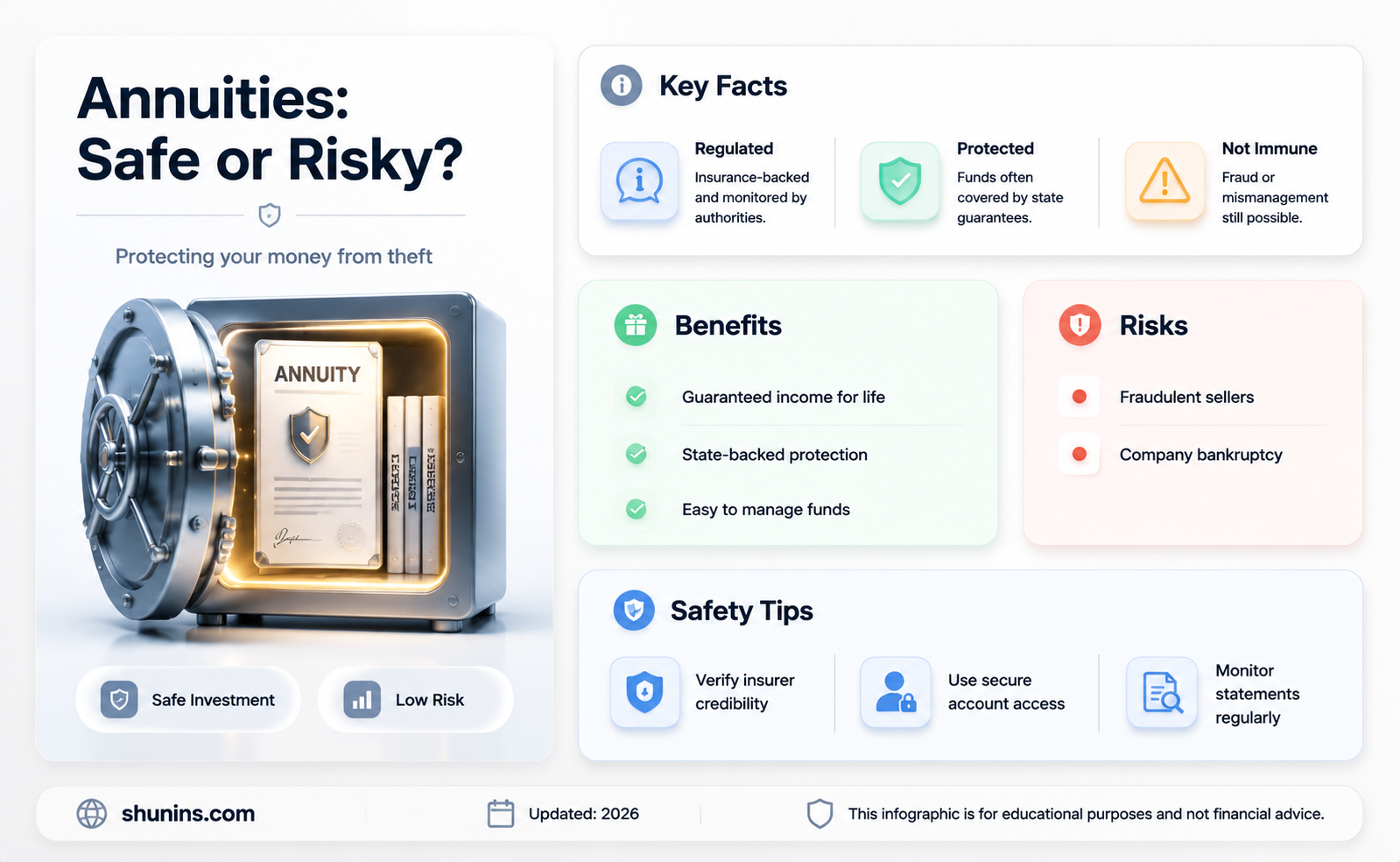

Annuities are a form of insurance that provides a guaranteed income stream, making them popular among retirees. They are not insured by the Federal Deposit Insurance Corporation (FDIC) or backed by a federal agency. Instead, annuities are issued by insurance companies and rely on their financial strength and creditworthiness. State guaranty associations offer protection, typically up to $250,000, in the event of insurer insolvency, with varying coverage limits across states. While annuities are not insured against theft specifically, these state-level protections help safeguard investments in annuities.

