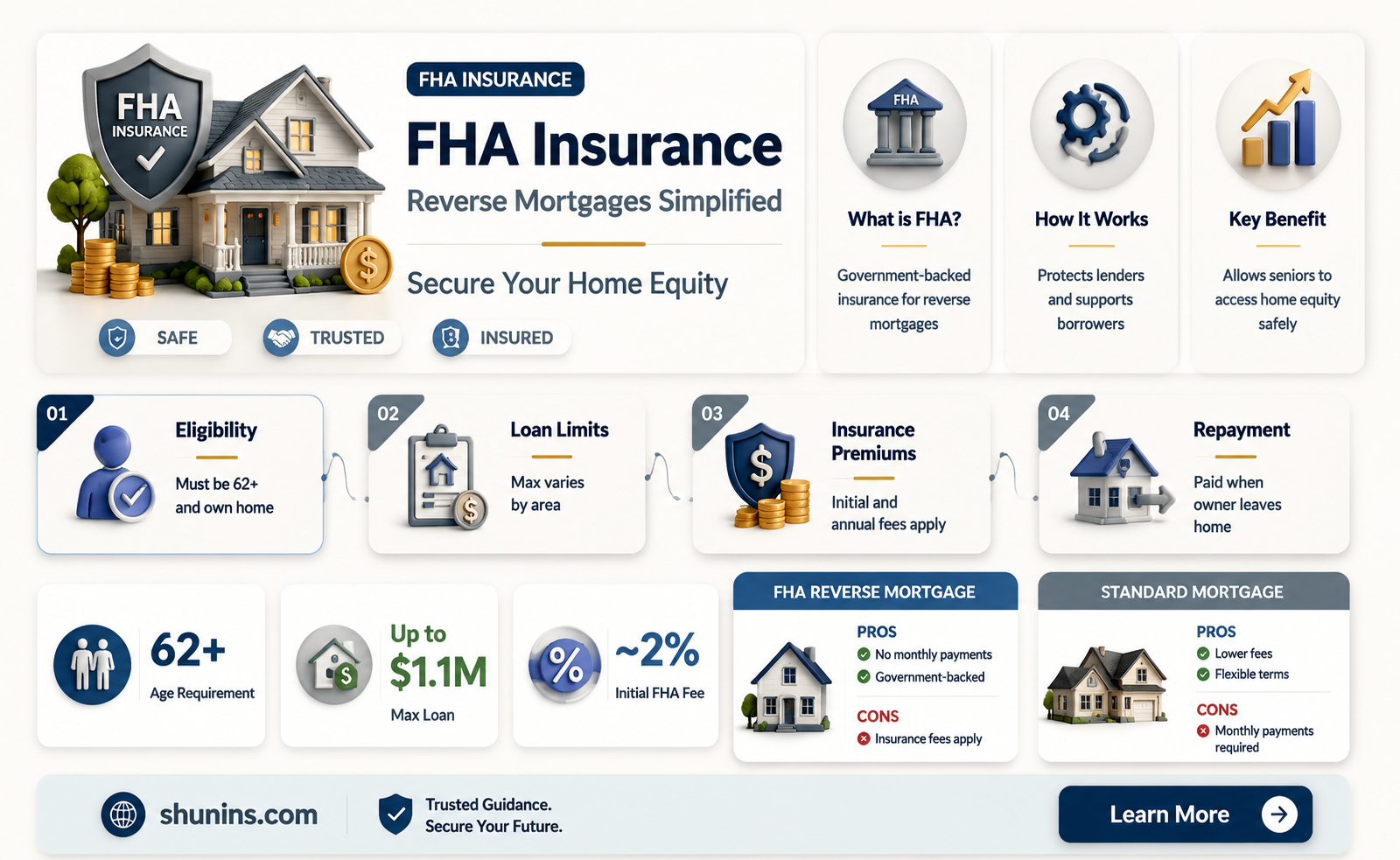

Reverse mortgages are a way for older homeowners to tap into the equity in their homes without having to sell them. The Federal Housing Administration (FHA), part of the US Department of Housing and Urban Development (HUD), provides insurance for a type of reverse mortgage known as a Home Equity Conversion Mortgage (HECM). HECMs are the most common type of reverse mortgage today, but not all reverse mortgages are FHA-insured. There are also proprietary reverse mortgages that are not insured by the federal government, as well as single-purpose reverse mortgages offered by state and local governments.

