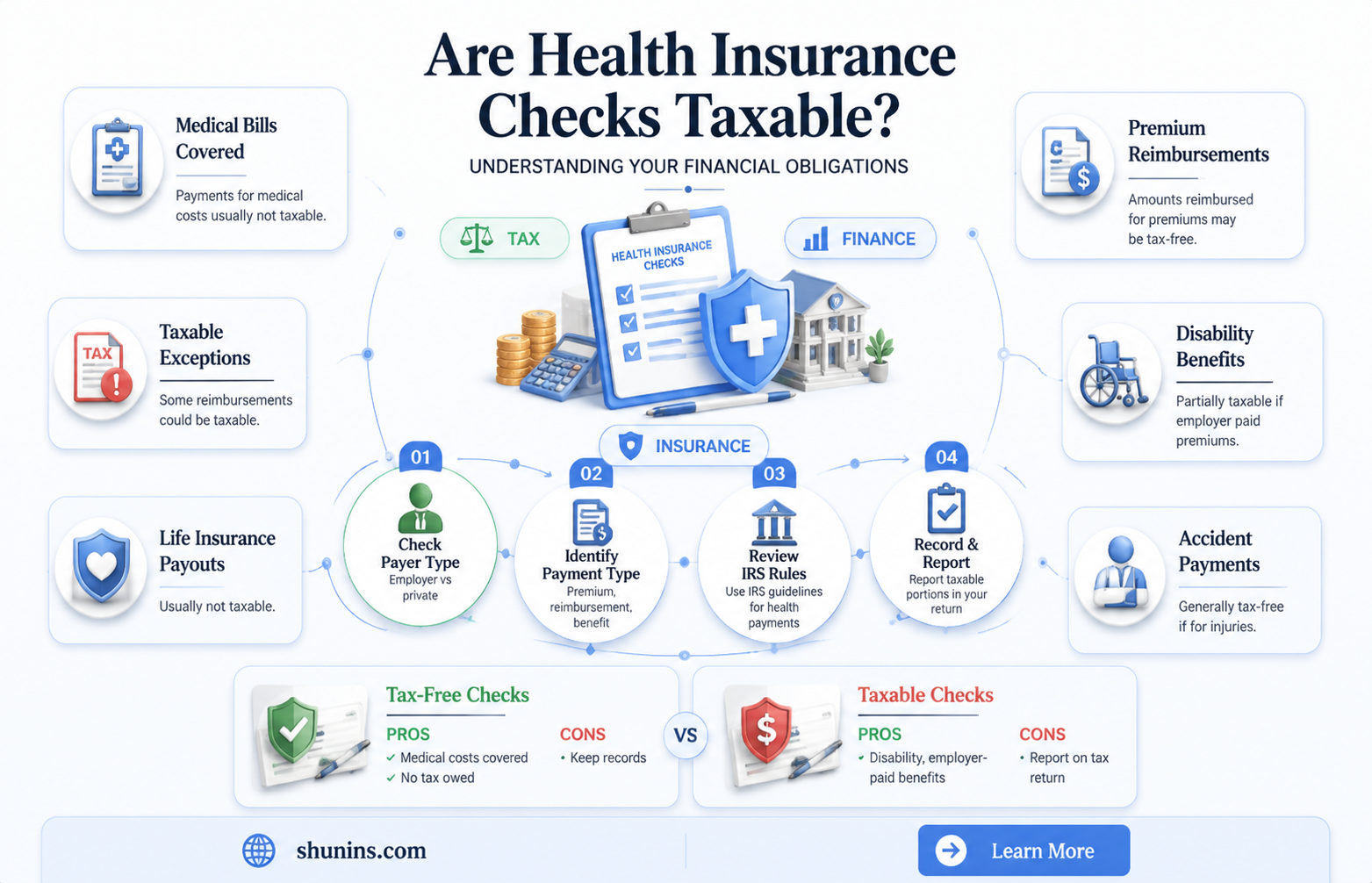

When considering whether checks received from a health insurance company are taxable, it’s essential to understand the context in which these payments are made. Generally, reimbursements for medical expenses paid by a health insurance company are not taxable if they are for qualified medical expenses and were not previously deducted on your tax return. However, if the payment is for non-medical reasons, such as a settlement or compensation unrelated to medical care, it may be subject to taxation. Additionally, if you received advanced premium tax credits for health insurance purchased through a marketplace and the amount exceeds what you were eligible for, you might owe taxes on the difference. Always consult the IRS guidelines or a tax professional to determine the taxability of specific insurance payments based on your individual circumstances.

