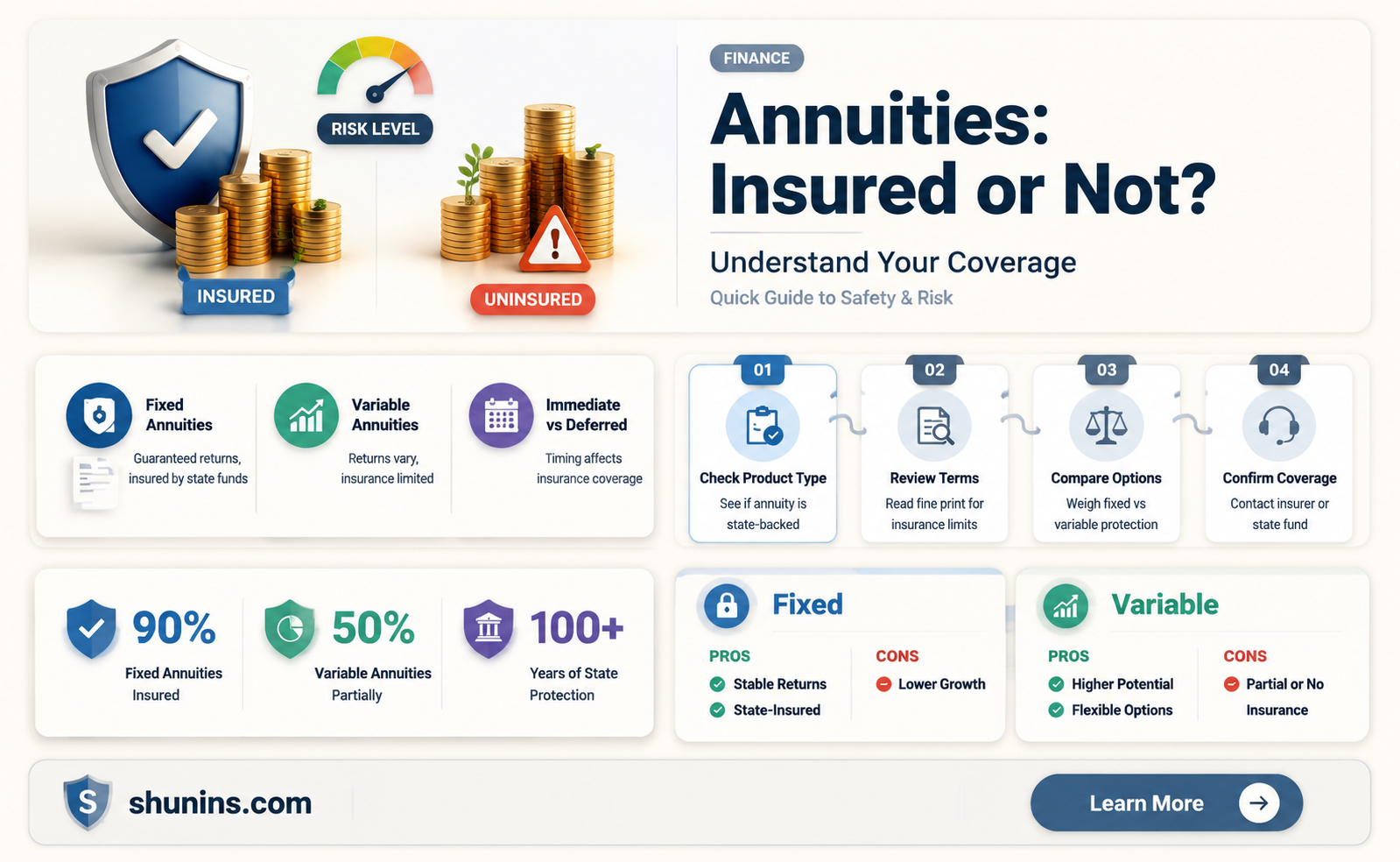

Annuities are insurance contracts designed to provide a guaranteed stream of income, making them a popular choice for retirees. They are typically considered safe investments that can provide guaranteed income in retirement. However, annuities are not insured by the Federal Deposit Insurance Corporation (FDIC) or any other federal agency. Instead, they are backed by the financial strength of insurance companies and regulated primarily at the state level. While annuities are generally low-risk, they are not entirely risk-free, and fees can diminish returns. Certain protections are in place if the issuing insurer goes out of business, and state guaranty associations offer additional protection, with coverage levels varying across states.

