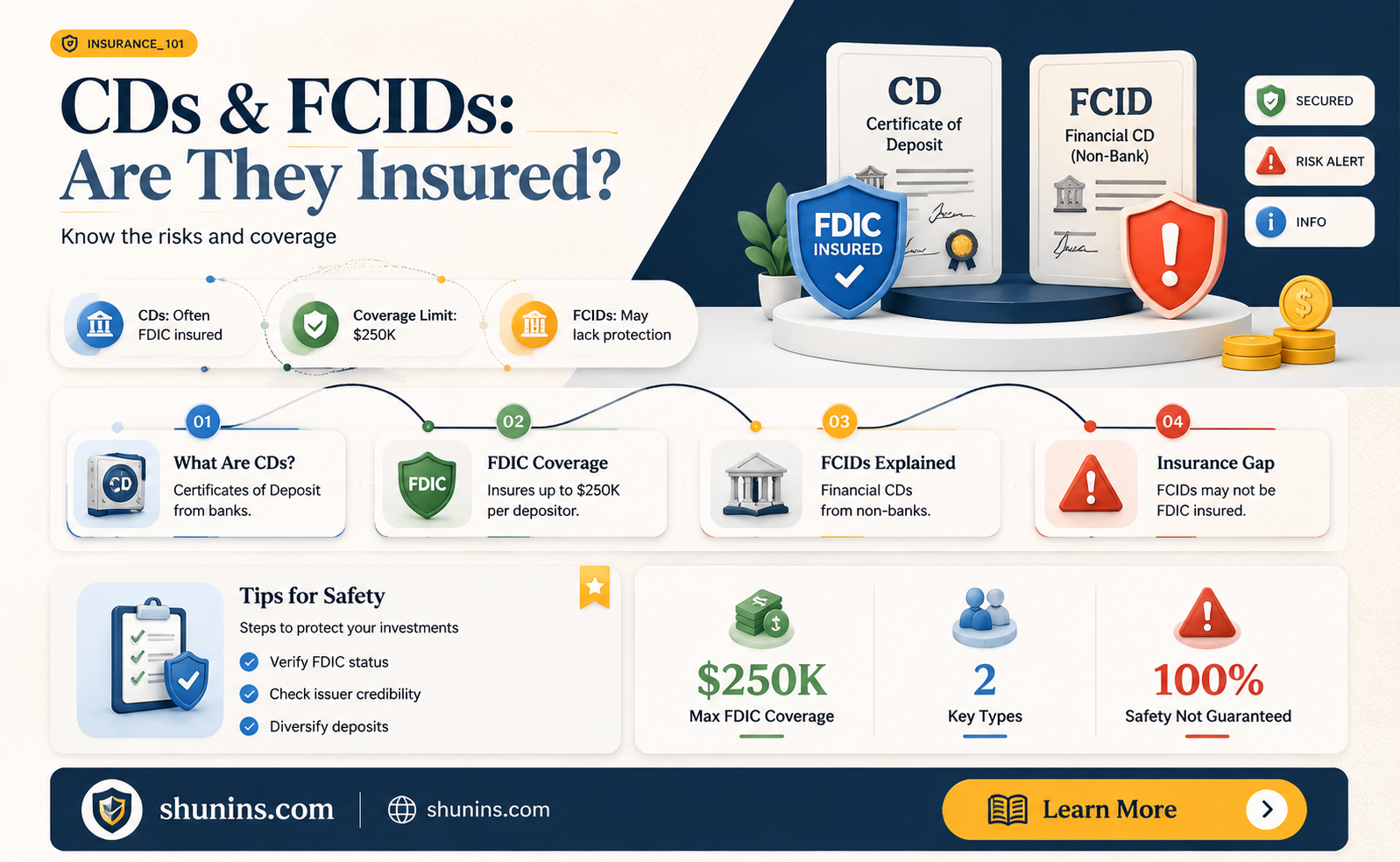

Certificates of deposit (CDs) are considered a safe way to save money because they are federally insured by the Federal Deposit Insurance Corporation (FDIC). The FDIC is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event of bank failure or liquidation. FDIC insurance covers up to $250,000 per depositor, per FDIC-insured bank, and per ownership category, including accrued interest. This limit can be expanded by opening CDs at different banks or purchasing brokered CDs from different issuing banks. While most CDs are FDIC-insured, it is important to understand the terms and conditions of your CD account to confirm that your funds are fully insured.