| Characteristics | Values |

|---|---|

| Taxability of Health Insurance Checks | Depends on the type of payment and circumstances. |

| Premium Refunds | Generally not taxable if premiums were paid with after-tax dollars. |

| Claim Reimbursements | Not taxable if the original expenses were paid with after-tax dollars. |

| Disability Benefits | Taxable if premiums were paid by employer or with pre-tax dollars. |

| Health Savings Account (HSA) Distributions | Tax-free if used for qualified medical expenses. |

| Flexible Spending Account (FSA) Reimbursements | Tax-free for qualified medical expenses. |

| Insurance Settlements | May be taxable if compensating for lost income or non-medical damages. |

| IRS Guidelines | Follow IRS Publication 502 for detailed rules on medical expense deductions. |

| Employer-Sponsored Plans | Tax treatment varies based on plan type (e.g., self-insured vs. insured). |

| Individual Health Insurance Plans | Refunds or reimbursements typically not taxable if paid with after-tax funds. |

| State-Specific Rules | Some states may have additional tax implications; check local regulations. |

| Reporting Requirements | Taxable amounts must be reported on Form 1040; non-taxable amounts usually not reported. |

Explore related products

What You'll Learn

![]()

Taxability of Reimbursement Checks

Reimbursement checks from health insurance companies often leave recipients unsure about their tax implications. The key to understanding taxability lies in the nature of the reimbursement itself. Generally, if the reimbursement covers medical expenses you’ve already paid for with after-tax dollars, it’s not taxable. For instance, if you paid a $500 medical bill out of pocket and your insurer later reimburses you, that $500 is typically tax-free because you’ve already been taxed on the income used to pay the expense. However, if the reimbursement exceeds the amount you spent or covers expenses not qualified as medical, it may become taxable income.

Consider the role of health savings accounts (HSAs) and flexible spending accounts (FSAs) in this context. Reimbursements from these accounts for qualified medical expenses are usually tax-free, as the funds were initially contributed pre-tax. For example, if you use your HSA to pay for a $200 prescription and later receive a reimbursement, that amount remains non-taxable. Conversely, if you’re reimbursed for non-qualified expenses—like cosmetic procedures not deemed medically necessary—the reimbursement could be taxable and subject to penalties. Always verify the eligibility of expenses through IRS guidelines to avoid unexpected tax liabilities.

A common pitfall arises when reimbursements are received for expenses claimed as itemized deductions in prior tax years. If you deducted $1,000 in medical expenses on your taxes and later receive a reimbursement for those same expenses, you must report the reimbursement as income. This prevents double-dipping on tax benefits. For instance, if you deducted medical expenses that pushed you over the 7.5% adjusted gross income (AGI) threshold for itemized deductions, a subsequent reimbursement would need to be declared to offset the earlier deduction.

To navigate this complexity, maintain detailed records of all medical expenses, reimbursements, and deductions. Use IRS Publication 502 as a reference for qualified medical expenses and consult a tax professional if you’re uncertain. For example, if you’re reimbursed $800 for a medical procedure but only spent $600, the $200 excess is likely taxable. Proactive documentation and awareness of these rules can save you from audits or penalties while ensuring compliance with tax laws.

Christian Medical Insurance: Is It a Good Option?

You may want to see also

Explore related products

![]()

Pre-Tax vs. Post-Tax Premiums

Health insurance premiums can be paid with pre-tax or post-tax dollars, and this distinction significantly impacts your taxable income and overall financial picture. Pre-tax premiums are paid with money that hasn’t been subject to federal income tax, Social Security, or Medicare taxes, effectively lowering your taxable income. For example, if you earn $60,000 annually and contribute $3,000 pre-tax to your health insurance premium, your taxable income drops to $57,000. This reduces your tax liability and increases your take-home pay. In contrast, post-tax premiums are paid with money that has already been taxed, offering no immediate reduction in taxable income. Understanding this difference is crucial for maximizing tax efficiency and managing healthcare costs effectively.

One common way to pay pre-tax premiums is through employer-sponsored plans, such as those offered under a Section 125 cafeteria plan or a Flexible Spending Account (FSA). These plans allow employees to allocate a portion of their salary to health insurance premiums before taxes are deducted. For instance, if your employer offers a health insurance plan with a monthly premium of $500, contributing this amount pre-tax could save you hundreds of dollars annually, depending on your tax bracket. Self-employed individuals can also pay pre-tax premiums by deducting health insurance costs from their taxable income, provided they meet specific IRS criteria, such as not being eligible for an employer-sponsored plan.

