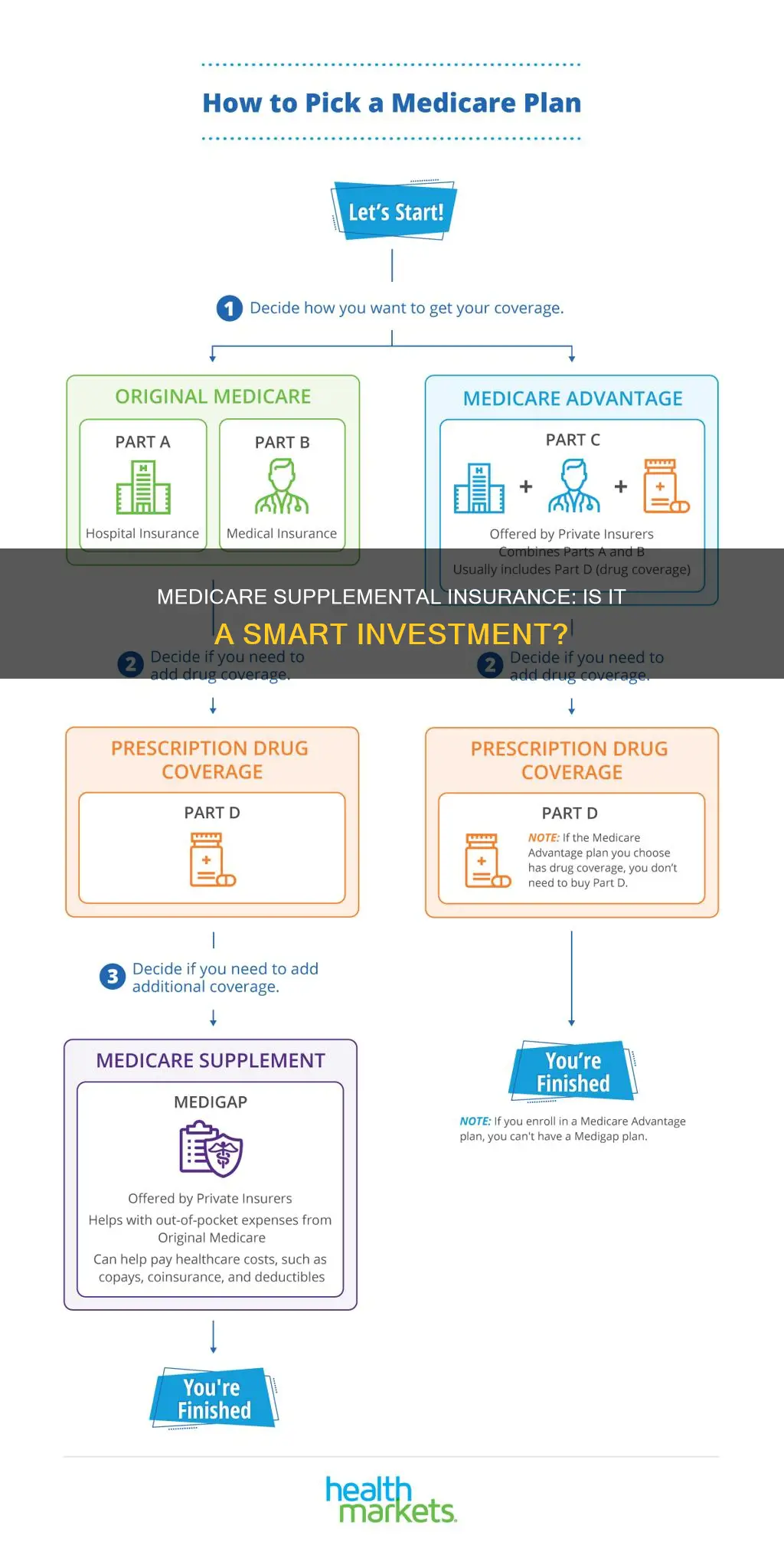

Medicare Supplemental Insurance, also known as Medigap, is an optional insurance policy that can be purchased to cover the gaps in Original Medicare (Parts A and B) coverage. While it is not mandatory, Medigap can provide valuable protection against unexpected and expensive medical costs. The decision to purchase Medicare Supplemental Insurance depends on various factors, including an individual's financial situation, health status, lifestyle goals, and budget. It may be particularly beneficial for those who frequently face leftover bills or high out-of-pocket expenses after their primary insurance coverage. However, it is important to carefully consider the costs and benefits of Medigap plans to determine if they align with one's specific needs and budget constraints.

