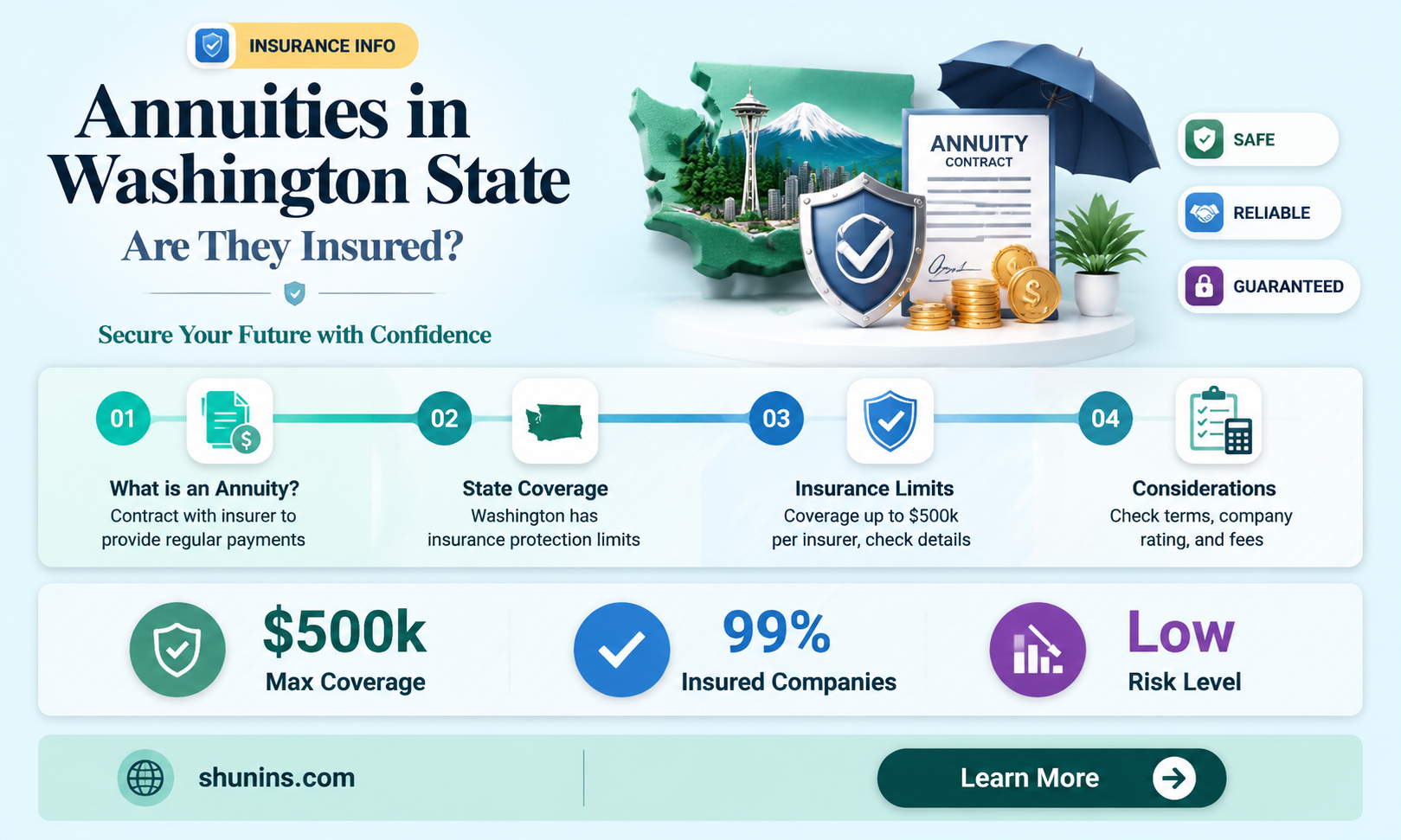

Annuities are a type of insurance product that offers a guaranteed income stream. They are a contract between an individual and an insurance company, where the individual pays a large, single premium or makes payments over time in exchange for future income. While annuities do not have federal government insurance, guaranty associations in all 50 states, including Washington, cover at least $250,000 in annuity benefits for customers in the event that the insurance company becomes insolvent.

