Comprehensive insurance is an optional form of vehicle insurance that covers damage to your car outside of a collision. This includes theft, vandalism, fire, and weather-related issues. When purchasing comprehensive insurance, you must select a deductible amount, which is the sum you pay when filing a claim. The insurance company will then pay up to the policy limit, which is usually the car's current market value minus the deductible. While comprehensive insurance is typically more affordable than collision coverage, it may not be worth it for older, low-value vehicles with high deductibles. In such cases, the insurance payout may not justify the cost of coverage. Therefore, it is essential to consider factors such as the age and value of your vehicle, the frequency of extreme weather and car theft in your area, and your financial ability to pay for repairs or a replacement vehicle when deciding whether comprehensive insurance is worth it for your specific situation.

| Characteristics | Values |

|---|---|

| Cost | The cost of comprehensive insurance depends on the value of the car, its replacement parts, and the deductible amount. |

| Deductible | The deductible is the amount paid out of pocket before insurance coverage kicks in. Higher deductibles can lower premiums but increase financial risk in the event of a claim. |

| Vehicle Value | Comprehensive insurance is less valuable for older, depreciated vehicles as payouts are based on the car's current value, not the original purchase price. |

| Vehicle Financing | Comprehensive insurance is often required when financing or leasing a vehicle. |

| Extreme Weather Events | Comprehensive insurance covers damage from extreme weather, including floods, hail, and falling objects. |

| Car Theft | Comprehensive insurance covers car theft and reimburses the owner for the car's value, minus the deductible. |

| Vandalism | Comprehensive insurance covers vandalism and other non-collision damage. |

| Collision Coverage | Collision insurance is often packaged with comprehensive insurance and covers accident-related repairs. |

| Liability Coverage | Liability insurance covers damage to others' property and injuries caused by the insured driver. |

| Location and Usage | Comprehensive insurance may be more valuable in areas with a high frequency of extreme weather, theft, and vandalism. |

| Savings and Alternatives | The availability of savings to cover replacement vehicle costs after a crash may impact the decision to opt for comprehensive insurance. |

Explore related products

What You'll Learn

![]()

Comprehensive insurance for older cars

When it comes to comprehensive insurance for older cars, there are a few key factors to consider. Firstly, let's understand what comprehensive insurance entails. Comprehensive insurance covers a range of issues outside your control, such as natural disasters, collisions with animals, fire, theft, and vandalism. It is important to note that comprehensive insurance does not cover damage to your vehicle in the event of a car accident; instead, it protects your car when it is not in motion.

Now, for older cars, the decision to maintain or drop comprehensive insurance depends on several variables. Firstly, you should consider the value of your vehicle. If your car is worth a few thousand dollars, dropping comprehensive coverage might be a good idea. For example, if your car is worth $3000 and you have comfortable financial stability, you might not need comprehensive insurance. However, if your car is worth $5000, you might be in a grey area, and it could be beneficial to hold onto comprehensive coverage for a little longer.

The age and mileage of your vehicle are also important factors. Generally, as cars get older, their value decreases, and it becomes less financially viable to maintain comprehensive coverage. For instance, the cost of insuring a 15-year-old car after an accident can represent a significant percentage of the car's value. Additionally, older cars are cheaper to insure, and the potential insurance payouts after an accident are lower due to the decreased value of the vehicle. Therefore, it might be more cost-effective to save the money from insurance premiums and prepare to repair or replace your car out of pocket if necessary.

Another aspect to consider is the frequency of extreme weather events, car theft, and vandalism in your area. If these incidents are common, comprehensive insurance might be a worthwhile investment for added protection. On the other hand, if these events are rare, you might opt to save on insurance premiums. Additionally, you can choose a higher deductible to reduce the cost of your comprehensive coverage premium, but ensure you can afford the deductible amount in case of a claim.