| Characteristics | Values |

|---|---|

| Definition | An annuity is an insurance contract designed to provide a guaranteed stream of income, making it a popular choice among retirees. |

| Types | Fixed, variable, and indexed annuities. |

| Issuers | Only insurance companies can issue annuities, but they are often available for purchase through banks, brokerage firms, and financial advisors. |

| Safety | Annuities are typically considered safe investments, but they are not entirely risk-free. Fees could diminish returns, and the money is not insured by the Federal Deposit Insurance Corporation (FDIC). |

| Regulation | Annuities are regulated at the state level by state insurance commissioners and state guaranty associations. Coverage levels can vary across states. |

| Protection | In the event of an insurance company's failure, state guaranty associations offer additional protection, usually up to $250,000. |

Explore related products

What You'll Learn

![]()

Annuities are not FDIC-insured

Annuities are not insured by the Federal Deposit Insurance Corporation (FDIC). This is because annuities are insurance products, not banking products, and only the latter are protected by the FDIC. However, annuities are protected by several layers of security, including state guaranty associations and insurance company safeguards. These protections are designed specifically for insurance products and provide comparable or even superior security for your investment.

State guaranty associations typically provide protection ranging from $100,000 to $500,000 per person, depending on the state of residence. For example, New York provides up to $500,000 in coverage, while California offers $250,000 in protection. Most other states provide at least $100,000 in coverage. Annuities are also protected by the insurance company's own financial strength, including substantial reserves that are strictly regulated and regularly audited.

While annuities are typically considered safe, it's important to remember that they are not entirely risk-free. Fees could diminish your returns, and the value of your money could decrease over time due to inflation. Different types of annuities also carry varying levels of risk. For example, fixed annuities offer low risk and guaranteed returns, while variable annuities are similar to mutual fund investments and may not guarantee the principal.

Before purchasing an annuity, it is essential to understand the specific protections and risks associated with these financial products. Working with qualified financial professionals can help you make informed decisions about your retirement investments and ensure your money is protected.

Protective Life Insurance: Exam-Free Option for Policyholders

You may want to see also

Explore related products

![]()

State guaranty associations offer protection

Annuities are generally considered safe investments that can provide guaranteed income in retirement. However, they are not without risk. Annuities are not insured by the Federal Deposit Insurance Corporation (FDIC) or any other federal agency. Instead, annuities are insured by state guaranty associations, which offer protection to annuity owners in the event that the issuing insurance company becomes insolvent.

State guaranty associations act as a safety net to protect policyholders if the insurance company that issued an annuity or insurance policy cannot meet its financial obligations. These associations are typically non-profit organizations governed by the state's insurance commissioner and an appointed board of directors. Coverage levels can vary from state to state, with most states having annuity coverage limits of $250,000. It's important to note that state guaranty associations prohibit insurance agents from mentioning their coverage to promote the sale of annuities or insurance.

The purpose of state guaranty associations is to protect consumers in the event that an insurance company in their state fails. Each state has its own guaranty fund or association, and any company selling insurance policies or annuities is required to belong to the state guaranty association in each state where they do business. This ensures that annuity customers have financial protection and that their investments are safeguarded even if the insurance company goes out of business.

While state guaranty associations provide important protection for annuity owners, it's worth noting that they do not guarantee against all risks associated with annuities. Fees and charges associated with annuities can diminish returns, and it's possible to lose money when investing in annuities. Therefore, it is recommended to carefully consider the potential risks and rewards before investing in annuities and to seek advice from a financial professional.

Life Insurance Cash Out: When and How?

You may want to see also

Explore related products

![]()

Annuities are protected by the insurer's financial strength

Annuities are a type of insurance contract that provides a guaranteed stream of income, making them popular among retirees. People typically buy annuities to help manage their income in retirement. They provide three things: periodic payments for a specific amount of time, death benefits, and a guaranteed rate of return.

Annuities are generally considered safe investments, but they are not entirely risk-free. While fees could diminish returns, certain protections are in place to safeguard your investment. Annuities are insured by state guaranty associations, and coverage levels vary from state to state. In addition, there may be state guarantees in the event of an insurance company's failure. However, annuities are not guaranteed by the Federal Deposit Insurance Corporation (FDIC), Securities Investor Protection Corporation (SIPC) or any other federal agency.

