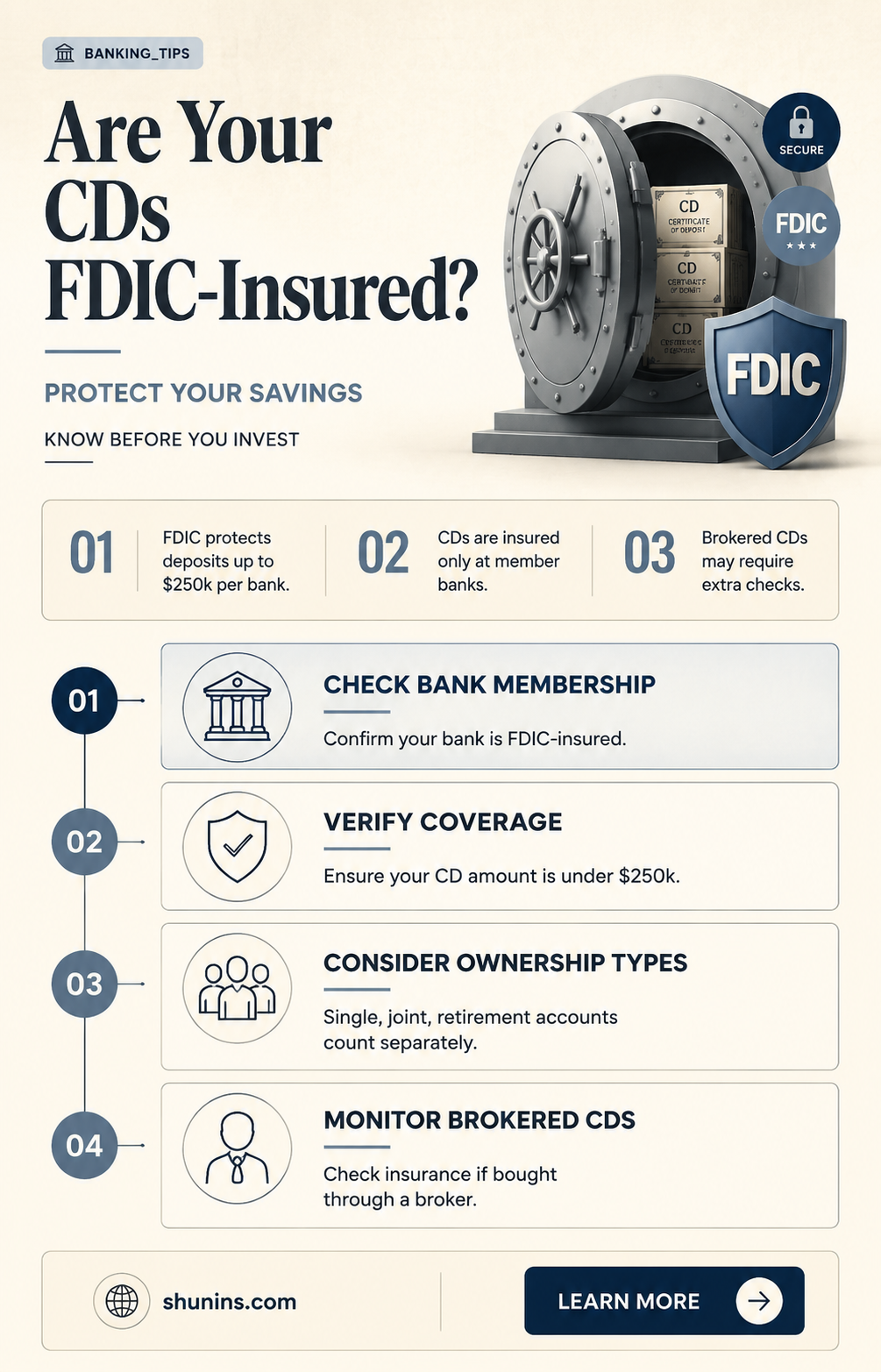

Certificates of Deposit (CDs) are considered a safe option as they are insured by the Federal Deposit Insurance Corporation (FDIC). The FDIC is a United States government-backed agency that provides deposit insurance to protect your money in the event of a bank failure. FDIC insurance covers various deposit products, including CDs, checking and savings accounts, and money market deposit accounts (MMDAs). This insurance is automatic for deposit accounts opened at FDIC-insured banks, protecting up to $250,000 per depositor, per bank, per ownership category. While most CDs are FDIC-insured, there are exceptions, such as investing in foreign banks or purchasing CDs on the secondary market. It is important to understand the specific terms and conditions of your CD account to ensure it is covered by FDIC insurance.