| Characteristics | Values |

|---|---|

| Type of Loan | Reverse Mortgage |

| Insurer | Federal Housing Administration (FHA) |

| Other Names | Home Equity Conversion Mortgage (HECM) |

| Loan Issuers | FHA-approved lenders, including banks and credit unions |

| Loan Limit | $1,209,750 |

| Requirements | Must be 62 or older and own a home |

| Credit Score Requirement | Minimum FICO score of 580 for low down payment advantage |

| Down Payment | 3.5% |

| Monthly Insurance Premium | 0.50% of the outstanding loan amount |

| Property Types | Single-family homes, condominiums, manufactured homes |

| Number of Units | Up to four units |

| Occupancy | Borrower must occupy the property |

| Payment Options | Monthly payments, line of credit, or a combination of both |

| Non-Recourse Feature | Borrower will not owe more than the home is worth |

Explore related products

What You'll Learn

![]()

FHA reverse mortgage loans

The Federal Housing Administration (FHA), part of the U.S. Department of Housing and Urban Development (HUD), provides insurance for a type of reverse mortgage known as a Home Equity Conversion Mortgage (HECM). HECMs are the most common type of reverse mortgage today. Like other reverse mortgages, they allow homeowners to tap into the equity accumulated in their homes without having to sell the home. Unlike a regular mortgage, the homeowner doesn't have to make payments until they sell the home, move out, or pass away. Instead, the amount owed accumulates over time and is eventually paid off when the home is sold or by the homeowner's heirs if they wish to keep it.

The FHA insures HECMs, but it does not issue them. Instead, they are issued by FHA-approved lenders, including banks and credit unions. HUD has a search tool on its website that borrowers can use to find approved lenders in their area. FHA-insured loans have always been a popular option for first-time homebuyers. There are no income or credit qualifications for this type of loan, and it allows closing costs to be financed into the reverse mortgage. The amount of an FHA reverse mortgage is based on the home's value or the FHA insurance limit, whichever is lower.

The FHA has a maximum loan amount that it will insure, known as the FHA lending limit, which is currently $1,209,750. This limit increases annually for many counties in the United States, giving potential borrowers more options. However, FHA may become less competitive due to loan limits set by the federal government. FHA-insured loans also have specific property type requirements, and homes such as manufactured homes built before 1976 or co-ops may not qualify for an FHA reverse mortgage.

In addition to HECMs, there are also proprietary reverse mortgage loans that are not FHA-insured and single-purpose reverse mortgage loans offered by state and local governments. Proprietary reverse mortgages are not government-insured and can have higher lending limits than FHA loans. Single-purpose reverse mortgages are issued by state and local agencies and some nonprofit organizations for low- and moderate-income homeowners, and the proceeds must be used for a specific purpose, such as home repairs or paying property taxes.

Termite Insurance: Worth the Cost?

You may want to see also

Explore related products

$4.99 $19.95

![]()

FHA insurance requirements

FHA Reverse Mortgage Insurance Requirements

The Federal Housing Administration (FHA) provides insurance for a type of reverse mortgage known as a Home Equity Conversion Mortgage (HECM). HECMs are the most common type of reverse mortgage today. FHA insurance on HECMs protects the lender in case the borrower defaults on the loan. This type of insurance is required for all HECM loans.

FHA Mortgage Insurance Requirements

FHA requires both upfront and annual mortgage insurance for all borrowers, regardless of the amount of the down payment. The upfront mortgage insurance premium is typically 2% of the loan amount. FHA mortgage insurance provides protection for lenders against losses resulting from defaults on home mortgages.

Homeowner's Insurance Requirements for FHA Loans

FHA loans also have specific requirements for homeowner's insurance. The property being purchased must have homeowner's insurance in effect on the day of closing. In addition, certain properties may require additional coverage, such as flood insurance. The insurance policies must remain in effect as long as there is a mortgage on the property, and they are typically paid as part of the monthly mortgage payment. The borrower has the right to choose their insurance carrier, as long as the policy meets FHA requirements.

Credit Score Requirements

While not directly related to insurance requirements, it is important to note that FHA loans have specific credit score requirements. For an FHA loan with a low down payment of 3.5%, borrowers typically need a minimum credit score of 580. If the credit score is below 580, the down payment requirement increases to 10%.

Cigna Accident Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Non-FHA reverse mortgages

Not all reverse mortgages are FHA-insured. Non-FHA reverse mortgages, also known as proprietary reverse mortgages, are distributed through private lenders and other financial institutions. Jumbo reverse mortgages are a type of non-FHA reverse mortgage that offers loan amounts as high as $4 million to $5 million for high-value properties. They are not limited to the current HUD maximum claim amount of $1,209,750.

