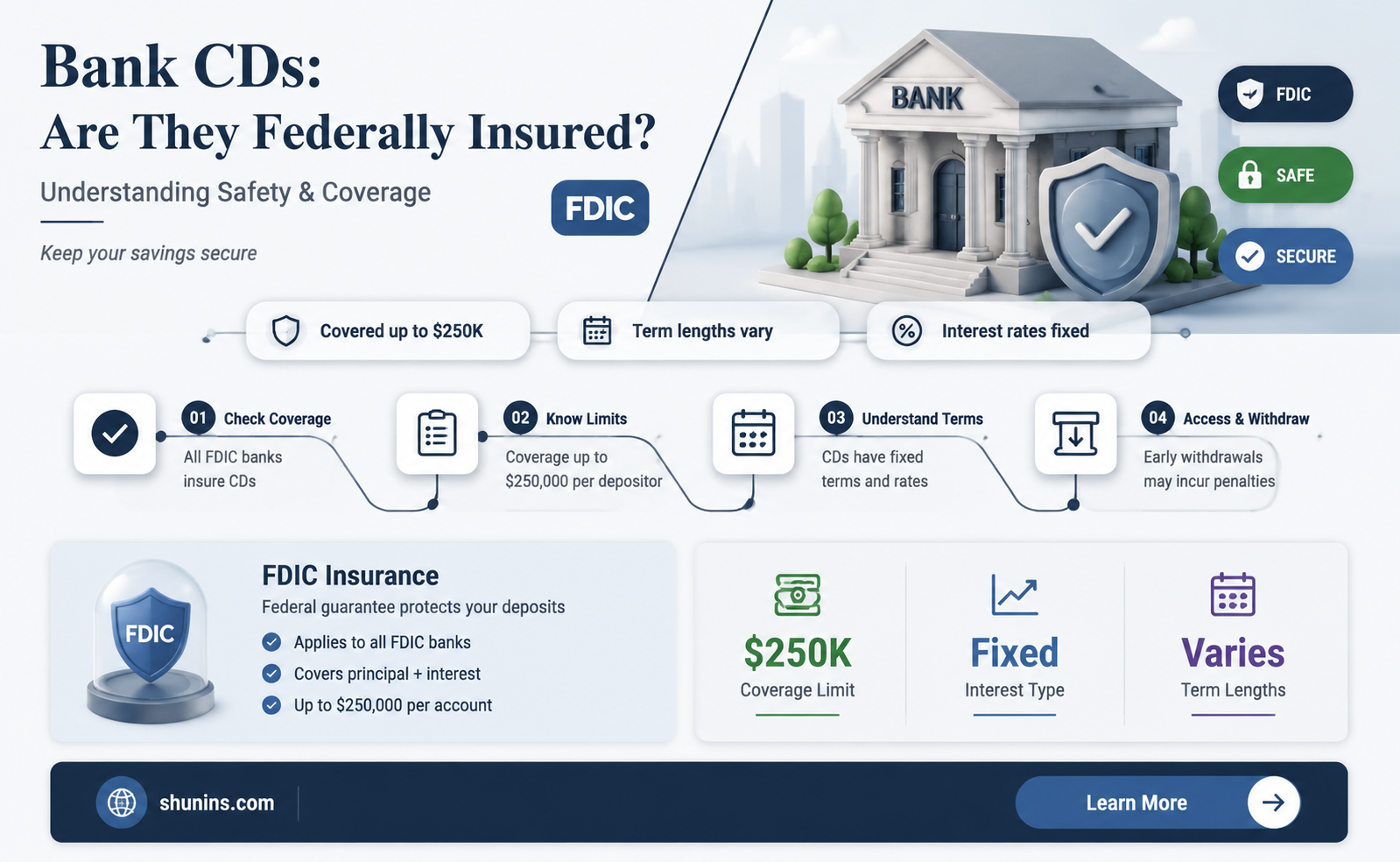

Certificates of deposit (CDs) are a type of deposit account that offers a higher rate of interest than a regular savings account. CDs are insured by the Federal Deposit Insurance Corporation (FDIC), an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event of bank failure. FDIC insurance is backed by the full faith and credit of the US government, and deposits are insured up to $250,000 per depositor, per FDIC-insured bank, and per ownership category. While most CDs are FDIC-insured, there are exceptions, such as when purchasing CDs through a non-bank institution or investing in foreign banks.

