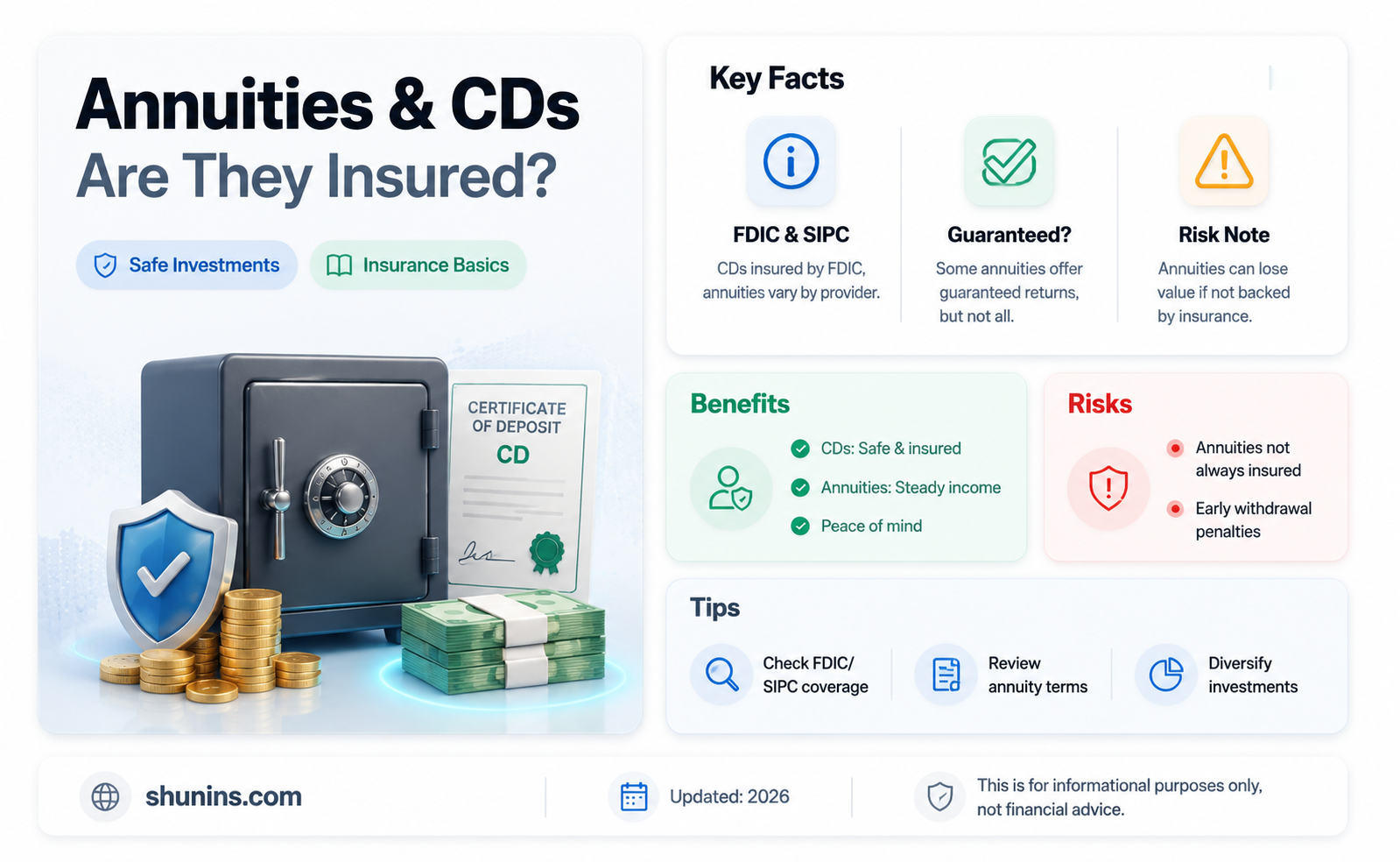

Annuities and certificates of deposit (CDs) are both popular investment options for retirees. CDs are federally insured by the Federal Deposit Insurance Corporation (FDIC), which guarantees your money up to $250,000 per person per account ownership type. Annuities, on the other hand, are not FDIC-insured, but they do have alternative protection mechanisms through state guaranty associations and insurance company safeguards. While annuities do not have federal government insurance, guaranty associations in all 50 states provide protection ranging from $100,000 to $500,000 per person, depending on the state.