Post-tax premiums, while less advantageous from a tax perspective, are often unavoidable for certain individuals. For example, if you purchase health insurance through a state or federal marketplace and don’t qualify for a premium tax credit, your payments are typically made with post-tax dollars. However, there’s a silver lining: you may be eligible for a tax deduction for medical expenses, including premiums, if your total medical expenses exceed 7.5% of your adjusted gross income (AGI) as of 2023. This deduction can offset some of the tax burden, though it’s less straightforward than pre-tax contributions.

Choosing between pre-tax and post-tax premiums requires careful consideration of your financial situation and tax status. If you’re employed and your employer offers pre-tax options, it’s almost always beneficial to take advantage of them. For self-employed individuals, consulting a tax professional can help ensure you’re maximizing deductions while staying compliant with IRS rules. For those paying post-tax premiums, tracking medical expenses throughout the year can help determine eligibility for deductions at tax time. Ultimately, the goal is to minimize out-of-pocket costs while optimizing your tax strategy, ensuring that your health insurance works as efficiently as possible for your financial health.

Domestic Partner Qualifications for Medical Insurance Coverage

You may want to see also

Explore related products

![]()

IRS Rules on Insurance Payments

Health insurance payments, including checks from insurance companies, are generally not taxable if they are for medical care or qualify under specific IRS guidelines. The Internal Revenue Service (IRS) treats these payments as reimbursements for expenses rather than income, provided they meet certain criteria. For instance, if you receive a check from your health insurance company to cover medical bills, it is typically tax-free because it is considered a return of premiums you or your employer paid, which were initially excluded from your taxable income. However, exceptions exist, and understanding these rules is crucial to avoid unexpected tax liabilities.

One key rule is that insurance payments are tax-free if they are for personal physical injuries or sickness and do not exceed the amount of medical expenses you incurred. For example, if your medical bills total $5,000 and your insurance company pays you $5,000, the payment is not taxable. However, if the insurance payment exceeds your actual expenses, the excess may be taxable as income. This often occurs in cases of punitive damages or compensation for lost wages, which are treated differently under IRS rules. Always document your medical expenses to substantiate the tax-free nature of the payment.

Another important consideration is the source of the insurance premiums. If your health insurance premiums were paid with pre-tax dollars (e.g., through a workplace plan like a Flexible Spending Account or Health Savings Account), any reimbursements or payments from the insurance company are generally tax-free. Conversely, if you paid premiums with after-tax dollars, the payments may still be tax-free if they qualify under the medical expense exclusion. However, if the payments are for non-medical purposes, such as compensation for emotional distress, they may be taxable.

For those receiving disability insurance payments, the tax treatment depends on who paid the premiums. If your employer paid the premiums and did not include the cost in your taxable income, the disability payments are taxable. If you paid the premiums with after-tax dollars, the benefits are typically tax-free. This distinction highlights the importance of reviewing your insurance policy and payroll records to determine the tax implications of disability payments.

In summary, while most checks from health insurance companies are not taxable, the IRS rules hinge on the purpose of the payment, the amount relative to expenses, and the source of the premiums. To ensure compliance, keep detailed records of medical expenses, understand the terms of your insurance policy, and consult a tax professional if you receive payments that seem ambiguous. Proactive attention to these details can prevent costly mistakes and ensure you accurately report your tax obligations.

Medicaid Insurance Options in Oklahoma: What's Covered?

You may want to see also

Explore related products

![]()

Taxable vs. Nontaxable Benefits

Health insurance checks can serve as a financial lifeline, but their tax implications aren’t always clear. Understanding whether these payments are taxable hinges on the nature of the benefit and the circumstances under which it’s received. Generally, health insurance benefits fall into two categories: taxable and nontaxable. Nontaxable benefits typically include reimbursements for qualified medical expenses, such as doctor visits, prescriptions, or hospital stays, as long as they’re paid through a plan like a Health Savings Account (HSA) or Flexible Spending Account (FSA). Taxable benefits, on the other hand, often arise when payments exceed actual medical costs or are provided as taxable income, such as certain disability benefits or payments not tied to specific medical expenses.

Consider a scenario where an individual receives a $5,000 check from their health insurance company after a hospitalization. If this amount directly covers medical bills and is paid through a qualified plan, it’s likely nontaxable. However, if the insurer pays the individual directly without specifying it’s for medical expenses, or if the payment exceeds the actual costs incurred, the excess could be taxable. For example, if the medical bills totaled $4,000, the remaining $1,000 might be considered taxable income. This distinction underscores the importance of reviewing the purpose and structure of the payment.

