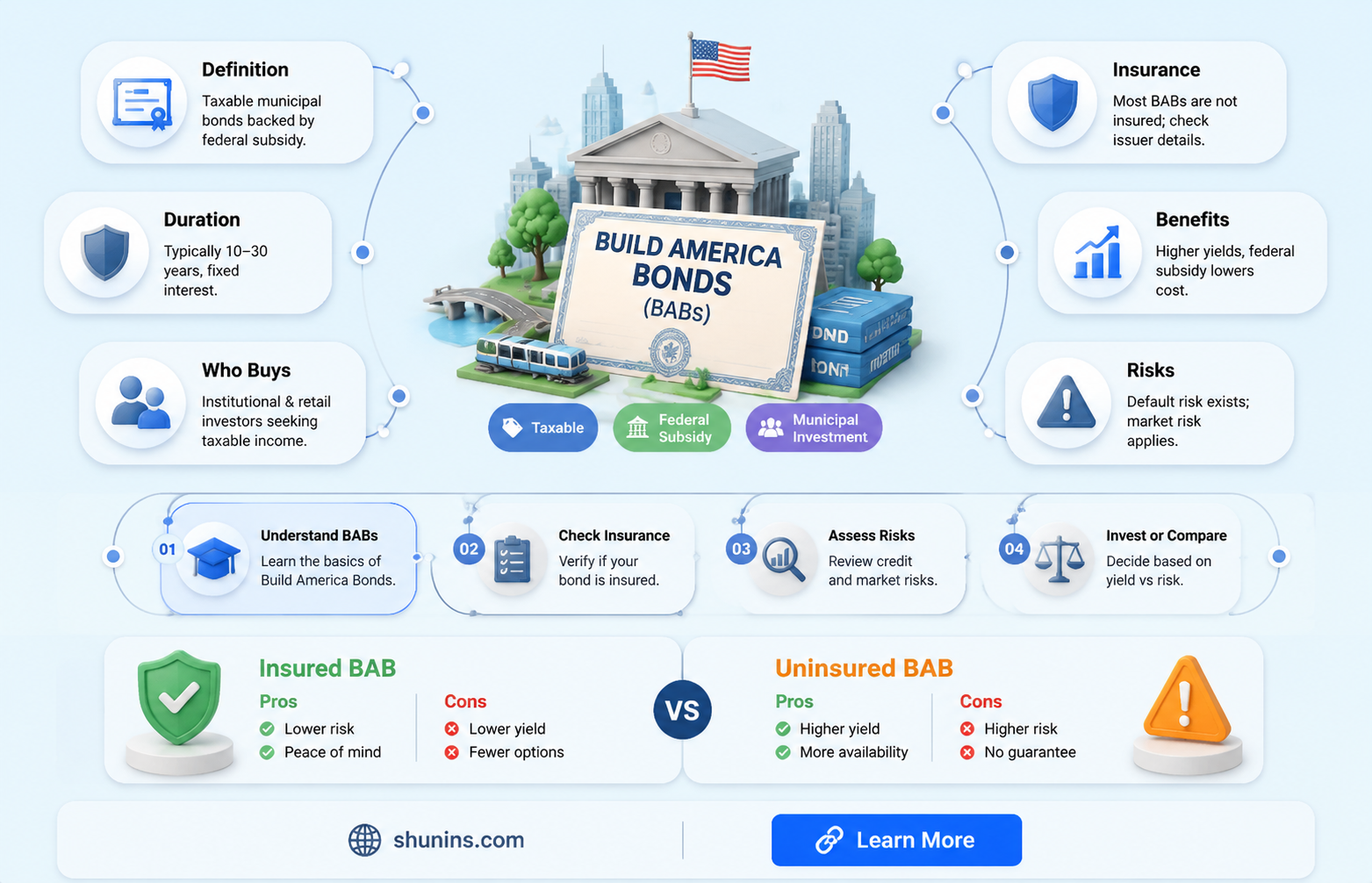

Build America Bonds (BABs) are taxable municipal bonds that were introduced by the US federal government in 2009 to stimulate the economy and subsidize state and local government projects. They are designed to reduce the cost of borrowing for eligible state and local government issuers and agencies, who receive a direct subsidy from the federal government of 35% of the BAB coupon. This subsidy does not constitute a federal guarantee of payment to the bondholder, and BABs carry the risk of default. However, historically, municipal default rates have been significantly lower than in the corporate bond market.

| Characteristics | Values |

|---|---|

| Type | Taxable municipal bonds |

| Purpose | Reduce the cost of borrowing for state and local government issuers and governmental agencies |

| Federal subsidies | 35% of the interest |

| Tax | Subject to federal income tax |

| Default risk | Lower than default rates in the corporate bond market |

| Largest buyers | Insurance companies, mutual funds, foreign central banks, and foreign commercial banks |

| Total issued | US$181 billion |

| Eligibility | Not eligible for private party issuers and 501 (c) (3) organizations |

| Maturity | Most BABs have maturities of more than 20 years |

| Interest rates | Competitive rates in the market |

Explore related products

What You'll Learn

![]()

Build America Bonds (BABs) are taxable municipal bonds

BABs are unique in that they are taxable, unlike traditional municipal bonds. This means that holders of BABs are subject to federal income tax on the interest they receive. However, those who live in the state where the bond was issued may be exempt from state and local taxes on the interest. It's important to note that BABs cannot be used for refunding working capital, private activities, or 501(c)(3) organizations.

There are two types of BABs: Direct Payment and Tax Credit. Direct Payment BABs provide a subsidy directly to the issuer, with the federal government subsidizing 35% of the interest they owe to investors. This reduces the effective cost of borrowing for issuers, allowing them to offer competitive rates in the market. Tax Credit BABs, on the other hand, provide a refundable tax credit directly to the bondholders. Both options effectively reduce the cost of borrowing for issuers compared to traditional taxable corporate bonds.