Lastly, if you still owe money on your older car to a lender, you may be required to maintain full coverage until the loan is paid off. Lenders and lease companies often require comprehensive coverage to protect their interest in the vehicle. However, if your vehicle is paid off, you have the option to drop comprehensive coverage and pay for any damages out of pocket.

Home Insurance: Why So Expensive?

You may want to see also

Explore related products

![]()

Comprehensive insurance and car value

Comprehensive insurance is generally required if you have a car loan or lease, and it's likely that your lender will require it. It pays for damage to your vehicle from non-collision events, such as storms, vandalism, or even hitting a deer. It's also worth considering if you'd have a hard time coming up with the cash to repair or replace your car if something unexpected happens.

The value of your car is a key factor in deciding whether to take out comprehensive insurance. If your car is worth a significant amount, comprehensive insurance is often the best choice. This is especially true if you're still making loan repayments on the car. If your car is older and less valuable, comprehensive insurance becomes less useful. That's because it reimburses you for repairs only up to the actual cash value of your car, minus your deductible, and that value declines as your car ages.

If your car holds minimal value, comprehensive coverage may not be worth carrying. You can subtract your deductible from the value of your car, and if the result is a negative number, it makes financial sense to drop your comprehensive policy. However, if the result is a large positive number, keep the comprehensive coverage. If the result is a low positive number, you can decide whether to maintain this type of policy or save the money and prepare to replace or repair your car out of pocket.

If you decide to drop comprehensive coverage, you can consider third-party property insurance or third-party fire and theft insurance. Third-party property covers any damage you cause to someone else's car or property, but not your own car. Third-party fire and theft add a couple of token protections for your car, namely against fire and theft.

Reporting Glass Damage: When to Involve Your Insurance

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

![]()

Comprehensive insurance and deductibles

Comprehensive insurance is typically part of "full coverage insurance", which includes collision insurance and liability insurance. When you buy a comprehensive policy, you must choose a deductible amount, which is the money you pay out of pocket when filing a claim. Most insurers offer deductibles ranging from $500 to $1500, and you can reduce the cost of your premium by choosing a higher deductible. However, this also means that you will have to pay more when you file a claim.

Comprehensive insurance covers various scenarios, including car theft, vandalism, fire, and weather-related issues. It is especially useful if you live in an area with a high frequency of extreme weather, car theft, and vandalism. It also covers damage caused by collisions with animals, falling objects, explosions, floods, lightning, or hail.

The decision to opt for comprehensive insurance depends on several factors. Firstly, consider the value of your car. If your car is not worth much, comprehensive insurance may not be necessary, as the payout will likely be low and may not be worth the insurance cost. In such cases, it may be more cost-effective to pay for repairs or replacements out of pocket. Additionally, consider the age and mileage of your vehicle. Comprehensive insurance becomes less useful as your car gets older and depreciates in value.

To decide if comprehensive insurance is worth it, you can perform a simple calculation. Subtract the deductible amount from the value of your car. Then, subtract the six-month comprehensive coverage premium amount from this value. If the result is a negative number, it makes financial sense to drop the comprehensive policy. If the result is a large positive number, keeping the comprehensive coverage is advisable. For a low positive number, you can choose to maintain the policy or save the money and prepare to pay for repairs or replacements yourself if needed.

Report Your Non-Smoking Status to Insurance: Save Money

You may want to see also

Explore related products

![]()

Comprehensive insurance and extreme weather

Extreme weather events, such as hurricanes, floods, and wildfires, can cause billions of dollars' worth of damage to property, including cars. Comprehensive insurance coverage is a way to financially protect your car from weather-related damage. This type of insurance covers vehicle damage caused by various weather-related events, such as hail, floods, wildfires, and tornadoes. It is particularly useful if you live in an area prone to severe weather or if you regularly park your car outdoors.

Comprehensive insurance is optional if you own your vehicle outright. However, if you finance or lease it, your lender will likely require it. It is also worth considering if you cannot afford to repair or replace your car if it is damaged or stolen. This type of insurance will pay for damage to your car from causes other than collisions, such as hail, flooding, fire, theft, vandalism, and natural disasters.

