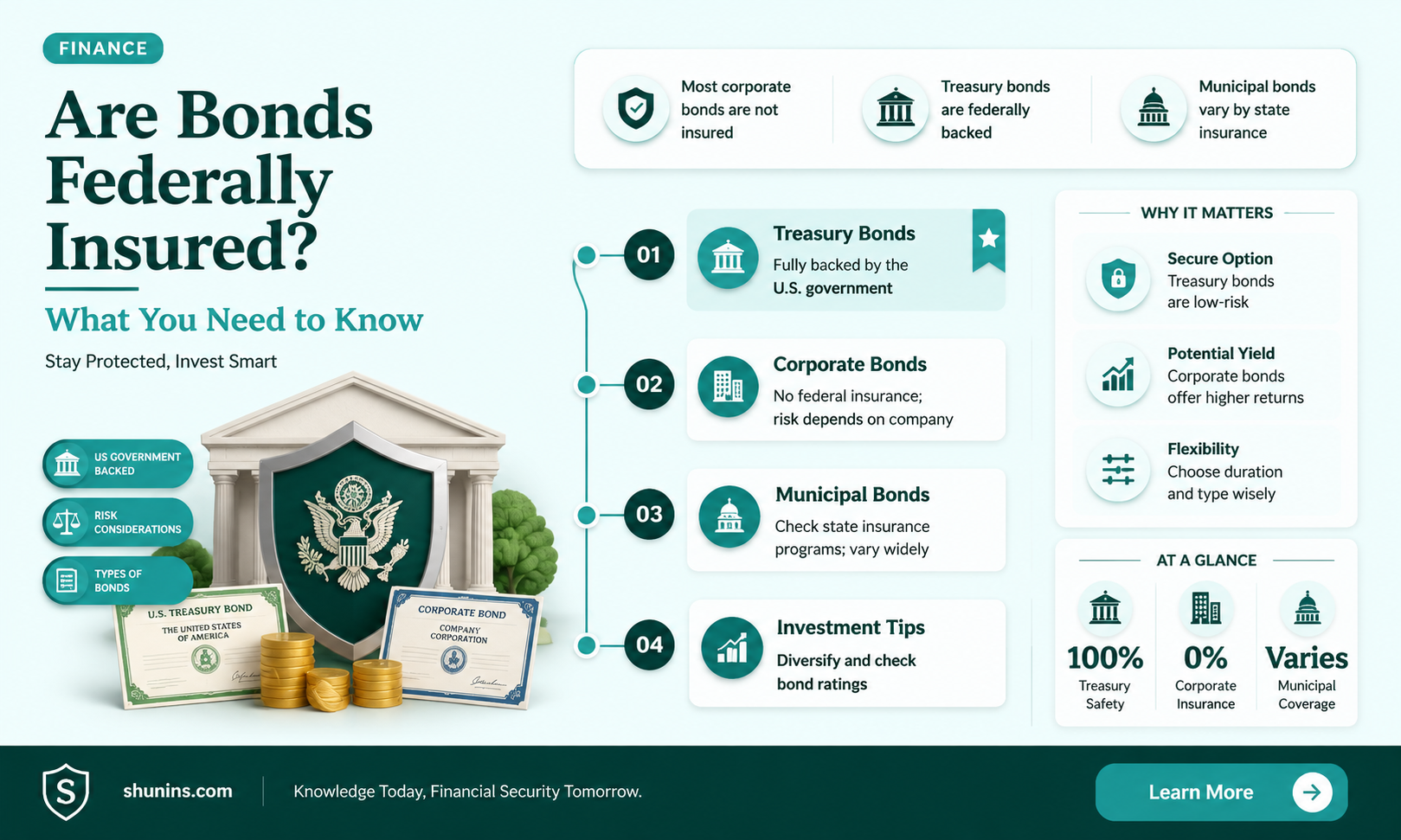

Bonds are not insured by the Federal Deposit Insurance Corporation (FDIC) because they are not considered deposits. Bonds are loans made by investors to borrowers, and when you buy a bond, you are lending money to the entity issuing the bond. The FDIC is an independent agency of the US government that insures deposits in specific accounts at FDIC-insured banks, protecting depositors against the loss of their deposits if an insured bank fails. FDIC insurance covers depositors' accounts dollar-for-dollar, including principal and interest, up to a standard limit of $250,000 per depositor per insured bank. While the FDIC does not insure bonds, the Securities Investor Protection Corporation (SIPC) may provide protection if a brokerage firm fails, with coverage of up to $500,000 in securities.