| Characteristics | Values |

|---|---|

| Are CDs federally insured? | Yes |

| Insurer | Federal Deposit Insurance Corporation (FDIC) |

| Insured amount | Up to $250,000 per depositor, per FDIC-insured bank, per ownership category |

| Insured amount for joint accounts | Up to $500,000 |

| Insured amount for credit union customers | Up to $250,000 per credit union per account owner |

| Insured amount for retirement accounts | Up to $250,000 |

| Insured amount for employee benefit plan accounts | Up to $250,000 |

| Insured amount for business accounts | Up to $250,000 |

| Insured amount for government accounts | Up to $250,000 |

| Insurer's website | www.fdic.gov |

| Insurer's phone number | 1-877-ASK-FDIC (1-877-275-3342) |

Explore related products

$20 $120.67

What You'll Learn

![]()

CDs are insured by the Federal Deposit Insurance Corporation (FDIC)

Certificates of deposit (CDs) are insured by the Federal Deposit Insurance Corporation (FDIC), an independent agency of the United States government. The FDIC was created in 1933 to protect bank depositors against the loss of their insured deposits in the event of an FDIC-insured bank failure. The FDIC insurance is backed by the full faith and credit of the US government, and it is provided automatically to any deposit account opened at an FDIC-insured bank. This insurance covers deposits up to $250,000 per depositor, per FDIC-insured bank, per ownership category. For example, a $250,000 certificate of deposit in a single-owner account would be fully insured in the event of a bank failure or liquidation.

The FDIC provides separate insurance coverage for deposit accounts held in different categories of ownership, including single, joint, revocable trust, irrevocable trust, certain retirement plans, employee benefit plans, business, and government accounts. The standard deposit insurance coverage limit is $250,000, but it is possible to qualify for more than this amount if you own deposit accounts in multiple ownership categories. For example, a joint account with two owners would have coverage of up to $500,000 in the event of a bank failure.

It is important to note that not all CDs are automatically insured by the FDIC. CDs purchased through a third-party broker or a non-bank institution, such as a brokerage firm, may not carry FDIC insurance. Additionally, some types of CDs, such as those that involve investing money in foreign banks, do not carry FDIC insurance. To ensure that your CD is insured, it is important to purchase it from an FDIC-insured bank and understand all the terms and conditions of the account.

Overall, the FDIC insurance on CDs provides peace of mind and security for individuals looking to save their money in a low-risk manner while also earning higher interest rates compared to traditional savings accounts.

Navy Federal Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

FDIC insurance covers up to $250,000 per depositor

FDIC insurance covers your deposits up to a limit of $250,000 per depositor, per FDIC-insured bank, per ownership category. This means that if you have multiple accounts in different ownership categories at the same bank, your total coverage may exceed $250,000. For example, if you have a single ownership savings account and a joint ownership checking account at the same FDIC-insured bank, you will be covered for up to $250,000 for your single ownership account and an additional $250,000 for your joint ownership account.

The FDIC, or Federal Deposit Insurance Corporation, is an independent agency of the United States government that insures deposits at banks and savings associations. This insurance protects bank customers in the event that an FDIC-insured institution fails. FDIC insurance is backed by the full faith and credit of the United States government, ensuring that depositors will receive their money back, up to the insurance limit.

Most banks are FDIC-insured, and you can check if your bank is insured by looking for the "Member FDIC" or FDIC logo on their website or using the FDIC's BankFind tool. FDIC insurance is automatic and free for depositors, and it covers a variety of deposit accounts, including checking accounts, savings accounts, money market accounts, and certificates of deposit (CDs).

CDs, or certificates of deposit, are considered a safe way to save money due to their FDIC insurance coverage. CDs typically offer higher interest rates than traditional savings accounts but require you to keep your money in the account for a specified period. If you need to withdraw your money early, you may have to pay a fee or penalty. Overall, CDs are a low-risk option for those looking to grow their savings over time while enjoying the peace of mind that comes with FDIC insurance.

US Bank Insurance: Is Your Money Safe?

You may want to see also

Explore related products

![]()

The FDIC is an independent agency of the US government

Certificates of deposit (CDs) are considered a safe way to save money because they are federally insured. The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that provides deposit insurance and maintains the safety of the US banking system. The FDIC was established by the Banking Act of 1933 during the Great Depression to restore trust in the American banking system. Over a third of banks failed in the years before the FDIC's creation, and bank runs were common.

