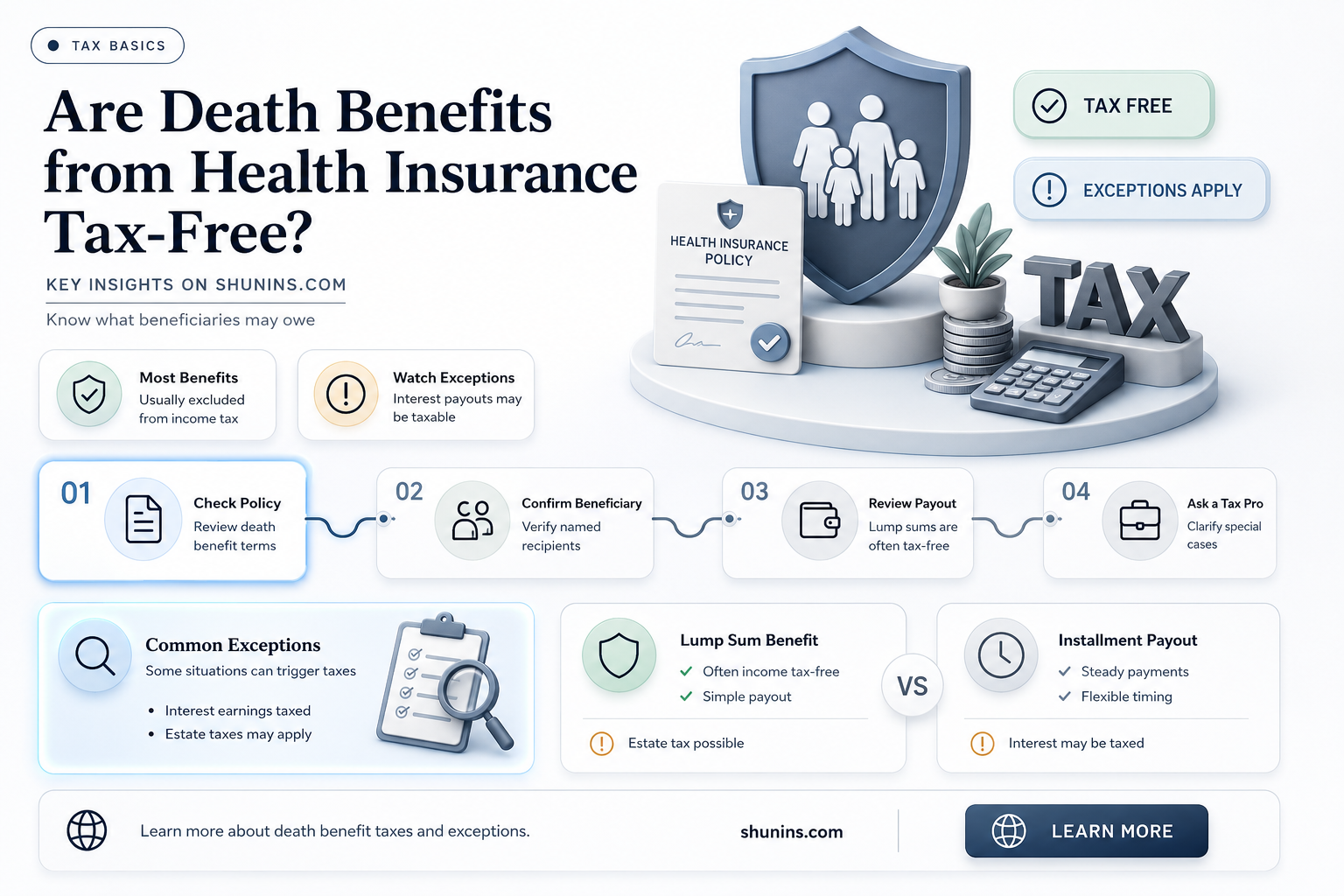

Death benefits received from health insurance policies often raise questions about their tax implications. In many jurisdictions, death benefits paid out from life insurance policies are typically tax-free, as they are considered a return of premiums or a fulfillment of a contractual obligation rather than taxable income. However, when it comes to health insurance, the treatment of death benefits can vary depending on the policy terms and local tax laws. Some health insurance plans may include a death benefit component, but whether these payouts are tax-free depends on factors such as the nature of the benefit, the policy structure, and the specific regulations in the policyholder’s country or region. It is essential for beneficiaries to consult tax professionals or review their policy documents to understand the tax treatment of such benefits in their specific circumstances.

| Characteristics | Values |

|---|---|

| Taxability of Death Benefits | Generally tax-free if received as a lump sum or life insurance payout. |

| Health Insurance Death Benefits | Typically not provided; health insurance covers medical expenses only. |

| Life Insurance Death Benefits | Tax-free under most circumstances (U.S. Internal Revenue Code §101). |

| Employer-Provided Group Life Insurance | First $50,000 is tax-free; amounts above may be taxable as income. |

| Estate Tax Implications | May be subject to estate tax if payable to the estate. |

| State-Specific Rules | Some states may impose inheritance or income tax on death benefits. |

| Annuity Death Benefits | Tax treatment depends on the payout structure (lump sum vs. installments). |

| Accidental Death & Dismemberment (AD&D) | Typically tax-free if paid as a lump sum. |

| Taxable Exceptions | Interest earned on death benefits or certain employer-provided plans. |

| International Tax Treatment | Varies by country; consult local tax laws. |

Explore related products

$6.99 $14.95

What You'll Learn

- Death Benefits from Life Insurance: Typically tax-free under IRC Section 101(a)

