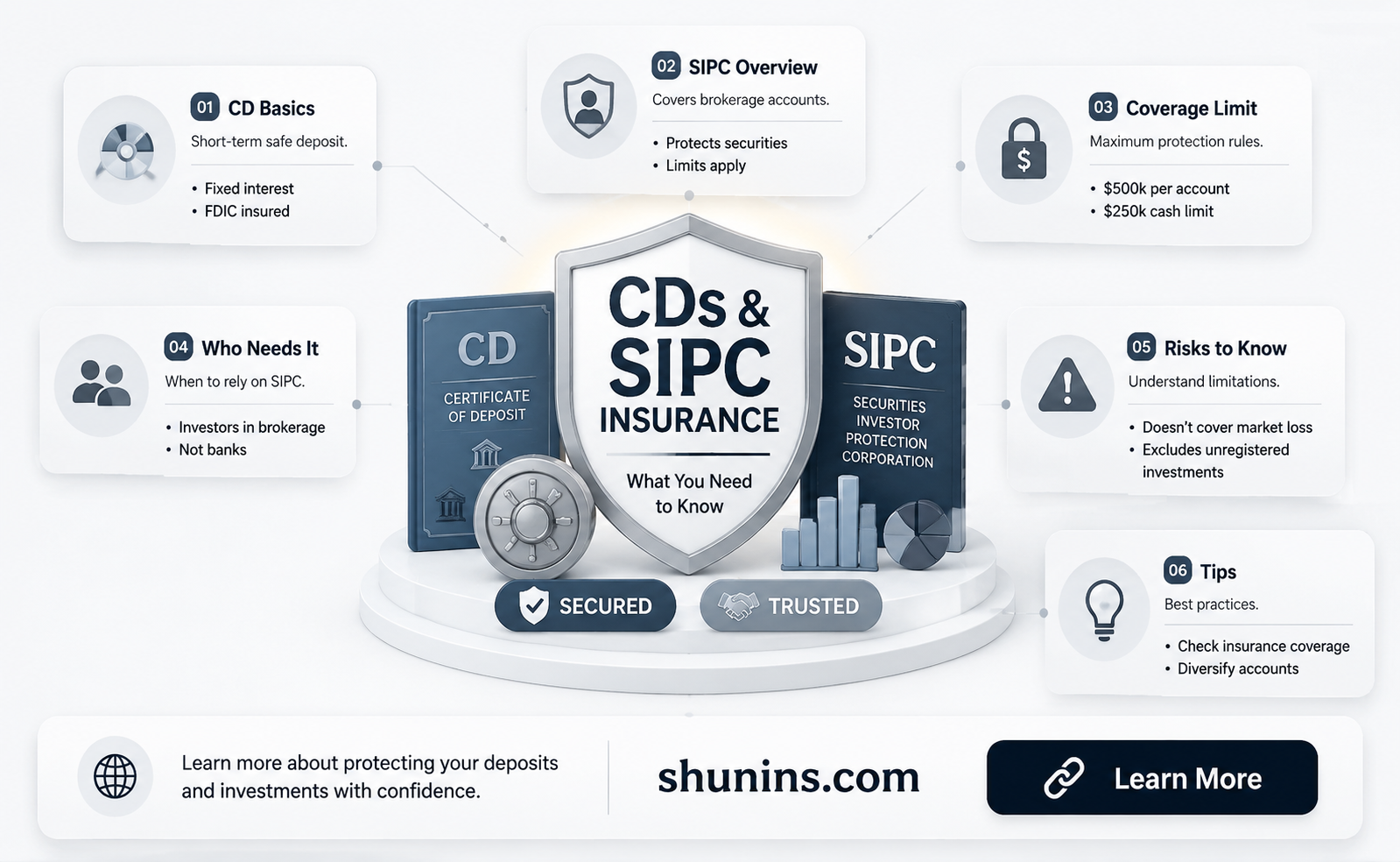

The Securities Investor Protection Corporation (SIPC) is a federally mandated, private, nonprofit organisation that insures investors against the loss of cash and securities in the event of their brokerage firm failing financially. SIPC insurance covers investors for up to \$500,000 in securities and up to \$250,000 in uninvested cash. While CDs (certificates of deposit) are protected by SIPC insurance, it is important to note that SIPC insurance does not cover all types of assets and there are limitations to the protection it provides.