| Characteristics | Values |

|---|---|

| Purpose | Fills "gaps" in Medicare Part A and Part B |

| Mandatory | No |

| Cost | Premiums vary by plan type, location, age, insurance company, and health status |

| Benefits | Protects against unexpected and/or expensive high deductibles, copays, and/or coinsurance |

| Considerations | Personal financial situation, health, lifestyle goals, doctor choice, and other insurance coverage |

Explore related products

What You'll Learn

![]()

Filling in the gaps in Original Medicare

Medicare Supplement Insurance, also known as Medigap, is an optional add-on that fills the "gaps" in Medicare Part A and Part B. It is an extra insurance policy that can be purchased from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare.

Medicare Part A and Part B do not have maximum out-of-pocket caps, meaning there is no limit on what you could owe as copays and coinsurance add up. Medigap policies put a cap on your yearly costs by covering deductibles, copays, and coinsurance. For example, under Medicare Part B, the government pays for 80% of doctor services, and you pay the other 20%. So, if you had a $100,000 surgery, you would owe $20,000 yourself. A Medigap policy would help cover this large bill.

Medigap policies can be beneficial for many seniors as a way to cover the gaps left by other insurance coverage. However, deciding whether to purchase a Medigap policy depends on your unique financial situation, health, lifestyle goals, and other considerations. If you are pretty healthy and have other coverage that takes care of most of your medical expenses, you might not need Medicare supplemental insurance. Additionally, if the cost of the premiums feels like too much of a stretch for your budget, there are other options to consider.

If you decide that a Medigap policy is right for you, it is important to act quickly. Insurance companies can use medical underwriting to charge you more or deny coverage based on your health or medical history. Therefore, it is best to purchase a Medigap policy during the six-month Medigap open enrollment period that begins when you turn 65 and sign up for Medicare Part B. You can compare Medigap options on Medicare.gov, shop online, or work with an agent or broker to find the best policy for your needs and budget.

MetLife Accident Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Protecting against unexpected costs

Medicare Supplement Insurance, also known as Medigap, is an optional add-on that can fill "gaps" in Medicare Part A and Part B. While it is not mandatory, it can be beneficial in protecting against unexpected and expensive costs.

Medicare Part A and Part B do not have maximum out-of-pocket caps, meaning there is no limit to what you could owe in copays and coinsurance. Medigap policies can help put a cap on these costs, providing peace of mind and financial protection. For example, under Medicare Part B, the government typically pays for 80% of doctor services, while you pay the remaining 20%. In the case of a $100,000 surgery, you would be responsible for $20,000. A Medigap policy could help cover this large bill, as it pays for deductibles, coinsurance, and other out-of-pocket costs.

The cost of Medigap policies varies by plan type, location, age, and insurance company. It is important to consider your budget and run the numbers to see how premiums, deductibles, and copays would impact your finances. While Medigap can provide valuable protection, it may not be necessary if you are generally healthy and have other coverage that takes care of most of your medical expenses. Additionally, Medigap policies only cover medical bills and do not include prescription drugs, dental care, routine eye care, or long-term care.

To make an informed decision, it is recommended to compare options on Medicare.gov or work with an agent or broker to find the best policy for your needs and budget. It is also essential to act promptly, as purchasing a Medigap policy may become more challenging or expensive if done later in life.

Inge Highway: Insurance Safety Report Website

You may want to see also

Explore related products

![]()

Choosing your own doctor

Medicare is the United States federal health insurance program for people aged 65 or older, but it also covers younger people with disabilities or those with End-Stage Renal Disease. While Medicare covers a large share of healthcare costs, it does not cover everything, and patients can be left with significant out-of-pocket expenses. This is where Medicare Supplemental Insurance, or Medigap, comes in. Medigap policies are sold by private companies and help to pay your share of costs in Original Medicare.

Medigap policies are particularly useful if you want to keep your out-of-pocket costs low and maintain freedom when choosing a healthcare provider. If you have Medicare Part A and Part B, you are eligible to apply for a Medigap plan. However, you need to qualify for coverage with the private insurance company. When you first turn 65 and sign up for Part B, you have a six-month Medigap open enrollment period, during which your application must be accepted, regardless of any pre-existing health conditions.

