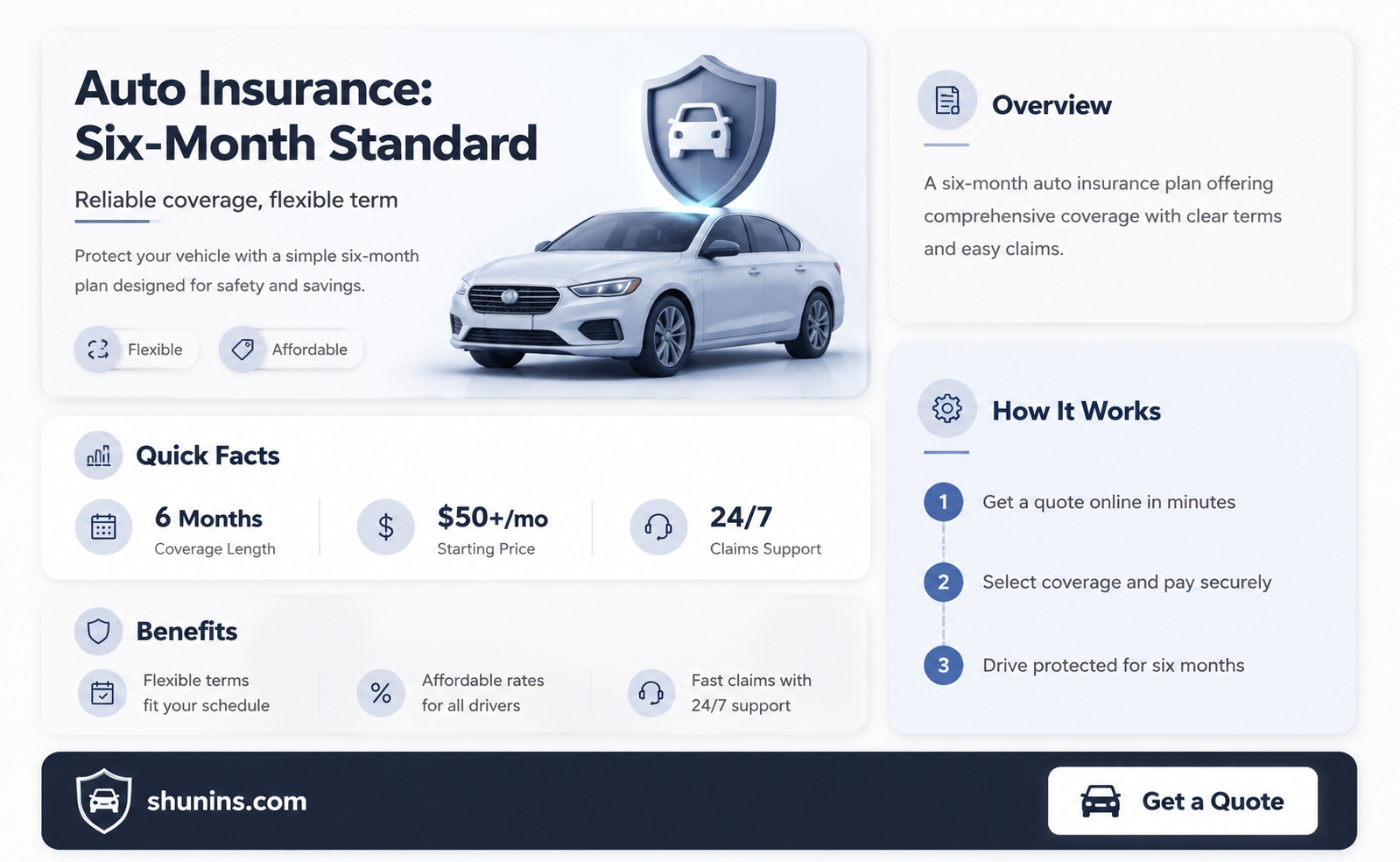

Auto insurance policies typically come in two durations: six months and 12 months. Six-month policies are more common, as they allow insurance companies to easily recalculate rates, factoring in routine price revisions and changes to your driving profile. This means that if you have traffic violations that fall off your driving record before your current policy expires, you may see a cheaper premium when you renew. However, a 12-month policy might be preferable if you want to lock in your rate for a full year.