Explore related products

$14.99

What You'll Learn

![]()

Annuities are not federally insured but have state-based protection

Annuities are not federally insured, but they do have state-based protection. Annuities are insurance contracts that offer a guaranteed income stream, making them a popular choice for retirees. They are often purchased through banks, brokerage firms, or financial advisors. While annuities don't have federal government insurance, guaranty associations in all 50 states provide protection for annuity benefits. This protection typically ranges from $100,000 to $500,000 per person, depending on the state. For example, New York provides up to $500,000 in coverage, while California offers $250,000.

The state guaranty associations step in if the insurance company that issued the annuity contract goes out of business. In such cases, the other companies in the guaranty association help pay the outstanding claims. These associations work similarly to FDIC insurance but are state-based. Before the state guaranty associations come into play, annuities are protected by the insurance company's own financial strength. Insurance companies are required to maintain substantial reserves and follow proper investment practices to meet their obligations. They undergo frequent regulatory examinations and audits to ensure compliance.

It's important to note that annuities have different types, such as fixed, variable, and indexed, each carrying varying levels of risk. While variable annuities and registered indexed-linked annuities (RILAs) are regulated at the national level by the SEC and FINRA, all annuities are regulated by state insurance commissioners. The lack of federal insurance doesn't mean annuity investments lack protection. State guaranty associations and insurance company safeguards provide alternative protection mechanisms that often offer comparable or even superior security for annuity investments.

When considering an annuity, it is advisable to consult a qualified financial advisor to determine how it fits into your retirement plan. Understanding the protections in place can help you make informed decisions about your retirement investments and provide peace of mind. Additionally, researching your state's specific coverage amounts and staying informed about any changes in state protection limits are important steps to take.

Edward Jones Accounts: Are They Federally Insured?

You may want to see also

Explore related products

![]()

Certificates of Deposit (CDs) are generally FDIC insured

Certificates of Deposit (CDs) are generally considered safe investments as they are federally insured. The Federal Deposit Insurance Corporation (FDIC) insures CDs issued by banks, and the National Credit Union Administration (NCUA) insures CDs issued by credit unions. FDIC insurance covers the principal amount of the CD and any accrued interest, up to $250,000 per account owner, per issuer. This coverage limit was made permanent in 2010 and includes both traditional bank CDs and brokered CDs.

The FDIC insurance provides protection in the rare event of a bank failure or liquidation. If a bank fails, the FDIC will first search for another bank willing to assume the insured accounts. If this is not possible, the FDIC reimburses account holders according to the insurance limits. While CDs are generally insured, there are exceptions. Some types of CDs, such as those held in foreign banks or purchased through a non-bank institution like a brokerage firm, may not carry FDIC insurance.

Compared to other investments, CDs offer a low-risk option with minimal volatility. They provide a fixed interest rate over a specified term, typically ranging from a few months to several years. CDs are suitable for short-term savings goals and can offer higher interest rates than traditional savings accounts. However, early withdrawal from a CD may result in penalties and fees.

While both CDs and annuities are considered stable and secure retirement investments, annuities are not federally insured. Annuities are backed by the issuing insurance company, and their safety depends on the insurer's financial stability and claims-paying ability. State guaranty associations provide additional protection for annuities, but there is a chance that only a portion of the claim may be paid.

In summary, Certificates of Deposit (CDs) are generally FDIC-insured up to $250,000 per account, making them a safe and stable investment option. Annuities, while also considered secure, are not federally insured and rely on the financial stability of the issuing insurance company.

Ally Bank: Is Your Money Safe and Federally Insured?

You may want to see also

Explore related products

![]()

CDs are a low-risk alternative to traditional savings accounts

CDs, or Certificates of Deposit, are a low-risk alternative to traditional savings accounts. They are a type of savings account offered by banks and credit unions, with a guaranteed rate of interest in exchange for a commitment to leave your money deposited for a specified term. CDs are insured by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA) for up to $250,000 per depositor, institution, and account category. This means that your money is protected even if the bank fails. CDs offer a fixed interest rate, which is typically higher than that of traditional savings accounts, and the rate is locked in when you make your deposit, so it won't change during the term.

Traditional savings accounts usually offer minimal annual percentage yields (APYs), sometimes as low as 0.01%. In contrast, CDs can offer APYs of 4.5% or more, and some as high as 4.65% or even 5%. This makes a significant difference in interest earnings. The higher APY of CDs, combined with their fixed rate, makes it easier to calculate how much interest you'll earn over time and protects your funds from rate drops.

CDs are also more flexible than annuities, with shorter terms and lower penalties for early withdrawals. With a CD, you can usually withdraw all your money, along with the interest earned, with no penalty after the first 6 days following the date you funded the account. However, there are different types of CDs with varying withdrawal penalties, so it's important to understand the terms of your specific CD account.