| Characteristics | Values |

|---|---|

| Are CDs FDIC insured? | Yes, most CDs are FDIC insured. |

| What is the insurance limit? | $250,000 per depositor, per FDIC-insured bank, per ownership category. |

| What does FDIC insurance cover? | FDIC insurance covers the principal plus any interest accrued or due to the depositor, through the date of default. |

| What happens in the event of a bank failure? | The FDIC steps in to guarantee the insured amount in existing deposit accounts. It first searches for another bank willing to assume the insured accounts. If that's not possible, it reimburses account holders according to insurance limits. |

| Are there any exceptions to FDIC insurance for CDs? | Yes, some types of CDs don't carry deposit insurance even when held at an FDIC member bank, such as investing money in foreign banks. |

| How to verify if a CD is FDIC insured? | Check for "Member FDIC" at the bottom of the bank's website. You can also use the FDIC's Electronic Deposit Insurance Estimator (EDIE) or call the FDIC toll-free at 1-877-ASK-FDIC (1-877-275-3342). |

Explore related products

What You'll Learn

![]()

CDs are federally insured

Certificates of deposit (CDs) are federally insured, making them a safe way to save money. The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event of an FDIC-insured bank or savings association failure. FDIC insurance is backed by the full faith and credit of the United States government.

FDIC deposit insurance covers bank customers if an FDIC-insured bank fails. This insurance is automatic for any deposit account opened at an FDIC-insured bank. The FDIC guarantees the insured amount in existing deposit accounts, up to a balance of $250,000 per depositor, per FDIC-insured bank, per ownership category. This limit includes the principal and any accrued interest. For example, if a customer had a CD account with a principal balance of $195,000 and $3,000 in accrued interest, the full $198,000 would be insured.

It is important to note that not all CDs are automatically insured. CDs purchased from a third-party broker instead of directly from an FDIC-insured bank may not be insured by the FDIC. Therefore, it is crucial to verify that the institution offering the CD is FDIC-insured and to understand the terms and conditions of the CD account.

In summary, CDs are federally insured, providing peace of mind for individuals looking to save their money with a guaranteed rate of return. By understanding the FDIC insurance coverage and choosing CDs offered by FDIC-insured institutions, individuals can ensure their deposits are protected up to the specified limits.

Best Life Insurance: Choosing the Right Coverage

You may want to see also

Explore related products

![]()

FDIC insurance covers up to $250,000 per depositor

Certificates of deposit (CDs) are considered a safe way to save money because they are federally insured by the Federal Deposit Insurance Corporation (FDIC). This means that, in the rare event of a bank failure, the FDIC steps in to guarantee insured amounts in existing deposit accounts, up to a limit of $250,000 per depositor.

The $250,000 limit applies per depositor, per FDIC-insured bank, per ownership category. This means that a single-owner account would be fully insured up to $250,000, while a joint account with two owners would be insured up to $500,000. The limit includes the principal and any accrued interest. For example, if a customer had a CD account with a principal balance of $195,000 and $3,000 in accrued interest, the full $198,000 would be insured.

It is important to note that not all CDs are automatically insured. While many CD accounts come with automatic FDIC coverage, some types of CDs do not carry deposit insurance, even when held at an FDIC-member bank. For example, uninsured CDs may include those that involve investing money in foreign banks. Additionally, if you purchase a CD from a third-party broker, rather than directly from an FDIC-insured bank, you will need to rely on the broker to place your funds into a CD at an FDIC-insured bank for your money to be insured.

To verify that your CD is FDIC-insured, you can use the FDIC's Electronic Deposit Insurance Estimator (EDIE) or contact the FDIC directly. By understanding the terms and conditions of your CD account and confirming that it is FDIC-insured, you can ensure that your savings are protected.

Irrevocable Beneficiary: Life Insurance Policy's Ultimate Decision

You may want to see also

Explore related products

![]()

The FDIC responds in the rare case of bank failure

Bank failures are rare, but they do happen. When they do, the FDIC steps in to guarantee insured amounts in existing deposit accounts. The FDIC first searches for another bank willing to assume the insured accounts. If it is not possible to sell or transfer the deposits, the FDIC reimburses account holders according to insurance limits, which amount to a $250,000 balance per depositor per member bank per account ownership category. This includes any interest accrued or due to the depositor.

For example, if a customer had a CD account in her name with a principal balance of $195,000 and $3,000 in accrued interest, the full $198,000 would be insured. The FDIC typically pays insurance within a few days after a bank closes, usually on the next business day. They do this by either providing each depositor with a new account at another insured bank for an amount equal to the insured balance of their account at the failed bank or issuing a cheque to each depositor for the insured balance.