| Characteristics | Values |

|---|---|

| Policy duration | 6 months |

| Review frequency | Twice per year |

| Cost | Less if paid in full |

| Pros | Policy flexibility, driving activity re-evaluated more frequently, paying in full may be more accessible |

| Cons | More frequent premium recalculations, potential to forget renewal dates, possible missed discounts |

Explore related products

What You'll Learn

![]()

Six-month policies are more common than 12-month policies

Six-month auto insurance policies are more common than 12-month policies, as they allow insurance companies to easily recalculate rates, factoring in routine price revisions and changes to your driving profile.

Benefits of a six-month policy

A six-month car insurance policy comes with two primary benefits: additional flexibility and frequent rate revisions.

Additional flexibility

Although you are not locked into your car insurance policy, a shorter policy period provides more flexibility than an annual policy. If you're unhappy with your current insurance provider but want to avoid cancellation fees or a lapse in coverage, you can simply non-renew at the end of your six-month term.

Frequent rate revisions

Depending on your driving record, more frequent premium reviews can save you money. Most at-fault accidents remain on your insurance record for three to five years. If a violation is set to fall off your record midway through your policy, most insurance companies will not adjust your premium until the policy period ends or you specifically ask. A shorter policy duration allows penalties to "fall off" your record more quickly.

Cons of a six-month policy

Potential for higher rates

Most car insurance companies charge slightly higher premiums for six-month policies due to the administrative costs of more frequent renewals.

Increased risk of a lapse

With more renewals, the chance of forgetting to renew and experiencing a coverage gap is higher.

No long-term stability

You might miss out on car insurance discounts offered for loyal customers with 12-month car insurance policies.

More administrative hassle

You'll deal with renewals, paperwork, and potentially new car insurance costs more often.

Medical Payments Coverage: Auto Insurance Essential?

You may want to see also

Explore related products

![]()

Six-month policies allow for more frequent rate revisions

Six-month auto insurance policies are more common than 12-month policies, as they allow insurance companies to recalculate rates more frequently. This means that if your driving record improves, you could benefit from lower rates sooner than with an annual policy.

More frequent rate revisions

Insurance companies typically revise their rates at the end of the policy period. A shorter policy duration means that this rate revision will happen twice a year, rather than once with an annual policy. This can work in your favour if your driving record has improved. For example, if you haven't filed a claim or any traffic violations are due to be removed from your record, you may get a lower rate when you renew your six-month policy.

Easier to pay in full

Some insurance carriers offer discounts for customers who pay their policy in full upfront, rather than in monthly instalments. While this option is available for both six and 12-month policies, paying for a full year upfront may not be possible for everyone. A six-month policy could make paying in full more accessible and may also entitle you to a discount.

More flexibility

A shorter policy period gives you more flexibility than an annual policy. If you're unhappy with your current insurance provider but want to avoid cancellation fees or a lapse in coverage, you can simply choose not to renew at the end of your six-month term.

Less risk of missing a payment

With a 12-month policy, you have the option to pay the entire expense of your policy upfront for the whole year. With a six-month policy, you may be more likely to forget your renewal dates, as they occur twice a year. This could mean that you potentially miss a payment, causing a lapse in your insurance coverage.

Less policy flexibility

Some companies charge an early cancellation fee if you terminate your policy before the term expires. With a six-month policy, you won't have to wait as long until the next renewal date if you want to cancel but also want to avoid this fee.

More frequent premium recalculations

With a year-long policy, your cost usually stays the same for the whole year unless you make changes like adding or removing a vehicle or driver. A six-month policy that renews twice a year could see your premium fluctuate more frequently.

Progressive Auto Insurance: How Much Does It Cost?

You may want to see also

Explore related products

![]()

Six-month policies offer more flexibility

Six-month auto insurance policies offer more flexibility than 12-month policies. This is because they allow for more frequent reviews of your driving activity, which can be beneficial if you are a high-risk driver or have a poor record. If you have a clean record, a six-month policy can also help you secure lower rates more quickly.