| Characteristics | Values |

|---|---|

| Are bonds federally insured? | No, bonds are not insured by the Federal Deposit Insurance Corporation (FDIC) |

| Why aren't bonds insured by the FDIC? | Bonds are not considered deposits, but investments. FDIC only insures specific deposit accounts at FDIC-insured banks. |

| Are there any alternatives to protect bonds? | Yes, the Securities Investor Protection Corporation (SIPC) may protect customers if their brokerage firm fails. |

Explore related products

What You'll Learn

![]()

FDIC insures deposits, not investments

The Federal Deposit Insurance Corporation (FDIC) provides deposit insurance, which covers depositors' accounts at insured banks, including any accrued interest, up to a limit of $250,000 per depositor, per insured bank, for each account ownership category. This means that if you have a single ownership account in one FDIC-insured bank, and another single ownership account in a different FDIC-insured bank, you will be insured separately for up to $250,000 in each bank. FDIC insurance covers all types of deposits received at an insured bank, including checking, savings, and money market deposit accounts (MMDAs).

It is important to note that FDIC insurance does not cover non-deposit investments or investment products, even if they were purchased at an insured bank. This includes U.S. Treasury bills, bonds, or notes. These investments are not insured by the FDIC but are backed by the full faith and credit of the U.S. government.

While FDIC insurance does not cover investments, there are other forms of protection for investors. For example, the Securities Investor Protection Corporation (SIPC) is a nonprofit membership corporation that protects customers of SIPC-member broker-dealers if the firm fails financially. SIPC insurance covers investors for up to $500,000 in securities, with up to $250,000 in cash balances.

In summary, FDIC insurance specifically covers deposits and not investments. Investors seeking protection for their investments may need to explore alternative options, such as those offered by the SIPC. It is always important to understand the risks associated with any investment and to ensure that your bank is FDIC-insured to protect your deposits.

Wells Fargo: Is Your Money Insured?

You may want to see also

Explore related products

![]()

FDIC does not insure bonds

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that provides insurance to protect depositors against bank failures. FDIC insurance covers depositors' accounts at each insured bank, including principal and any accrued interest, up to a limit of $250,000 per depositor, per insured bank, for each account ownership category.

However, it is important to note that FDIC insurance does not cover non-deposit investments or investment products, even if they were purchased at an insured bank. This includes U.S. Treasury bills, bonds, or notes. Bonds are not insured by the FDIC because they are considered investments rather than deposits, and they carry their own set of risks. When an investor purchases a bond, they are lending money to the entity issuing the bond, which could be a corporation, a municipality, or the federal government. The issuer promises to pay the investor a specified rate of interest during the life of the bond and to repay the principal when the bond matures or comes due.

The risk associated with bonds is that the issuer might default, failing to pay the interest or principal as promised. This risk depends on the creditworthiness of the issuer. While U.S. government bonds, also known as Treasury bonds, have a very low risk of default, other types of bonds may have a higher risk of default depending on the issuer.

It is worth noting that while the FDIC does not insure bonds, the Securities Investor Protection Corporation (SIPC) may offer some protection to customers if their brokerage firm fails. However, SIPC protection has its limitations and does not cover losses due to a decline in the market value of securities.

In summary, investors should be aware that FDIC insurance does not extend to bonds or other investment products. The FDIC only insures specific deposit accounts at FDIC-insured banks, up to the specified limit.

Savings Accounts: Federally Insured or Not?

You may want to see also

Explore related products

![]()

SIPC protection is limited

The Securities Investor Protection Corporation (SIPC) is a nonprofit corporation created by an act of Congress in 1970 to protect the clients of brokerage firms that are forced into bankruptcy. It is not an agency, nor is it part of the United States government.

SIPC insurance covers investors for up to $500,000 in securities, of which up to $250,000 can be cash balances. This means that if a brokerage firm fails financially, SIPC will step in to make the investor whole by providing up to $500,000 in coverage. However, SIPC does not protect against the decline in value of securities. It does not protect individuals who are sold worthless stocks and other securities, nor does it protect against losses due to a broker's bad investment advice or inappropriate investment recommendations.