The financial strength of the insurance company issuing the annuity is an important consideration. You want to be sure that the company will still be around and financially sound during your payout phase. Five credit rating agencies assess the financial strength of insurance companies in the US: AM Best, Fitch, Kroll Bond Rating Agency (KBRA), Moody's, and S&P Global. Each agency has its own criteria and rating systems, which may include minor variations in ratings. The insurance financial strength rating issued by KBRA assesses a company's overall financial health and ability to meet policyholder obligations.

When looking at insurance company and annuity carrier ratings, it is important to consider multiple ratings as companies may publicize only their highest ratings. While these agencies do not recommend specific products, their assessments and official ratings can influence annuity purchase decisions.

Understanding Insurance: Treatment Approval and Coverage

You may want to see also

Explore related products

![]()

Reinsurers act as a financial safety net

Annuities are insurance contracts that provide a guaranteed stream of income, making them a popular choice for retirees. They are generally considered safe investments, but they are not entirely risk-free. While annuities are not insured by the Federal Deposit Insurance Corporation (FDIC), Securities Investor Protection Corporation (SIPC), or any federal agency, certain protections are in place to safeguard your investment in the event of an insurance company's failure. These protections include state guaranty associations, with coverage levels varying across states.

Reinsurance, often referred to as "insurance for insurance companies," serves as a crucial risk management tool. It allows insurance companies to transfer a portion of their financial risk to another company, known as the reinsurer. This transfer of risk helps insurers maintain financial stability and enhances their ability to underwrite more policies. By assuming some of the insurer's risks, the reinsurer provides a financial safety net that protects the insurer from accumulated liabilities and helps them handle financial pressure during significant events or catastrophes.

In the event of substantial losses, the reinsurer bears a portion of the financial burden, reducing the insurer's net liability. This risk-sharing arrangement enables insurers to expand their capacity, stabilize results, and protect themselves from large or multiple losses. Reinsurance also makes substantial liquid assets available to insurers, fostering equilibrium within the insurance market. The relationship between the insurer and the reinsurer is governed by a formal contract, which can include special clauses in the event of insolvency.

The role of reinsurers as financial safety nets is particularly evident in the case of ceding companies, where the reinsurer assumes insurance risk in exchange for credit risk. Ceding companies carefully select their reinsurers, monitoring their financial ratings and aggregated exposures. Reinsurance allows ceding companies to take on more and bigger risks while maintaining their solvency. It also enables them to issue policies with higher limits and enhance their risk management capabilities.

In summary, reinsurers act as a financial safety net for insurance companies by sharing their risks, absorbing losses, and providing financial stability. This, in turn, enables insurers to better protect their customers and maintain their operations during challenging economic times or in the face of catastrophic events.

Henrietta Lacks: Insurance and Healthcare Injustices

You may want to see also

Explore related products

![]()

Annuities are a form of insurance

While annuities are not insured by the Federal Deposit Insurance Corporation (FDIC) or the Securities Investor Protection Corporation (SIPC), they are backed by the financial strength of insurance companies themselves. State guaranty associations, present in all 50 states, provide additional protection in the event of an insurer's failure, with coverage levels varying across states. These associations are not insurance companies but rather nonprofit organizations that all annuity-selling companies in a state must join.

It is important to note that annuities are not entirely risk-free. Fees, such as mortality and expense risk fees, can reduce overall returns, and market fluctuations may impact fixed-rate annuities over time. Nonetheless, certain types of annuities, like registered index-linked annuities (RILAs), offer both upside limits and downside protection, providing a buffer against potential losses.

When considering the purchase of an annuity, it is advisable to carefully evaluate the insurer's stability and understand the specific protections and guarantees offered. While annuities can provide a sense of financial security, it is always wise to be informed about the potential risks and returns associated with any investment decision.

Quitting Tobacco: Better Life Insurance and a Healthier You

You may want to see also

Frequently asked questions

An annuity is an insurance contract designed to provide a guaranteed stream of income, making it a popular choice for retirees.

Annuities are not FDIC-insured but are backed by the financial strength of insurance companies. If an insurer fails, state guaranty associations offer additional protection, usually up to $250,000.

Annuities are generally considered safe investments that can provide guaranteed income in retirement. However, they are not entirely risk-free, as fees could diminish returns.

There are three types of annuities: fixed, variable, and indexed. Fixed annuities provide a guaranteed rate of return over a specific period, while variable and indexed annuities offer more flexibility but may come with higher risks.