In the case of loans, the FDIC offers some or all of the failing bank's assets for sale to healthy financial institutions before the bank's failure. Loans not sold at the time of the bank's closing are packaged and offered for sale to the broader financial market within a few months of the bank's failure. The FDIC also undertakes the servicing responsibilities previously held by the failed bank until the loan is sold. The FDIC encourages borrowers to seek a new lender and may offer an incentive to refinance by offsetting some or all of the associated closing costs.

The FDIC also makes representatives available to meet with loan customers within one business day after the bank failure. Customers can reach FDIC staff by calling the failed bank's telephone number, and the FDIC also establishes a temporary, specific 1-800 Customer Service line for every failed bank.

Roth IRA Insurance: What's Covered and What's Not

You may want to see also

![]()

CDs offer a higher rate of interest than savings accounts

Certificates of Deposit (CDs) are a type of savings account that generally offers a higher interest rate than traditional savings accounts. CDs have a fixed interest rate, which means that the rate is locked in when you open the account and won't change during the account's term. This provides a predictable return on your investment. The trade-off is that you agree to keep your money in the CD for a set amount of time, typically ranging from a few months to several years. If you withdraw your funds before the maturity date, you may have to pay a penalty.

The higher interest rates offered by CDs can make them an attractive option for those looking to grow their savings over time. However, it's important to consider the limited access to your cash while the CD is active. CDs are best suited for longer-term savings goals, as they provide a low-risk way to keep your money growing without the volatility associated with investing in the stock market.

On the other hand, high-yield savings accounts also offer higher interest rates than traditional savings accounts. These accounts are typically offered by online banks and credit unions, which have lower overhead costs and can pass those savings on to customers in the form of higher interest rates. High-yield savings accounts provide flexibility, as they usually don't restrict access to your funds for a specific period. However, there may be withdrawal limits on the number of transactions you can make each month.

Both CDs and high-yield savings accounts are considered low-risk options. They are FDIC-insured, which means that your funds are protected up to $250,000 per depositor, per insured bank. This insurance provides peace of mind, as it guarantees that your money is safe even in the rare event of a bank failure.

When deciding between a CD and a high-yield savings account, it's important to consider your financial goals and needs. CDs are ideal for long-term savings, providing higher interest rates and guaranteed returns. High-yield savings accounts offer flexibility and easy access to funds, making them suitable for those who may need to withdraw money frequently. By understanding the features and benefits of each option, you can make an informed decision that aligns with your financial objectives.

General vs Life Assurance: What's the Main Difference?

You may want to see also

![]()

CDs are a safe option for short-term savings goals

Certificates of deposit (CDs) are considered a safe option for short-term savings goals. They are insured by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA), which guarantees your money up to a limit of $250,000 per depositor, per insured bank, and ownership category. This means that even if your bank fails, your money is still protected.

CDs are a stable and conservative investment option, offering a fixed interest rate that is usually higher than regular savings accounts. The trade-off is that you agree to keep your money in the CD for a set period, typically three months to five years. This makes CDs ideal for short-term savings goals, as you can choose a term that aligns with your financial plans.

While CDs provide a lower opportunity for growth compared to stocks and bonds, they eliminate the risk of market downturns. This makes them a safer choice if you are looking for consistent returns. Additionally, CDs can help you save by deterring you from spending. Since withdrawing funds before the maturity date often incurs a penalty, you are encouraged to leave your money untouched, allowing your savings to grow.

It is important to note that not all CDs are automatically insured. When considering a CD, ensure that you are working with an FDIC-insured bank or an NCUA-insured credit union. Understanding the terms and conditions of your CD account will help you make an informed decision about your short-term savings goals.

Life Insurance and Taxes: Saving Strategies Revealed

You may want to see also

Frequently asked questions

Yes, most CDs are FDIC insured.

Deposits are insured up to at least $250,000 per depositor, per FDIC-insured bank, per ownership category. This includes the principal and any accrued interest.

You can call the FDIC at 1-877-275-3342 to speak to a deposit insurance specialist to ensure your funds are fully insured. You can also use the FDIC's Electronic Deposit Insurance Estimator.

Yes, some types of CDs do not carry deposit insurance even when held at an FDIC-member bank. For example, if you invest money in foreign banks through a CD, it may not be FDIC insured.