It is important to note that not all doctors accept Medicare, and some may be considered 'opt-out' doctors, meaning Medicare won't pay for any services from these doctors, even if they are Medicare-covered services. You may need to pay upfront for these services or set up a payment plan with the provider. Therefore, it is important to check whether your doctor accepts Medicare. If your doctor participates in Medicare, they accept it for all patients, and your Medigap insurance company is required to pay your doctor directly if you ask them to.

Medigap policies are standardized and automatically renewed each year, provided you pay your premiums. The benefits in each lettered plan are the same, no matter which insurance company sells it. The price is the only difference between policies with the same letter sold by different companies. Medigap policies do not usually cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Medicare Advantage is another way to get your Medicare coverage, but you cannot have both Medicare Advantage and Medigap. Medicare Advantage offers more flexibility and can include extra benefits such as dental, vision, and prescription drugs. However, you must renew your policy each year, and the insurance company can change your benefits or cancel the plan. The co-payments and deductibles may also be higher than with Medigap.

Insurers' Clearing Houses: Why and What For?

You may want to see also

Explore related products

![]()

The peace of mind it offers

Medicare Supplemental Insurance, or Medigap, is an optional add-on that can fill “gaps” in Medicare Part A and Part B. It is an extra insurance policy that you can buy from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare.

Medicare Supplement Insurance may be worth it for the peace of mind it offers. It can be beneficial for many seniors as a way to cover the gaps left by other insurance coverage. It can help protect your finances from high costs, which can destroy your nest egg. It can be seen as a product that brings predictability and peace of mind.

Medicare Part A and Part B don't have maximum out-of-pocket caps. There’s no limit on what you could owe as copays and coinsurance add up. Buying a Medigap policy is one way to put a cap on your yearly costs. Paying more upfront for premiums could pay off by limiting your future out-of-pocket spending.

Additionally, Medicare Supplemental Insurance may be worth it if you value doctor choice. A supplement does not require a referral to see any doctor, so you can choose the doctor you want without worrying about insurance restrictions.

However, it's important to consider your unique financial situation, health, lifestyle goals, and other factors when deciding if Medicare Supplemental Insurance is worth it for you. It may not be necessary if you are pretty healthy and have other coverage that takes care of most of your medical expenses.

Home Insurance: Theft Coverage Explained

You may want to see also

Explore related products

![]()

The potential for reduced costs

Medicare supplemental insurance, or Medigap, is an optional add-on that can fill “gaps” in Medicare Part A and Part B coverage. It is important to note that Medicare Supplement Insurance is not mandatory, and you are not required to sign up for it. However, it can provide significant benefits in reducing potential costs for individuals.

Medicare Part A and Part B do not have maximum out-of-pocket caps, meaning there is no limit to what you could owe in copays and coinsurance. Medigap policies can help address this issue by putting a cap on your yearly costs. By paying more upfront for premiums, you can potentially limit your future out-of-pocket spending. This is especially beneficial if you find yourself with leftover bills or unexpected expenses after your other insurance coverage has been applied.

For example, under Medicare Part B, the government typically pays for 80% of doctor services, leaving you responsible for the remaining 20%. If you had a $100,000 surgery, you would owe $20,000 out of pocket. With a Medigap policy, you can help cover these large bills and protect yourself from unexpected financial burdens. Additionally, Medigap plans can provide peace of mind by ensuring that if Medicare covers a service, your supplements will also cover it, reducing the likelihood of medical cost surprises.

While the benefits of Medigap plans are standardized, the premiums can vary by insurance company, plan type, location, age, and health status. Therefore, it is essential to compare different options and run the numbers to see how the premiums, deductibles, and copays would impact your budget. Ultimately, the decision to purchase Medicare supplemental insurance should be based on your unique financial situation, health, lifestyle goals, and other considerations.

Insurance Due Date: Homeowner's Guide

You may want to see also

Frequently asked questions

Medicare Supplemental Insurance, also known as Medigap, is an optional add-on that can fill “gaps” in Medicare Part A and Part B.

Deciding whether Medicare Supplemental Insurance is worth it depends on its benefits and costs as they relate to your personal situation. It may be worth it if you value doctor choice or if you want to avoid unexpected expenses.

Medicare Supplemental Insurance is sold by private health insurance companies. You can compare options on Medicare.gov, shop online, or work with an agent or broker to find the best policy for you.