The cost of comprehensive insurance varies, but it typically involves selecting a deductible amount, which you pay when filing a claim. The insurance company will then send you a check for the approved claim amount minus the deductible. If the damage to your vehicle is close to or more than its value, the insurer will declare it a total loss. You can then choose to accept the payout minus the deductible or repair the car yourself, in which case it will be considered a salvage vehicle and may be ineligible for further coverage.

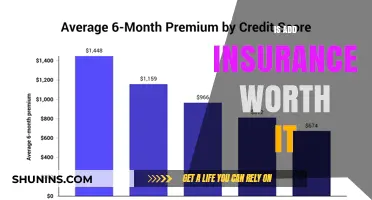

To determine if comprehensive insurance is worth it for you, compare the value of your car to your comprehensive deductible plus the amount you pay for coverage. If there is not a significant difference, you may be paying for coverage you do not need. Additionally, check your monthly bill or policy declaration page to find the six-month premium cost of your comprehensive policy. Subtract the deductible amount from the value of your car, and then subtract your six-month comprehensive coverage premium amount from this value. If you get a negative number, it may be best to drop the comprehensive policy.

In addition to comprehensive insurance for your vehicle, you may also consider purchasing travel insurance to protect yourself financially if extreme weather disrupts your trip. Travel insurance can reimburse you for a percentage of your expenses if your trip is delayed, cancelled, or interrupted due to unforeseen circumstances, such as extreme weather events.

Report Insurance Fraud: Know Your Rights

You may want to see also

Explore related products

![]()

Comprehensive insurance and car theft

Comprehensive insurance is optional, and it's up to the owner whether they want to insure their car comprehensively or not. It is not required by law in any state, but it's usually required by lenders if you are leasing or financing your vehicle. If you own your vehicle outright, you can decide whether comprehensive coverage is worthwhile. Comprehensive insurance is also known as "other than collision" coverage as it covers non-collision-related damage to your vehicle. This includes theft, vandalism, glass and windshield damage, fire, accidents with animals, weather, or other acts of nature.

If your car is stolen and not recovered, comprehensive insurance may pay you the actual cash value (ACV) of the car minus your deductible. If your car is recovered, comprehensive insurance may cover any resulting damages like broken windows and other vandalism that occurred during the theft. However, it is important to note that comprehensive insurance does not cover personal items stolen from your car. It only covers the permanent and pre-installed parts of the car.

The value of comprehensive insurance in the event of car theft depends on your unique circumstances and comfort level. If your vehicle has a high cash value or you cannot afford to repair or replace it out of pocket, comprehensive coverage is a smart move. It can provide peace of mind in case your vehicle gets stolen. On the other hand, if your vehicle's cash value is relatively low and you have a higher deductible, comprehensive coverage may not be worth the additional cost.

If you decide against comprehensive insurance, you can consider third-party property or third-party fire and theft insurance. Third-party property is the most basic level of car insurance, covering damages to someone else's car or property. Third-party fire and theft add coverage for fire damage and theft to the basic third-party property insurance.

Farmers Insurance's Political Leanings: Unraveling the Ties with the Republican Party

You may want to see also

Frequently asked questions

Comprehensive insurance covers damage to your car outside of an accident, including theft, vandalism, and damage from natural disasters. It is usually purchased alongside collision insurance, which covers damage to your car in the event of a crash.

Comprehensive insurance is worth it when the value of your car is significantly higher than the sum of your insurance deductible and the amount you pay for coverage. If your car is leased or financed, comprehensive insurance is likely required. It is also worth considering if you live in an area with a high frequency of extreme weather, car theft, or vandalism.

Comprehensive insurance may not be worth it if your car is paid off and has a low market value. As your car gets older and depreciates, comprehensive insurance becomes less useful as the payout will likely be very low relative to the cost of insurance. If your vehicle is already covered by another policy, you may also want to avoid paying for comprehensive insurance twice.