| Characteristics | Values |

|---|---|

| Definition | Annuities are a contract between you and an insurance company that offers a way to reduce taxes and/or ensure a steady flow of income. |

| Type of Insurance Product | Annuities are a type of insurance product that pays you income. |

| Use | Some people use annuities as part of a retirement strategy. |

| Purchase | When you buy an annuity, you either pay a large, single premium or make payments over time in exchange for future income. |

| Tax | Annuities grow on a tax-deferred basis until you withdraw money or begin receiving payments. Withdrawals from annuities are normally taxed as ordinary income. |

| Death Benefit | The basic death benefit guarantees that the insurer will, at a minimum, pay out the amount you paid in when you die. |

| Annual Costs | Annuities have costs that you need to pay each year. |

| Early Cancellation Fee | If you cancel or cash out your annuity early, you'll need to pay a fee. |

| Riders | Riders are additions to your annuity that provide more benefits at an additional cost. |

| Payout Options | There are multiple payout options that may be available to you based on your contract. |

| Equity-Indexed Annuity | With an equity-indexed annuity, the insurer offers a guaranteed minimum return, plus a variable rate based on the return of a specific market index. |

| Washington State Guaranty | The Washington Life & Disability Insurance Guaranty Association was created by the Washington legislature in 1971 to protect state residents who are policyholders and beneficiaries of policies (including annuities) issued by an insolvent insurance company, up to specified limits. |

Explore related products

What You'll Learn

![]()

Annuities are a contract between you and an insurance company

An annuity is a contract between an individual and an insurance company. The individual pays either a lump sum or makes regular payments over a period. In return, the insurance company agrees to make regular payments to the individual, either immediately or in the future. Annuities are typically used as a retirement strategy to ensure a steady flow of income. They can be fixed, variable, or indexed to an equity index.

Annuities are a type of insurance product, and as such, they come with certain costs and tax considerations. Individuals should be aware of any fees they will need to pay, as well as the potential tax implications of withdrawals. For example, withdrawals from annuities are normally taxed as ordinary income, and there may be a penalty for early withdrawal.

The basic death benefit of an annuity guarantees that when the annuitant dies, the insurer will pay out at least the amount the annuitant paid in. The annuity contract may also designate a beneficiary who will receive this death benefit. It is important to note that annuities can be complex, and the associated fees can be high. Individuals should carefully consider the pros and cons before entering into an annuity contract.

When purchasing an annuity, individuals have the option to choose how they want to receive their income. They can request regular, fixed payments or opt for a lump-sum payment. A popular payout option is a "lifetime income with 10 years certain," which guarantees monthly income for the life of the annuity owner or for 10 years, whichever is longer.

In summary, annuities are a contract between an individual and an insurance company that offers a steady income stream, typically for retirement. They can provide financial security and peace of mind but also come with certain costs and complexities that should be carefully considered before entering into a contract.

Get a Life Insurance License in Washington: What You Need to Know

You may want to see also

Explore related products

![]()

Annuities offer a guaranteed income stream

Annuities are a type of insurance product that offers a guaranteed income stream. They are a contract between an individual and an insurance company, where the individual pays either a large single premium or makes regular payments over a period of time in exchange for future income. This future income can be in the form of regular payments or a lump sum. Annuities are typically used as part of a retirement strategy, providing a guaranteed stream of income during an individual's retirement years. This can be particularly useful for addressing the risk of outliving one's savings.

There are different types of annuities, including immediate and deferred annuities. Immediate annuities allow individuals to turn a lump sum of money into a guaranteed stream of income right away. Within this category are lifetime annuities, which provide income for the rest of the individual's life, and short-term annuities, which provide income for a specified period. Deferred annuities, on the other hand, allow individuals to make a lump-sum payment or a series of payments, with the money growing until they are ready to start receiving income. Fixed deferred annuities offer growth at a guaranteed interest rate, while variable deferred annuities invest payments into mutual funds, offering more growth potential but also market risks.

Annuities can also be categorized as fixed, variable, or indexed. Fixed annuities provide a fixed income stream, typically for a predetermined period, and are not impacted by economic conditions or market performance. Variable annuities, on the other hand, offer the opportunity for higher returns but are subject to market risks, including the potential loss of principal. Indexed annuities, such as equity-indexed annuities, offer a guaranteed minimum return plus a variable rate based on the performance of a specific market index.

When considering an annuity, it is important to understand the fees and costs associated with the product. There may be annual costs, as well as fees for early cancellation or cash-out. Additionally, withdrawals from annuities are typically taxed as ordinary income. It is recommended to consult with a tax advisor or financial planner to determine if an annuity is suitable for one's financial needs and goals.