With a six-month policy, you will not be locked into your car insurance for as long, giving you more flexibility if you are unhappy with your current provider or want to avoid cancellation fees. You can simply choose not to renew at the end of the six-month term. Six-month policies are also better if you want to pay in full, as you will not have to pay for a full year upfront.

Six-month policies are also beneficial if you want to avoid the risk of twice-yearly premium increases. Insurance companies typically revise rates at the end of the policy period, so the cost of your insurance coverage may decrease more quickly with a six-month policy. If you haven't filed any claims or have any traffic infractions during the policy period, you may get a lower rate when it's time to renew.

However, it is worth noting that six-month policies can also lead to more frequent premium recalculations and fluctuations. This means that your premiums are more likely to change, either increasing or decreasing, depending on your previous coverage period. Additionally, you may be more likely to forget your renewal dates with a six-month policy, as they occur twice a year.

Insurance Scores: Good Auto Rates

You may want to see also

Explore related products

![Life and Health Insurance License Exam Secrets Study Guide - Full-Length Practice Test, Detailed Answer Explanations: [2nd Edition]](https://m.media-amazon.com/images/I/71PdYCnP8ML._AC_UL320_.jpg)

![]()

12-month policies are better for budgeting

While six-month auto insurance policies are more common, some insurance providers do offer 12-month policies. Opting for a 12-month policy has several benefits, especially when it comes to budgeting.

A 12-month auto insurance policy can make budgeting simpler. Your car insurance rate will be locked in for the entire year, so you will know what to expect each month. This predictability can make it easier to manage your finances and ensure you have enough money to cover your expenses.

With a 12-month policy, you will only see rate increases during the year if you make changes to your policy, such as adding another vehicle or driver. This stability can provide peace of mind and help you plan your finances effectively.

Additionally, a 12-month policy may also reduce the risk of forgetting to pay your insurance premiums. With a six-month policy, you have to remember to pay twice a year, which increases the chances of missing a payment. A 12-month policy simplifies this process, reducing the potential for lapses in insurance coverage.

Furthermore, a 12-month policy can also save you money in the long run. Insurance companies typically offer discounts if you pay your premium in full instead of in monthly installments. With a 12-month policy, you have the option to pay annually, taking advantage of this discount and potentially saving money overall.

While a 12-month auto insurance policy has advantages for budgeting, it is important to consider your personal circumstances and preferences when choosing an insurance policy. Both six-month and 12-month policies have their pros and cons, and the best option for you will depend on your specific needs and financial situation.

Root Auto Insurance: Good or Bad?

You may want to see also

Explore related products

![]()

12-month policies are ideal for drivers seeking consistent rates

Auto insurance policies typically come in two durations: six months and 12 months. Six-month policies are more common, as they allow insurance companies to easily recalculate rates, factoring in routine price revisions and changes to your driving profile. However, 12-month policies are ideal for drivers seeking consistent rates.

The primary benefit of a 12-month policy is that your rate is locked in for an entire year. This means that, excluding any changes you make to your policy, you will be immune to rate revisions for at least 12 months. With a six-month policy, your rates are revisited every six months, and your insurance company can raise your premium even if you didn't have an accident or make any changes to your policy.

In addition, a 12-month policy can make budgeting simpler. You will know what to expect from month to month and won't have to worry about monthly payments if you pay your premium annually. However, your rates will change if you add or remove a driver or vehicle from your policy.

Twelve-month policies are less common than six-month policies, so you may need to specifically request one from your provider. They can also be difficult to find, as not all insurance providers offer them. You may need to be in a legacy program to qualify. In addition, if you are unhappy with your insurance provider, you will have to wait longer to change providers with a 12-month policy.

When deciding between a six-month and a 12-month policy, you should consider whether your priority is flexibility or locked-in rates. Six-month policies offer more flexibility, as they are re-evaluated twice a year, whereas 12-month policies are better for drivers who want to avoid the risk of twice-yearly premium increases and lock in their rate for a full year.

Auto Insurance: What You Need to Know

You may want to see also