Employer-provided health insurance benefits further complicate this landscape. Premiums paid by employers for group health plans are typically nontaxable to employees, as they’re excluded from gross income under IRS rules. However, certain benefits, like payments from a Health Reimbursement Arrangement (HRA) that aren’t tied to specific expenses, may be taxable. For instance, if an employer provides a taxable HRA, any reimbursements received could increase the employee’s taxable income. Self-employed individuals face a different set of rules: they can deduct health insurance premiums, but reimbursements from plans like HRAs or FSAs may still be taxable if not properly structured.

Practical tips can help navigate these complexities. First, always request itemized statements from insurers detailing how payments are allocated to medical expenses. Second, consult IRS Publication 502 for a comprehensive list of qualified medical expenses that are nontaxable when reimbursed. Third, if you’re self-employed, ensure your health insurance plan complies with IRS guidelines to maximize deductions and minimize taxable income. Finally, consider consulting a tax professional when dealing with large or ambiguous payments, especially those exceeding actual medical costs.

In summary, the taxability of health insurance checks depends on their purpose, source, and structure. Nontaxable benefits are typically tied to qualified medical expenses and paid through designated plans, while taxable benefits often arise from excess payments or non-medical reimbursements. By understanding these distinctions and taking proactive steps, individuals can avoid unexpected tax liabilities and make the most of their health insurance benefits.

Understanding Non-Admitted Insurance: Key Regulations and Requirements Explained

You may want to see also

Explore related products

$6.95 $8.95

![]()

Reporting Insurance Payments on Taxes

Health insurance payments can significantly impact your tax situation, but not all checks from a health insurance company are taxable. Understanding which payments to report and how to do so accurately is crucial for compliance and maximizing your financial benefits.

Generally, reimbursements for medical expenses you’ve already paid out-of-pocket are not taxable, as they’re considered a return of your own funds. However, payments made directly to you that exceed your actual medical expenses or are not used for qualified medical purposes may be taxable as income.

Identifying Taxable Insurance Payments

The key distinction lies in the purpose of the payment. If your health insurance company sends you a check to cover a specific medical expense you’ve incurred, and you use the funds for that purpose, it’s typically not taxable. This includes reimbursements for doctor visits, prescriptions, hospital stays, and other qualified medical expenses outlined by the IRS.

However, if you receive a lump sum payment from your insurance company that isn’t tied to a specific expense, or if the payment exceeds your actual out-of-pocket costs, it may be considered taxable income. This could include disability payments, certain types of settlements, or payments made under a health insurance policy that provides cash benefits rather than direct reimbursement for medical expenses.

Reporting Requirements

Taxable insurance payments should be reported on your federal income tax return. The specific line item depends on the nature of the payment. For example:

- Disability Payments: Generally reported as wages on Form 1040, line 1.

- Lump-Sum Payments: May be reported as "Other Income" on Schedule 1 (Form 1040).

- Excess Reimbursements: If you received a reimbursement exceeding your actual expenses, the excess may be reported as "Other Income" on Schedule 1 (Form 1040).

Documentation is Key

Maintaining thorough records is essential. Keep copies of all insurance payments received, along with documentation of the corresponding medical expenses. This includes receipts, explanations of benefits (EOBs), and any other relevant paperwork. This documentation will be crucial if the IRS requests verification of your reported income or deductions.

Consulting a Tax Professional

Given the complexities surrounding taxable insurance payments, consulting a qualified tax professional is highly recommended. They can provide personalized guidance based on your specific circumstances, ensuring accurate reporting and minimizing your tax liability. Remember, proper reporting of insurance payments is not just about compliance; it’s about protecting yourself from potential penalties and ensuring you receive all the tax benefits you’re entitled to.

Indiana Insurance for Kids: Application Process Simplified

You may want to see also

Frequently asked questions

No, checks from a health insurance company are not always taxable. They are typically tax-free if they are reimbursements for medical expenses that were paid with after-tax dollars.

A check from a health insurance company may be taxable if it represents a refund of premiums paid with pre-tax dollars (e.g., through a Flexible Spending Account or Health Savings Account) or if it exceeds the amount of eligible medical expenses.

No, tax-free reimbursements from health insurance for eligible medical expenses do not need to be reported on your tax return.

Disability payments from a health insurance company may be taxable if the premiums were paid with pre-tax dollars. If the premiums were paid with after-tax dollars, the benefits are generally tax-free.