While non-FHA reverse mortgages may offer higher loan amounts and more flexibility in property types, they do not offer the same level of insurance protection as FHA-insured loans. FHA-insured loans are backed by the Federal Housing Administration, providing peace of mind to borrowers. Non-FHA reverse mortgages may also have different interest rates and loan terms, which can be more or less favourable depending on the borrower's circumstances.

It is important for borrowers to carefully consider their options and compare loan products from multiple lenders before deciding on a reverse mortgage. This includes understanding the fees, interest rates, and repayment terms associated with each loan option. Borrowers should also be aware of the potential risks and implications of taking out a reverse mortgage, such as the accumulation of debt over time if regular payments are not made.

Understanding Residential Insurance Underwriting Reports

You may want to see also

Explore related products

![]()

HUD maximum lending limit

The Federal Housing Administration (FHA), part of the U.S. Department of Housing and Urban Development (HUD), provides insurance for a type of reverse mortgage known as a Home Equity Conversion Mortgage (HECM). The FHA has a maximum loan amount that it will insure, known as the FHA lending limit. The lending limit for 2025 is $1,209,750.

The FHA's lending limit is calculated based on median house prices in each county and these limits increase annually for many counties in the United States. The FHA's nationwide forward mortgage limit "floor" and "ceiling" for a one-unit property in 2025 are $524,225 and $1,209,750, respectively. The limits for multiple-unit properties are fixed multiples of the one-unit limits.

The FHA reverse mortgage allows homeowners to tap the equity accumulated in their homes without selling the home. The homeowner can take the money as a lump sum, a series of monthly payments, or a line of credit. The borrower does not pay on these loans until the house is sold.

The FHA insurance provides essential protection for borrowers. If there is not enough money from the sale of the home to repay the loan in full, FHA insurance is used to pay the difference. One of the standout features of FHA insurance is the "non-recourse" feature, which means that if the loan amount exceeds the value of the home, neither the borrower nor their heirs will be responsible for paying the excess amount.

Medicare Supplemental Insurance: Is It a Smart Investment?

You may want to see also

Explore related products

![]()

FHA-insured HECM loans

The Federal Housing Administration (FHA), part of the U.S. Department of Housing and Urban Development (HUD), provides insurance for a type of reverse mortgage known as a Home Equity Conversion Mortgage (HECM). The insurance protects the lender in case the borrower defaults on the loan. HECMs are the most common type of reverse mortgage today.

HECMs can be either fixed-rate or variable-rate loans. In the case of a fixed-rate loan, the borrower must take the money as a lump sum. A variable-rate HECM can provide income in the form of monthly payments, a line of credit for the homeowner to draw on as they choose, or some combination of the two.

The FHA does not issue HECM loans; instead, they are issued by FHA-approved lenders, including banks and credit unions. The FHA sets guidelines and eligibility for these loans. Borrowers can only obtain HECMs from FHA-approved lenders. To qualify for an HECM, borrowers must meet all the requirements set by the FHA, including having the financial capability to continue to make timely payments of ongoing property charges such as property taxes, insurance, homeowner association fees, etc.

HECM loans include several fees and charges, including mortgage insurance premiums (initial and annual), third-party charges, origination fees, interest, and servicing fees. The initial mortgage insurance premium (MIP) is 2% of the loan amount, and the annual MIP is 0.5% of the outstanding mortgage balance. The mortgage insurance guarantees that borrowers will receive expected loan advances.

HECM loans are designed for those aged 62 and older who own their home outright or have few payments left on the mortgage. The loan is paid back when the homeowner no longer occupies the property. Unlike a traditional mortgage loan, the money borrowed from a reverse mortgage does not need to be repaid monthly. Instead, the borrower must repay the entire loan when the home is sold or when the borrower passes away or moves out of the property.

Justin Thomas' Participation in the Farmers Insurance Open: Will He Compete?

You may want to see also

Frequently asked questions

FHA reverse mortgage, also known as Home Equity Conversion Mortgage (HECM), is a type of loan designed for those aged 62 and above who own their home outright or have few payments left on the mortgage.

The Federal Housing Administration (FHA), part of the U.S. Department of Housing and Urban Development (HUD), provides insurance for HECM loans. The insurance protects the lender in case the borrower defaults on the loan.

No, there are several types of reverse mortgages, including FHA-insured and non-FHA-insured. Non-FHA-insured reverse mortgages include proprietary reverse mortgages and single-purpose reverse mortgages.

FHA-insured reverse mortgages offer essential protections for borrowers. One standout feature is the "non-recourse" clause, which means that neither the borrower nor their heirs will be responsible for paying the excess amount if the loan amount exceeds the home's value.

FHA-insured reverse mortgages are issued by FHA-approved lenders, including banks and credit unions. You can use the search tool on the HUD website to find approved lenders in your area.