| Characteristics | Values |

|---|---|

| Are all CDs insured by the FDIC? | No, only CDs from FDIC-member banks are insured. |

| What is the coverage limit? | $250,000 per depositor per bank. |

| Are there different types of CDs? | Yes, traditional fixed-rate CDs, high-yield CDs, no-penalty CDs, and bump-up CDs. |

| When is a good time to purchase CDs? | When interest rates are climbing, as you can lock in higher rates. |

| Where can you purchase CDs? | Banks, credit unions, and online banks. |

| How risky are CDs? | CD accounts are a low-risk option with an acceptable balance between return and risk. |

| How do I know if my bank is FDIC-insured? | You can ask a bank representative, look for the FDIC sign at your bank, or use the FDIC's BankFind tool. |

| What happens if my bank fails? | The FDIC steps in to guarantee the insured amount in existing deposit accounts. |

Explore related products

What You'll Learn

- CDs are insured if the bank is FDIC-insured, with coverage up to $250,000

- CD accounts are a low-risk option with a balance between return and risk

- CD accounts usually have higher interest rates than savings accounts

- CD accounts can be purchased at banks, credit unions, and online banks

- CD accounts that are renewed for the same term and amount are separately insured

![]()

CDs are insured if the bank is FDIC-insured, with coverage up to $250,000

The Federal Deposit Insurance Corporation (FDIC) provides insurance for certificates of deposit (CDs) in the event of a bank failure. This insurance is available for CDs from FDIC-insured banks, with coverage of up to $250,000 per depositor per bank.

FDIC deposit insurance is designed to protect bank customers if an FDIC-insured bank fails. This insurance is automatic for deposit accounts opened at FDIC-insured banks and covers various deposit products, including checking and savings accounts, money market deposit accounts (MMDAs), and CDs. It's important to note that not all financial products at a bank are covered by the FDIC, and certain types of CDs may not carry deposit insurance even when held at an FDIC-member bank.

To determine if a bank is FDIC-insured, individuals can ask a bank representative, look for the FDIC sign at the bank, or use the FDIC's BankFind tool. This tool provides detailed information about FDIC-insured institutions, including branch locations, official websites, and current operating status.

While CDs are generally considered safe, it's always a good idea to diversify your investments and understand the specific terms and conditions of any financial product before making a decision. Additionally, it's worth noting that the FDIC provides resources for individuals looking to open a bank account and learn more about deposit insurance coverage.

In summary, CDs are insured by the FDIC if they are from an FDIC-insured bank, with coverage of up to $250,000 per depositor. This insurance provides protection for depositors in the event of bank failure, but it's important to be informed about the specifics of any financial product before investing.

Who Can Be Your Life Insurance Beneficiary?

You may want to see also

Explore related products

![]()

CD accounts are a low-risk option with a balance between return and risk

Certificates of Deposit (CDs) are considered a low-risk option for investing. They are suitable for those who are risk-averse but still want to earn a decent return. CDs are insured by the Federal Deposit Insurance Corporation (FDIC), which is an independent agency of the United States government. The FDIC steps in to guarantee the insured amount in the rare event of a bank failure. Per depositor, up to $250,000 is protected by the FDIC or the National Credit Union Administration (NCUA).

CDs offer a predictable and stable return on your investment, making them a reliable option for saving. They generally have higher interest rates than traditional savings accounts, with short-term options currently offering around 3-5% APY. The longer the term, the higher the interest rate tends to be. However, CDs with longer terms may have lower rates than short-term CDs if interest rates are expected to fall. Therefore, it is important to consider the direction of interest rates before investing in CDs.

CDs are a good option for those who want to save for a specific goal or date in the short to medium term. You can choose the length of the term, which can range from a few months to many years. During this time, you earn a guaranteed interest rate on your deposit before getting back your initial investment plus any interest at the maturity date. This predictable return means that CDs are a safer option than the stock market, where there is a possibility of losing money.