| Characteristics | Values |

|---|---|

| Are annuities insured against theft? | No, annuities are not insured against theft. |

| Are annuities insured by the FDIC? | No, annuities are not insured by the Federal Deposit Insurance Corporation (FDIC). |

| Are annuities insured by SIPC? | No, SIPC insurance does not protect investors against the loss in value of a given investment. |

| Are annuities insured by a federal agency? | No, annuities are not backed by a federal agency. |

| Are annuities insured by state guaranty associations? | Yes, annuities are insured by state guaranty associations, which offer protection of up to $250,000 in most states. |

| Are annuities insured by the insurance company issuing them? | Yes, annuities are insured by the financial strength and creditworthiness of the issuing insurance company. |

| Are annuities protected against creditors? | Yes, annuities provide protection against creditors, although this may vary by state. For example, in Florida and Texas, annuities are exempt from seizure by creditors. |

Explore related products

What You'll Learn

![]()

Annuities are not FDIC-insured

Annuities are not insured by the Federal Deposit Insurance Corporation (FDIC). Annuities are insurance products, not banking products, and only the latter are protected by the FDIC.

Annuities are insurance contracts that offer a guaranteed stream of income in exchange for a lump sum or a series of payments. They are popular among retirees seeking a stable and predictable income. While annuities are generally considered low-risk, they are not without their drawbacks and fees associated with them can eat into overall returns.

Despite not being FDIC-insured, annuities are protected through several layers of security. Each state in the US has an insurance guaranty association that provides protection for annuity owners if an insurance company fails. These guaranty associations work similarly to FDIC insurance but are state-based rather than federal. The coverage limits vary by state, but all 50 states offer protection of at least $100,000 per customer, per company, with some states offering up to $500,000 in coverage.

In addition to state guaranty associations, annuities are also protected by the financial strength of the insurance company issuing them. These companies maintain substantial reserves that are strictly regulated and regularly audited to ensure they can meet their obligations.

While annuities are not FDIC-insured, the alternative protection mechanisms in place offer comparable or even superior security for investors.

Hepatitis B: A Life Insurance Deal-Breaker?

You may want to see also

Explore related products

![]()

State guaranty associations offer protection

Annuities are not insured against theft. However, annuity customers are protected by nonprofit insurance guaranty associations at the state level. These state guaranty associations act as a safety net to protect policyholders if the insurance company that issued an annuity or insurance policy cannot meet its financial obligations.

State guaranty associations are typically governed by the state's insurance commissioner and an appointed board of directors. In the event that an insurance company becomes insolvent and cannot pay its obligations, the state guaranty association levies an assessment against all the other companies selling the same type of annuity or insurance product. The money from this levy, along with the failed company's remaining assets, is used to pay customer claims against the insolvent insurer up to a limit set by each state's law. These limits vary by state, with a typical statutory limit of $250,000 of an annuity contract. Annuities in Washington D.C. have $300,000 of protection, while those in Puerto Rico get $100,000 in coverage.

State guaranty associations may also voluntarily join the National Organization of Life and Health Insurance Guaranty Associations (NOLHGA). NOLHGA raises funds from its members to pay claims to policyholders if an insolvent insurer does business in multiple states and cannot pay the claims. While state guaranty associations offer some protection, it is important to note that they should not be a substitute for purchasing an annuity from a well-managed and financially stable company. Payments to policyholders are not automatic and depend on court and state legislature approval, which can result in delays.

Understanding Stock Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Variable annuities and market risk

Variable annuities are a type of investment income that rises or falls periodically based on the performance of an underlying portfolio of investments. These underlying investments are called sub-accounts and may include stocks, bonds, or money market accounts. Variable annuities are created by a contract between an investor and an insurance company, where the investor makes a lump sum or series of payments over time. The amount of each payment varies based on the performance of the underlying portfolio.

Variable annuities offer the possibility of higher returns than fixed annuities but also come with market risk, meaning the account value can fall. This market risk is inherent in the product and is due to the variable annuity's market exposure. If financial markets deteriorate, policy balances can decline, and guarantees may kick in across the board. This risk is systematic rather than idiosyncratic and cannot be mitigated by issuing a large number of policies.

Due to the complexity and confusion surrounding variable annuities, they are a leading source of investor complaints. FINRA Rule 2330 establishes sales practice standards and requires that customers be informed of the various features of variable annuities, including market risk, before purchase. Variable annuities may be more suitable for younger investors with longer time horizons and higher risk tolerance.

To manage the systematic risk of variable annuity guarantees, insurers may enter into derivative contracts that transfer risk to other counterparties, typically large banks with more capital. Insurers are also required to set aside funds called reserves to back future payouts on all their issued policies, including variable annuity guarantees. However, if these reserve additions exceed available funds, insurers may experience financial distress and even become insolvent.