Explore related products

What You'll Learn

![]()

SIPC insurance covers money and securities in brokerage accounts

SIPC insurance, or the Securities Investor Protection Corporation, is a nonprofit membership corporation created by the US Congress in 1970. It is not the same as FDIC insurance, which covers money in bank accounts. Instead, SIPC insurance covers money and securities in brokerage accounts.

SIPC insurance covers investors for up to up to $500,000 in securities, with a $250,000 limit for cash balances. However, investors can be covered for more than $500,000 depending on how the accounts are held, or what SIPC calls "separate capacities". For example, if an investor owns a traditional IRA and a Roth IRA, SIPC insures those separately, providing up to $1 million in coverage for the two accounts.

SIPC insurance covers money market mutual funds, stocks, bonds, Treasury securities, certificates of deposit, mutual funds, and certain other investments as "securities". However, it does not cover commodity futures contracts, foreign exchange trades, investment contracts, fixed annuity contracts, or digital asset securities that are not registered with the US Securities and Exchange Commission.

SIPC steps in when a brokerage firm fails financially and assets are missing from customer accounts. It works to restore investors' cash and securities, recovering billions of dollars for investors over the years.

Life Insurance Termination: What You Need to Know

You may want to see also

Explore related products

![]()

FDIC insurance covers money in bank accounts

SIPC insurance is not the same as FDIC insurance. SIPC insurance covers money and securities in brokerage accounts, whereas FDIC insurance covers money in bank accounts. FDIC insurance protects your money in deposit accounts at FDIC-insured banks in the event of a bank failure. FDIC deposit insurance covers $250,000 per depositor, per FDIC-insured bank, for each account ownership category.

FDIC deposit insurance covers money you hold at an FDIC-insured bank in traditional deposit accounts like certificates of deposit (CDs). Coverage is automatic when you open one of these accounts at an FDIC-insured bank. FDIC insurance covers money in bank accounts, protecting your money in the event of a bank failure. Since the FDIC was founded in 1933, no depositor has lost any FDIC-insured funds.

The FDIC helps maintain stability and public confidence in the US financial system by insuring deposits to at least $250,000 per depositor, per ownership category at each FDIC-insured bank. The FDIC maintains the Deposit Insurance Fund (DIF), which insures deposits and protects depositors of FDIC-insured banks. The DIF is backed by the full faith and credit of the US government and is funded by assessments (insurance premiums) that FDIC-insured institutions pay, as well as interest earned on funds invested in US government obligations.

The FDIC deposit insurance covers various types of accounts, including single ownership accounts, joint ownership accounts, retirement accounts, employee benefit plan accounts, and irrevocable trusts. For single ownership accounts, all accounts owned by the same person at the same bank are added together and insured up to $250,000. If you have a single ownership account and a joint ownership account at the same bank, you will be insured for up to $250,000 for your single ownership account deposits and separately for your ownership interest in the joint account.

In contrast to FDIC insurance, SIPC insurance protects against the loss of cash and securities held by a customer at a financially troubled SIPC-member brokerage firm. The limit of SIPC protection is typically $500,000 per account per brokerage firm, including up to $250,000 for cash. SIPC steps in when a brokerage firm fails financially and works to restore investors' cash and securities.

Life Insurance: Suicide and Policy Payouts Explained

You may want to see also

![]()

SIPC insurance covers investors for up to \$500,000 in securities

The Securities Investor Protection Corporation (SIPC) is a federally mandated, private, nonprofit organisation. It was created as part of the Securities Investor Protection Act (SIPA) of 1970, which aimed to protect investors from brokerages becoming insolvent.

SIPC insurance covers investors for up to $500,000 in securities and up to $250,000 in uninvested cash. This limit applies per account per brokerage firm. SIPC insurance covers specific types of investments as securities, including stocks, bonds, Treasury securities, certificates of deposit, mutual funds, and money market mutual funds.

It's important to note that SIPC insurance does not cover all types of assets. For example, it does not protect commodity futures contracts unless they are held in a special portfolio margining account. It also does not cover investment contracts such as limited partnerships or fixed annuity contracts that are not registered with the U.S. Securities and Exchange Commission.

SIPC insurance only comes into play when the SIPC intervenes, which happens when it receives a referral from regulatory agencies such as the Securities and Exchange Commission (SEC) or the Financial Industry Regulatory Agency (FINRA). It is designed to protect investors when their brokerage firm fails financially and works to restore investors' cash and securities.