Maximizing Life Insurance Benefits: Understanding Spouse Coverage

You may want to see also

Explore related products

![]()

Annuities are not federally insured

While annuities lack federal insurance, they are protected by state guaranty associations and the insurance company's safeguards. These state guaranty associations are nonprofit organizations that provide additional protection if an insurer fails. The typical coverage limit offered by these associations is around $250,000, although it can vary depending on the state. For example, New York provides up to $500,000 in coverage, while California offers $250,000 in protection, and most other states provide a minimum of $100,000.

It is important to note that insurance companies are primarily regulated at the state level, and protection for policyholders is managed by state authorities. These state guaranty associations are not insurance companies themselves but function as cooperatives. The insurance companies must be members of their state's guaranty association if they sell annuities in that state. The associations work to protect policyholders in the rare event of an insurance company's failure.

Before purchasing an annuity, it is recommended to evaluate the insurer's stability thoroughly. This can be done through independent rating agencies, financial reports from the company, and online research. Working with qualified financial professionals can also help individuals make informed decisions about their retirement investments and understand the specific protections available. While annuities are not federally insured, the alternative protection mechanisms in place aim to provide security for investors.

Globe Life Insurance and Colonial Penn: What's the Difference?

You may want to see also

Explore related products

![]()

Annuity benefits are covered by guaranty associations

Annuities are a type of insurance product that pays you an income. They are typically bought by people who want to set aside a significant amount of money for retirement. When you buy an annuity, you either pay a large, single premium or make payments for a fixed period. In return, you get a future income, which can be withdrawn as regular, fixed payments or taken as a lump sum. Annuities can also help reduce taxes as you are not taxed on any interest, dividends, or capital gains that accumulate inside your annuity contract until you make a withdrawal.

State guaranty associations are funded by assessments of their members, with solvent insurance carriers contributing to the funds when a member insurer becomes insolvent. The amount each member pays in assessments is based on the share of premiums they held in the previous three years. Each state defines its own limits on the maximum amount of coverage provided by guaranty associations, with every state guaranteeing a minimum of $250,000 of an annuity contract in the event of an insurer's insolvency.

It is important to note that guaranty associations also have regulatory responsibilities, including monitoring their member insurers to ensure they are complying with industry standards and working with state insurance departments to investigate consumer complaints. To ensure you receive all your annuity benefits, it is recommended to investigate the annuity company's ratings and understand the fees associated with your annuity before purchasing.

Life Insurance Payout: Impact on Scholarship Money

You may want to see also

Explore related products

$14.87 $19.99

![]()

Annuities are a retirement strategy

Annuities are a type of insurance product that pays you an income. They are a contract between you and an insurance company, offering a way to reduce taxes and/or ensure a steady flow of income. People typically buy annuities with retirement in mind, as they can pay out in lump-sum amounts or provide a guaranteed income for as long as they live.

Annuities can be a good retirement strategy for those who want a guaranteed income stream in retirement. They can simplify financial management, reducing the need for complex budgeting or investment decisions. They can also provide a level of longevity protection, ensuring that retirees do not outlive their assets. Annuities can also be used to supplement other sources of retirement income, such as Social Security, pensions, and withdrawals from retirement accounts, enhancing overall financial stability.

There are different types of annuities available, such as fixed annuities and variable annuities, and it is important to understand the fees and charges associated with each. For example, variable annuities have fees that include mortality and administrative expenses, while fixed annuities offer a guaranteed rate of return, reducing investment risk. When purchasing an annuity, you can choose to delay withdrawals until retirement or start them immediately, with various options offering different levels of risk and return.

Before purchasing an annuity, it is recommended to seek advice from a tax advisor or financial planner to understand if it is the right decision for your individual circumstances. It is also important to evaluate the strength and ability of the insurance company providing the annuity guarantees, as these are critical considerations.

Life Insurance and Mass Health: Incompatible or Not?

You may want to see also

Frequently asked questions

Annuities are a contract between you and an insurance company that offers a way to reduce taxes and/or ensure a steady flow of income.

Annuities are insurance contracts that do not have federal government insurance. However, guaranty associations in all 50 states, including Washington, cover at least $250,000 in annuity benefits for customers if the insurance company that issued the contract goes out of business.

There are fixed annuities, variable annuities, and indexed annuities. Fixed annuities provide a guaranteed rate of return over a specific period. Variable annuities tie your payments to the performance of investment sub-accounts, offering higher returns but also carrying market risk. Indexed annuities bridge the gap between fixed and variable options, earning interest based on the performance of a market index while typically offering a minimum guaranteed return.

To purchase an annuity, you can either pay a large, single premium or make payments over time in exchange for future income. It is recommended that you talk with a tax advisor or financial planner to determine if an annuity is right for you.