However, CDs may not be suitable for everyone. They may not be the best choice for long-term goals, such as retirement, as the potential for growth is limited compared to market investments. Additionally, CDs typically require a minimum deposit, and there may be penalties for early withdrawal. Therefore, it is important to consider your financial goals and risk tolerance when deciding whether to invest in CDs.

Funeral and Burial Insurance: A Life Insurance Alternative?

You may want to see also

Explore related products

![]()

CD accounts usually have higher interest rates than savings accounts

CDs (certificates of deposit) are a type of savings account that pays a fixed rate for a set length of time. They are considered low-risk investments as they offer a predictable return on investment. On the other hand, savings accounts provide more flexibility to make withdrawals.

CDs generally offer higher interest rates than traditional savings accounts. For example, on May 19, 2025, the average rate for a 12-month CD was 1.75%, more than four times higher than the average savings account rate of 0.42%. The best interest rate a bank could offer on a CD was 5.37%—the national cap rate at the time.

CDs with longer term lengths tend to offer higher interest rates. Term lengths can range from three months to five years, and sometimes up to ten years. Callable CDs, which can be redeemed by the issuing bank before maturity, also tend to offer higher rates than CDs protected against call risk.

However, it's important to note that interest rates on savings accounts can change over time, going up or down according to the Federal Reserve's benchmark interest rate. If rates rise, locking your money into a CD with a lower rate may result in earning less than if you had chosen a savings account.

High-yield savings accounts, which are often offered by online-only banks, can provide competitive interest rates that are much higher than traditional savings accounts. These banks can offer higher rates due to their lower overhead costs compared to brick-and-mortar banks.

Haemochromatosis: Life Insurance Considerations and Impacts

You may want to see also

Explore related products

![]()

CD accounts can be purchased at banks, credit unions, and online banks

Certificates of deposit (CDs) are insured by the Federal Deposit Insurance Corporation (FDIC) if they are purchased from FDIC-member banks. The FDIC is a United States government agency that provides deposit insurance, protecting customers if an FDIC-insured bank fails. This insurance is automatic and free for customers with deposit accounts in FDIC-insured banks, and covers up to $250,000 per depositor, per bank, and per ownership category.

Most CDs are insured by the FDIC, but there are exceptions. CDs that are not insured include those that involve investing money in foreign banks. In addition to lacking FDIC insurance, these CDs carry the risk of exchange rates moving up or down during the CD term.

CDs are considered a safe investment option, offering guaranteed returns over a period of time chosen by the customer, ranging from a few months to several years. CDs generally pay higher interest rates than savings accounts, and money market accounts. However, CDs require more commitment than regular savings accounts, as the money is locked away for a set time period, and withdrawing money before the maturity date may result in an early withdrawal penalty.

Whole Life Insurance: Smart Investment or Waste of Money?

You may want to see also

Explore related products

![]()

CD accounts that are renewed for the same term and amount are separately insured

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance is backed by the full faith and credit of the United States government. FDIC deposit insurance covers certain deposit products, including certificates of deposit (CDs).

It is important to note that not all CDs are FDIC-insured. Only CDs from FDIC-member banks are insured, and this coverage is up to $250,000 per depositor per bank. Additionally, there are some exceptions to FDIC coverage for CDs. For example, if you invest money in foreign banks through a CD account, it may not carry FDIC insurance. Similarly, if you purchase a CD through a non-bank institution, such as a brokerage firm, it may not be insured.

To determine if your CD is FDIC-insured, you can ask a bank representative, look for the FDIC sign at your bank, or use the FDIC's BankFind tool, which provides detailed information about all FDIC-insured institutions.

Group Term Life Insurance: Individual Benefits and Coverage

You may want to see also

Frequently asked questions

No, only CDs from FDIC-insured banks are insured. FDIC insurance covers checking and savings accounts, money market deposit accounts (MMDAs), and certificates of deposit (CDs).

FDIC insurance covers up to \$250,000 per depositor per bank. This limit applies to all single accounts owned by the same person at the same bank.

You can ask a bank representative, look for the FDIC sign at your bank, or use the FDIC's BankFind tool to access detailed information about FDIC-insured institutions.