimbursed for necessary additional costs incurred during this challenging time.

Life Insurance Proceeds: Texas Probate Exemption

You may want to see also

Explore related products

![]()

ALE is paid directly to the insured person

Additional Living Expenses (ALE) coverage is a crucial component of homeowners' insurance policies, offering financial assistance during challenging periods. ALE is designed to alleviate the financial burden of temporary living costs when a policyholder is forced to leave their home due to unforeseen circumstances. This type of coverage is typically included in homeowners' or renters' insurance policies and can provide reimbursement for a range of expenses.

When an insured person is temporarily displaced from their home, ALE coverage helps cover the additional costs they may incur. This includes expenses such as temporary housing, meals, transportation, and other necessities. For example, if a policyholder needs to stay in a hotel or rent a temporary apartment while their primary residence is being repaired, ALE will cover those costs. It is important to note that ALE is intended to maintain the policyholder's pre-loss standard of living and is not meant to enhance their lifestyle during the displacement.

ALE coverage is typically triggered by specific events, such as fire, smoke damage, water damage, or other insured incidents. It is important to understand that not every inconvenience qualifies for ALE reimbursement. Insurance companies usually require a clear, covered event to trigger the benefit. Additionally, ALE coverage may have a monetary limit, so it is essential to review your policy carefully to understand the extent of your coverage.

To maximize their ALE settlement, policyholders should keep track of all expenses incurred during their displacement. This includes rent for a temporary rental property, hotel expenses, meals and groceries, transportation costs, and any other relevant costs. By organizing and documenting these expenses, policyholders can effectively support their ALE claim and receive reimbursement for their additional living expenses.

Life Insurance: A Generational Inheritance?

You may want to see also

Frequently asked questions

ALE stands for Additional Living Expenses.

ALE covers expenses incurred when a covered peril forces you to leave your home temporarily. This includes things like hotel stays, restaurant meals, commuting costs, and laundry services.

ALE applies when your home is damaged and deemed unsafe to live in due to events such as a kitchen fire, structural damage, water damage, or smoke damage. It is important to note that planned renovations or voluntary moves are not eligible for ALE coverage.

To make a claim for ALE, you must first ensure that the loss suffered is covered under your particular policy. Keep all your receipts and documentation for expenses incurred due to displacement, as these are necessary for filing a claim and ensuring you receive the appropriate reimbursement.