SIPC does not provide blanket coverage. It does not protect cash held in connection with a commodities trade, nor does it cover digital asset securities that are investment contracts not registered with the US Securities and Exchange Commission. SIPC also does not investigate fraud or securities crimes.

It is important to note that SIPC protection is not the same as FDIC insurance, which covers depositors' accounts at insured banks, dollar-for-dollar, including principal and any accrued interest up to the insurance limit of $250,000 per depositor, per insured bank, for each account ownership category.

Ally Bank: Is Your Money Safe and Federally Insured?

You may want to see also

Explore related products

![]()

CDs are federally insured

Certificates of deposit (CDs) are considered a safe way to save money because they are federally insured. The Federal Deposit Insurance Corporation (FDIC) is an independent agency that provides deposit insurance and maintains the safety of the U.S. banking system. FDIC insurance covers depositors' accounts at each insured bank, including principal and any accrued interest, up to a limit of $250,000 per depositor, per bank, for each account ownership category. This means that if you have a CD at an FDIC-insured bank and the bank fails, you are guaranteed to receive your money back, up to the $250,000 limit, by the full faith and credit of the U.S. government.

It is important to note that not all CDs are automatically insured. While many CD accounts come with FDIC coverage, there are exceptions. For example, if you purchase a CD from a third-party broker instead of directly from an FDIC-insured bank, you will need to rely on the broker to make your deposit and acquire the CD on your behalf. In this case, your money will not be insured by the FDIC if the broker does not place your funds into an FDIC-insured bank. Additionally, some CDs, such as those purchased through a non-bank institution like a brokerage firm, may not carry FDIC insurance.

To ensure that your CD is federally insured, you can look for the acronym "FDIC" or "Member FDIC" at the bottom of a bank's website or on its marketing materials. You can also use the FDIC's BankFind tool to look up the status of your financial institution. By confirming that your CD account is FDIC-insured, you can have peace of mind that your savings are protected.

CDs are a popular investment option as they offer a higher rate of interest than regular savings accounts, typically ranging from one month to several years. They are considered low-risk and provide a steady and predictable investment income. By choosing CDs, investors can benefit from the security of federal deposit insurance while also enjoying higher interest rates compared to traditional savings accounts.

Vanguard Accounts: Are They Federally Insured?

You may want to see also

![]()

US government bonds are low-risk

US government bonds are often considered low-risk investments due to the stability of the US government and its track record of honouring its debt obligations. The US government has never defaulted on debt payments, which inspires confidence in investors. This perception of US government bonds as "risk-free" leads to lower rates of return compared to other investments, such as the stock market.

While the US government's commitment to paying interest and principal payments is reliable, there are other risks associated with long-term US government bonds. These include interest rate risk, which refers to the possibility of a loss in value if interest rates increase. When interest rates change, bond prices fluctuate in the opposite direction, and long-term bonds experience greater price volatility. Additionally, there is the risk that inflation will erode the value of income received over time, resulting in a decline in the principal amount.

US Treasury bonds are exempt from state income taxes, providing tax benefits that other investments may not offer. This adds to their appeal as a low-risk investment option. However, it is important to note that while the US government backs these bonds, they are not insured by the Federal Deposit Insurance Corporation (FDIC) or any other federal government agency.

When considering US government bonds as an investment option, it is crucial to assess your financial needs, investment goals, and risk tolerance. While these bonds offer stability and security, they may not provide the same high returns as other investments. Diversification of your investment portfolio is essential to balance risk and return according to your financial objectives.

M&T Bank: Is Your Money Safe and Federally Insured?

You may want to see also

Frequently asked questions

No, bonds are not federally insured. The Federal Deposit Insurance Corporation (FDIC) only insures specific deposit accounts at FDIC-insured banks, and bonds are considered investments, not deposits.

The FDIC insures depositors' accounts at each insured bank, including principal and any accrued interest, up to a limit of $250,000 per depositor, per insured bank, for each account ownership category.

The FDIC is an independent agency of the US government that has been operating since 1934. It protects depositors against the loss of their deposits if an insured bank fails.

Yes, the Securities Investor Protection Corporation (SIPC) is a nonprofit membership corporation created by federal statute in 1970. SIPC protects customers of SIPC-member broker-dealers if the firm fails financially.

Yes, Certificates of Deposit (CDs) are federally insured and issued by banks and savings-and-loans institutions. CDs are considered bank deposits and are backed by FDIC insurance up to $250,000 per bank per depositor.