BABs are often issued by essential service providers, such as water and power agencies, which may ensure a reliable income stream to cover interest payments. Most BABs have been issued with maturities of more than 20 years. While all bonds carry the risk of default, municipal default rates have historically been significantly lower than in the corporate bond market.

Renter's Insurance: Individual or Household Coverage?

You may want to see also

Explore related products

![]()

BABs were created to stimulate the economy

Build America Bonds (BABs) were introduced in 2009 as part of President Obama's American Recovery and Reinvestment Act (ARRA). The Act authorizes state and local governments to issue taxable municipal bonds with federal subsidies to the issuer for a portion of the borrowing costs. These bonds were designed to stimulate the economy by encouraging investment in local areas.

BABs were created to address the reluctance of investors to invest in anything other than federal government bonds following the 2008 financial crisis. The federal government introduced BABs to ensure that local municipalities and counties could raise capital during the recession. They were designed to subsidize state and local government projects that might otherwise be unaffordable.

There are two types of BABs: "Direct Payment" and "Tax Credit". Direct Payment BABs provide a federal subsidy directly to the issuer, while Tax Credit BABs offer a refundable tax credit directly to the bondholder. The subsidy reduces the cost of borrowing for eligible state and local government issuers and agencies, allowing them to offer higher interest rates that attract institutional and individual investors. For example, California's $5.2 billion BAB issue in 2009 offered an interest rate of 7.4% to investors, of which the state only paid 4.8%, with the federal government subsidizing the rest.

BABs also provided a reliable income stream for essential service providers, such as water and power agencies, to cover interest payments. Most BABs were issued with maturities of over 20 years. The program was only open to new issue capital expenditure bonds issued before January 1, 2011, and could not be used for refinancing old debts or for refunding working capital, private activities, or 501(c)(3) organizations.

Irrevocable Life Insurance: Understanding the Unchangeable Policy

You may want to see also

Explore related products

![]()

BABs are issued by state, municipality, or county

Build America Bonds (BABs) are a form of taxable municipal bonds created under the American Recovery and Reinvestment Act of 2009. They are issued by state, municipality, or county to finance capital expenditures. The Act authorises state and local governments to issue taxable governmental bonds with federal subsidies for a portion of the borrowing costs. This subsidy does not constitute a federal guarantee of payment to the bondholder.

The purpose of BABs is to reduce the cost of borrowing for eligible state and local government issuers and governmental agencies. These entities receive a direct subsidy from the federal government of 35% of the BAB coupon, which enables them to offer higher interest rates that can attract institutional and individual investors.

There are two types of BABs: Direct Payment and Tax Credit. Direct Payment BABs provide the federal subsidy directly to the issuer, while Tax Credit BABs provide the federal subsidy as a refundable tax credit directly to the bondholder.

BABs cannot be used for refunding working capital, private activities, or 501(c)(3) organisations. They are often issued by essential service providers, such as water and power agencies, which may provide a reliable income stream to cover interest payments. Most BABs have been issued with maturities of more than 20 years.

Insurance Simplified: Am I Covered?

You may want to see also

Explore related products

![]()

BABs carry the risk of default

Build America Bonds (BABs) are a form of taxable municipal bonds. They were introduced by the federal government to help local municipalities and counties raise capital during the recession. BABs carry the risk of default, but municipal default rates have historically been significantly lower than in the corporate bond market. When defaults have occurred, the average recovery rate on municipal bonds has been higher than on defaulted corporate bonds.

BABs are designed to subsidize state and local government projects that would otherwise be unaffordable. They are also intended to stimulate the economy. There are two types of BABs: "Direct Payment" and "Tax Credit". Direct Payment BABs provide the federal subsidy directly to the issuer, while Tax Credit BABs provide the federal subsidy as a refundable tax credit directly to the bondholder.

The federal subsidy for Direct Payment BABs is a direct payment from the US Treasury to the bond issuers, equivalent to 35% of the interest they owe to investors. This lowers the effective cost of borrowing for issuers, allowing them to offer the bonds to investors at competitive rates. Tax Credit BABs offer a 35% federal subsidy of the interest paid through refundable tax credits, reducing the bondholder's tax liability. If the bondholder's tax liability is insufficient to use the entire credit, it can be carried forward to future years.

Issuers of BABs must meet the requirements imposed by the American Recovery and Reinvestment Act of 2009 to receive federal cash subsidy payments. Failure to do so may impair their ability to make scheduled interest payments. These securities may also carry extraordinary calls, making yield calculation unpredictable. Changes in tax treatment due to future legislation or the failure of a public issuer to meet tax law conditions may adversely impact the value of the bonds.

Vul Insurance: A Superior, Long-Term Investment Option

You may want to see also

Explore related products

![]()

BABs are not eligible for refinancing old debts

Build America Bonds (BABs) are a form of taxable municipal bonds that were created under the American Recovery and Reinvestment Act of 2009. These bonds are designed to subsidize state and local government projects that may otherwise be unaffordable, thereby stimulating the economy.

BABs carry the risk of default, although municipal default rates have historically been significantly lower than in the corporate bond market. When defaults occur, the average recovery rate on municipal bonds has been higher than on defaulted corporate bonds.

There are two types of BABs: Direct Payment and Tax Credit. Direct Payment BABs provide a federal subsidy directly to the issuer, while Tax Credit BABs offer the federal subsidy as a refundable tax credit to the bondholder. The federal government provides a direct subsidy of 35% of the BAB coupon to eligible state and local government issuers and agencies, enabling them to offer higher interest rates that attract investors.

Life Insurance While on Probation: Is It Possible?

You may want to see also