Insurance Settlement: Are Proceeds Taxable?

You may want to see also

![]()

Annuities as a safe and secure retirement option

Annuities are an increasingly popular option for retirement planning. They are a form of insurance contract that guarantees a steady income stream, protecting against the risk of outliving one's assets. With annuities, individuals can build a personal pension, ensuring they have enough to cover essential living expenses. This is especially attractive to retirees who prioritise stability and protecting their capital.

There are several types of annuities, each offering different features and benefits to suit various financial needs and preferences. Fixed annuities, for instance, provide a guaranteed rate of return, reducing investment risk compared to more volatile options. This guarantees income for as long as the retiree lives, offering peace of mind and financial security. On the other hand, variable annuities offer the potential for higher returns by tying payments to the performance of investment sub-accounts, but they also carry market risk and may not be suitable for all investors. Indexed annuities, such as those tied to the S&P 500, offer a middle ground with modest growth and some protection against market losses.

Annuities also provide tax advantages. Funds within a deferred annuity grow tax-deferred, meaning taxes are only paid upon withdrawal. Additionally, certain annuities, like fixed-index annuities, offer tax deferral benefits, allowing your money to grow tax-free.

While annuities do not have FDIC insurance, they are protected by state-level regulations and guaranty organisations. Each state has a nonprofit guaranty organisation that insurance companies must join, safeguarding your investment even if the issuing insurer goes out of business. Coverage limits vary, but all 50 states protect at least $250,000 per customer, per company, providing an extra layer of security for retirees.

Overall, annuities are a safe and secure retirement option, offering a guaranteed income stream, financial stability, and protection from market fluctuations. They can be a valuable tool for individuals seeking to grow their wealth in retirement and ensure a comfortable, worry-free future.

How to Get Your Life Insurance License

You may want to see also

![]()

Understanding fees, charges and penalties

Annuities are insurance contracts designed to provide a guaranteed stream of income, making them a popular choice for retirees. While annuities are insured against the issuing insurer going out of business, they are not insured against loss in value of a given investment.

Fees and Charges

- Administrative fees: These are fees you pay for someone to manage your annuity. This fee is generally about 0.3% of the value of your annuity contract, which for a $100,000 annuity would be $300.

- Mortality expenses: These fees compensate the insurance company for the risk it takes by agreeing to a contract with you. The fee can range from 0.5% to 1.5% of the policy value each year. For a $100,000 annuity with a 1% mortality fee, you would pay an additional $1,000.

- Rider fees: Riders are additional options that can be added to your annuity contract, such as a guaranteed minimum income benefit. These typically come with their own fees.

- Rate spreads: These are subtracted from earnings on interest-earning annuities.

- Investment fees: Variable annuities may have fees associated with the underlying investments.

- Commission: Financial professionals are typically paid a commission when they sell you an annuity contract. This commission is usually built into the price of the annuity contract.

Penalties

- Surrender charges: If you withdraw money from your annuity early, you may be charged a surrender fee. These fees can be steep and are intended to discourage early withdrawals.

- Market value adjustment provision: If you incur a surrender charge, you may also be charged a market value adjustment provision.

- Early withdrawal penalty: Withdrawing funds before age 59½ may result in a 10% IRS penalty, in addition to ordinary income taxes.

- Penalty-free withdrawal limits: Some annuities allow for a small percentage of funds to be withdrawn without penalty each year.

- Hardship withdrawals: Some annuities may waive early withdrawal penalties in certain instances, such as disability, terminal illness, or confinement to a healthcare facility.

It is important to carefully review the annuity contract and understand all the associated fees, charges, and penalties before purchasing an annuity.

Child Support and Life Insurance: Can They Place a Lien?

You may want to see also

Frequently asked questions

Annuities are not insured against theft. Annuities are a form of insurance themselves, issued by insurance companies. While annuities are not backed by a federal agency, they are protected by state guaranty associations, which offer protection of up to $250,000.

If an insurance company fails, state guaranty associations offer protection to safeguard your investment. Each state has a guaranty organization that insurance companies must join. If a member company fails, the other companies in the guaranty association help pay the outstanding claims.

Yes, there are different types of annuities with varying levels of protection. Fixed annuities provide a guaranteed rate of return over a specific period, while variable annuities are tied to the performance of investments and carry market risk. Variable annuities purchased through private brokerage firms are protected by the Securities Investor Protection Corporation.