The FDIC is an independent agency in the sense that it exists outside the federal executive departments and the Executive Office of the President. While it is considered part of the executive branch, it has regulatory and rulemaking authority and is insulated from presidential control. The FDIC's primary source of funding comes from member banks' insurance dues, and it charges premiums based on the risk that the insured bank poses.

The FDIC provides deposit insurance to depositors in American commercial banks and savings banks. This insurance is automatic for any deposit account opened at an FDIC-insured bank, and it is backed by the full faith and credit of the US government. The FDIC insures deposits up to $250,000 per depositor, per FDIC-insured bank, per ownership category. This limit has increased over time to accommodate inflation.

In the unlikely event of a bank failure, the FDIC responds by paying insurance to depositors up to the insurance limit. The FDIC has the authority to regulate and supervise state non-member banks, and it can also examine and supervise certain financial institutions for safety and soundness. Overall, the FDIC plays a crucial role in maintaining the stability and integrity of the US banking system.

Vanguard Accounts: Are They Federally Insured?

You may want to see also

Explore related products

![]()

CDs are a safe way to save money

Certificates of deposit (CDs) are a safe way to save money. They are federally insured, low-risk savings accounts that generally pay higher interest rates than traditional savings accounts. The Federal Deposit Insurance Corporation (FDIC) insures CDs at banks, and the National Credit Union Administration (NCUA) insures CDs at credit unions. This insurance protects your money in the rare event that your financial institution closes. Coverage is up to $250,000 per person per account ownership type, with joint accounts receiving up to $500,000 in coverage.

CDs are a safe option for those seeking to grow their savings over time. By committing to keeping your money in the account for a specified term, you can benefit from higher interest rates. These terms typically range from one month to several years, with longer durations offering even more attractive rates. However, early withdrawal may result in penalties, so it is important to consider your financial goals and time horizon when selecting a CD.

The FDIC was established in 1933 to protect depositors of failed banks and maintain the stability of the US banking system. It is an independent agency of the US government, and its insurance is backed by the full faith and credit of the nation. This means that in the unlikely event of a bank failure, the FDIC guarantees that you will receive your money back, up to the insured limit.

While most CDs are federally insured, there are some exceptions. For example, purchasing a CD from a foreign bank or through a non-bank institution like a brokerage firm may not carry FDIC insurance. It is important to carefully review the terms and conditions of your CD account to understand the level of insurance coverage provided. Additionally, be cautious of marketing ploys that offer temporarily high CD rates to lure customers into purchasing uninsured, long-term investments.

Overall, CDs are a secure option for those looking to grow their savings over time. With federal deposit insurance and higher interest rates, you can have peace of mind that your money is protected and working harder for you. However, it is always important to do your due diligence and understand the specific terms and conditions of any financial product before committing to it.

RBFCU: Federally Insured, Safe and Secure

You may want to see also

Explore related products

![]()

You can check if a bank is FDIC-insured on its website or the FDIC's BankFind tool

Most bank CDs (Certificates of Deposit) are federally insured by the FDIC (Federal Deposit Insurance Corporation). The FDIC is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank fails. FDIC insurance is backed by the full faith and credit of the United States government.

It is important to note that not all CDs carry deposit insurance, even when held at an FDIC-member bank. For example, CDs that involve investing money in foreign banks do not carry FDIC insurance. Additionally, you can purchase CD accounts through a non-bank institution such as a brokerage firm, which may also not carry FDIC insurance. Therefore, it is essential to check the terms and conditions of your CD account to understand whether it is insured or not.

Is Your 401(k) Safe? Federal Insurance and Your Retirement

You may want to see also

Frequently asked questions

Yes, most CDs are insured by the Federal Deposit Insurance Corporation (FDIC), an independent agency that provides deposit insurance and maintains the safety of the U.S. banking system.

Deposits at FDIC-insured banks are covered up to $250,000 per person per account ownership type. For joint accounts with two owners, coverage of up to $500,000 would kick in if a bank fails.

One way to check for coverage is by scrolling to the bottom of a bank’s website to find the acronym FDIC or NCUA. You can also look up your financial institution’s status on the FDIC’s BankFind tool or the NCUA’s Credit Union Locator widget.