In some cases, investors may be covered for more than $500,000 if they have multiple accounts of different types, such as a traditional individual retirement account (IRA) and a Roth IRA at the same brokerage. In this case, the SIPC will insure them separately, providing up to $1 million in coverage across the two accounts.

Sun Life and Minnesota Life Insurance: What's the Difference?

You may want to see also

![]()

SIPC covers up to \$250,000 in uninvested cash

The Securities Investor Protection Corporation (SIPC) is a federally mandated, private, nonprofit organisation that was created as part of the Securities Investor Protection Act (SIPA) of 1970. It shields investors from brokerages becoming insolvent by recovering missing cash or securities if a brokerage firm goes out of business.

SIPC insurance covers investors for up to $500,000 in securities, with a limit of $250,000 for cash balances. This means that if you have $500,000 in securities and $250,000 in cash, your entire amount may not be covered. However, there are circumstances in which investors are covered for more than $500,000. This occurs when investors have multiple accounts of different types, such as a traditional individual retirement account (IRA) and a Roth IRA at the same brokerage, in which case the SIPC will insure them separately, providing a total of up to $1 million in protection.

It is important to note that SIPC insurance does not protect against all types of losses. For example, it does not cover investment losses or claims against bad advice. Additionally, cash held in connection with a commodities trade or foreign exchange trades is not protected by SIPC.

In summary, while SIPC provides significant protection for investors, it is important to understand the limits and exclusions of the coverage. Investors should carefully review their specific situation and consider additional layers of protection if needed.

Life Insurance: A Gift of Lasting Security

You may want to see also

![]()

SIPC does not protect against investment losses

Certificates of deposit (CDs) are eligible for SIPC protection and are subject to the $500,000 protection limit applicable to securities. However, SIPC does not protect against the risk that CDs will decline in value. This means that SIPC does not protect against investment losses.

SIPC insurance is not the same as FDIC insurance. SIPC insurance covers money and securities in brokerage accounts, whereas FDIC insurance covers money in bank accounts. SIPC insurance is provided by a non-profit corporation that has been protecting investors for 50 years. It works to restore investors' cash and securities when their brokerage firm fails.

SIPC steps in when a brokerage firm fails financially and assets are missing from customer accounts. It protects customer assets when a SIPC-member brokerage firm fails financially. SIPC has recovered billions of dollars for investors.

SIPC protects cash held by the broker for customers in connection with the customers' purchase or sale of securities, whether the cash is in US dollars or denominated in non-US dollar currency. It also protects stocks, bonds, Treasury securities, certificates of deposit, mutual funds, money market mutual funds, and certain other investments as "securities".

However, it is important to note that SIPC does not protect against investment losses. It does not provide protection for investment contracts not registered with the SEC. SIPC also does not protect against the decline in value of securities or CDs. While SIPC provides brokerage account insurance of up to $500,000 if assets and cash go missing, it does not cover investment losses or claims against bad advice.

In summary, SIPC insurance provides protection for investors in the event of brokerage firm failure, but it does not cover investment losses or declines in the market value of securities or CDs.

Life Insurance: Choosing the Right Cover for Peace of Mind

You may want to see also

Frequently asked questions

SIPC insurance is provided by the Securities Investor Protection Corporation (SIPC), a federally mandated, private, nonprofit organisation. It was created as part of the Securities Investor Protection Act (SIPA) of 1970, which aimed to protect investors from brokerages becoming insolvent.

SIPC insurance covers investors for up to $500,000 in securities and up to $250,000 in uninvested cash per account. It protects customers of SIPC-member broker-dealers if the firm fails financially.

CDs (Certificates of Deposit) are protected under SIPC insurance as "securities".

SIPC insurance does not cover commodity futures contracts (unless held in a special portfolio-margining account), foreign exchange trades, investment contracts (such as limited partnerships), and fixed annuity contracts not registered with the U.S. Securities and Exchange Commission. It also does not protect against investment losses or claims of bad advice.

SIPC insurance covers money and securities in brokerage accounts, whereas FDIC insurance covers money in bank accounts. SIPC insurance does not provide blanket coverage like FDIC insurance, which offers a standard deposit insurance amount of $250,000 per depositor, per insured bank, for each account ownership category at a bank.