While CDs do offer higher interest rates and insured protection, there are some drawbacks to consider. Firstly, CDs often require a minimum deposit to open an account, typically ranging from $500 to $1,000. Additionally, most CDs only allow a one-time deposit, so you can't regularly add money to your savings over time. Finally, CDs may not be ideal if you need frequent access to your funds, as they are designed for short- to medium-term investments.

In summary, CDs are a low-risk alternative to traditional savings accounts due to their federally insured protection, higher and fixed interest rates, and guaranteed returns. However, they may not be as flexible as traditional savings accounts in terms of access to funds and the ability to make regular deposits. When deciding between a CD and a traditional savings account, it's important to consider your financial goals, the amount of money you want to deposit, and your savings timeline.

TD Bank Customers: Is Your Money Federally Insured?

You may want to see also

![]()

CDs purchased from third-party brokers may not be insured

Certificates of Deposit (CDs) are considered a safe investment option as they are protected by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA) for up to $250,000 per account. However, it is important to note that this insurance coverage only applies to CDs purchased directly from banks or credit unions. When it comes to CDs bought through third-party brokers, the insurance coverage may not be as comprehensive.

Brokered CDs are CDs that are purchased through a broker or brokerage firm rather than directly from a bank. While brokered CDs still offer the benefits of traditional CDs, such as FDIC insurance and a fixed interest rate, there are some key differences. One advantage of brokered CDs is that they can provide access to higher interest rates and longer terms compared to traditional CDs. They also offer more flexibility, as they can be sold on the secondary market if you need access to your funds before maturity.

However, one important consideration regarding brokered CDs is that they may not always be FDIC-insured. While the FDIC insurance still applies to brokered CDs issued by banks, the coverage may not extend to CDs purchased through third-party brokers. This is because the brokered CDs are not directly issued or guaranteed by the bank, but rather sold through an intermediary. Therefore, it is crucial to carefully review the terms and conditions of brokered CDs to understand the level of insurance protection provided.

Additionally, it is worth noting that brokered CDs may come with additional risks and complexities. For example, if you sell a brokered CD before maturity, you may face a loss, especially in a rising interest rate environment. There may also be transaction fees or sales charges associated with buying or selling brokered CDs on the secondary market, which can impact your overall returns.

In summary, while CDs purchased directly from banks or credit unions are typically insured by the FDIC or NCUA, the same level of insurance protection may not apply to CDs bought through third-party brokers. It is important for investors to carefully evaluate the risks and benefits of brokered CDs and understand the specific terms and conditions of their investments to make informed decisions.

Navy Federal Insurance: NCUA-Insured Deposits

You may want to see also

![]()

CDs with foreign banks are not FDIC insured

Certificates of Deposit (CDs) are generally considered a safe investment option. They are protected by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA) for up to $250,000 per account. However, it's important to note that this insurance only applies to CDs issued by banks or credit unions that are members of these federal deposit insurance agencies.

When it comes to CDs with foreign banks, the FDIC insurance coverage may not apply. Foreign banks that reside in the US may offer Yankee CD accounts, which are available in US dollar denominations but typically do not come with FDIC insurance. These CDs may be purchased through a non-bank institution, such as a brokerage firm, which also may not carry FDIC insurance.

It is essential to carefully review the terms and conditions of any CD account, especially when considering an uninsured option. Uninsured CD accounts may offer higher interest rates to compensate for the lack of FDIC insurance and the increased risk. While some foreign banks may have subsidiaries in the US and contribute to the insurance fund, it is not a guarantee, and it is crucial to evaluate your risk tolerance and the issuing bank's stability.

Fidelity, for example, offers Brokered CDs that are FDIC-insured. However, the insurance is provided by the underlying bank, not Fidelity itself. Therefore, it is important to verify the FDIC status of the specific foreign bank offering the CD to ensure coverage.

In summary, while most CDs are FDIC-insured, CDs with foreign banks may not be. It is important to carefully review the terms and conditions and consider the risks associated with uninsured accounts.

Understanding the Federal Insurance Contributions Act

You may want to see also

Frequently asked questions

No, annuities are not federally insured. However, they are protected by state guaranty associations and insurance company safeguards.

State guaranty associations typically provide protection ranging from $100,000 to $500,000 per person, depending on the state of residence.

Yes, most CDs are federally insured by the Federal Deposit Insurance Corporation (FDIC).

Deposits at FDIC-insured banks are covered up to $250,000 per person per account ownership type.

CDs are considered a safe way to save money as they are federally insured and generally only face charges and fees if you withdraw your money before the term is up.