- Employer-Provided Group Life Insurance: First $50,000 is tax-free for beneficiaries

- Accidental Death & Dismemberment (AD&D): Benefits are usually tax-free as per IRS rules

- Health Insurance Payouts: Not death benefits; taxable if paid by employer post-death

- Estate Tax Considerations: Large payouts may impact estate taxes, not income taxes

![]()

Death Benefits from Life Insurance: Typically tax-free under IRC Section 101(a)

Death benefits from life insurance are generally tax-free under Internal Revenue Code (IRC) Section 101(a), a provision that offers significant financial relief to beneficiaries during a time of loss. This section explicitly excludes life insurance proceeds from taxable income, meaning the lump sum or installments received by beneficiaries are not subject to federal income tax. However, exceptions exist, such as if the policy was transferred for valuable consideration or if the beneficiary opts for interest-bearing installments, which may trigger taxation on the interest earned. Understanding this rule is crucial for beneficiaries to manage their finances effectively after the policyholder’s death.

To qualify for tax-free treatment, the death benefit must meet specific criteria outlined in IRC Section 101(a). First, the payout must be received directly by the beneficiary as a result of the insured’s death. Second, the policy must have been owned by the insured or someone with an insurable interest, such as a spouse or business partner. If the policy was sold or transferred to a third party, the exclusion may not apply. For example, if a policyholder sells their life insurance policy for a viatical settlement, the proceeds may become taxable to the new owner. Beneficiaries should review the policy’s ownership history to ensure compliance with IRS rules.

While the death benefit itself is typically tax-free, beneficiaries must be aware of potential tax implications in other areas. For instance, if the payout pushes the estate’s value above the federal estate tax exemption threshold, the estate may owe taxes. Additionally, if the beneficiary invests the proceeds and earns interest or dividends, those earnings are taxable. Practical tip: Consult a tax advisor to explore strategies like setting up a trust to manage the death benefit, which can help minimize estate tax exposure and provide long-term financial planning benefits.

Comparing life insurance death benefits to other types of payouts highlights the uniqueness of IRC Section 101(a). Unlike taxable income from wages or investments, life insurance proceeds are treated as a return of premiums paid, not as income. This distinction is rooted in the policy’s purpose—to provide financial security, not to generate taxable gains. For example, if a beneficiary receives $500,000 from a life insurance policy, they report $0 as taxable income, whereas a $500,000 inheritance from a taxable estate might require filing an estate tax return. This tax-free treatment underscores the value of life insurance as a financial safety net.

In conclusion, IRC Section 101(a) provides a clear framework for tax-free death benefits from life insurance, but beneficiaries must navigate its nuances carefully. By understanding the rules, exceptions, and related tax considerations, beneficiaries can maximize the financial support intended by the policyholder. Proactive steps, such as reviewing policy ownership and consulting professionals, ensure compliance and optimize the benefit’s impact. This knowledge transforms a complex tax provision into a practical tool for financial stability during challenging times.

Target Medical Insurance: Signing Up Simplified

You may want to see also

Explore related products

![]()

Employer-Provided Group Life Insurance: First $50,000 is tax-free for beneficiaries

Employer-provided group life insurance often includes a tax-free death benefit of up to $50,000 for beneficiaries, a provision rooted in Section 79 of the Internal Revenue Code. This benefit is designed to ease financial burdens for surviving family members without adding tax liabilities. The first $50,000 is excluded from taxable income because it is considered a de minimis fringe benefit, meaning it is small enough to be administratively impractical to track and tax. For beneficiaries, this means immediate access to funds without the need to set aside money for taxes, providing crucial financial stability during a difficult time.

To qualify for this tax-free benefit, the group life insurance policy must meet specific criteria. First, it must be provided by the employer as part of a group plan, not an individual policy. Second, the coverage amount must not exceed $50,000, or the excess value may become taxable. Employers often offer this benefit as part of a comprehensive benefits package, and employees typically do not need to pay premiums for this coverage, though they may have the option to purchase additional coverage at their own expense. Understanding these parameters ensures beneficiaries can fully leverage the tax-free advantage.

One practical example illustrates the value of this provision: a 35-year-old employee with a spouse and two children passes away unexpectedly. The employer’s group life insurance policy pays out $50,000 to the spouse, who uses the funds to cover funeral expenses, outstanding debts, and immediate living costs. Because the benefit is tax-free, the spouse receives the full $50,000 without any reduction for taxes, allowing the family to focus on emotional recovery rather than financial strain. This scenario highlights how the tax-free nature of the first $50,000 can serve as a financial safety net.

However, beneficiaries should be aware of potential pitfalls. If the deceased employee had opted for additional coverage beyond $50,000, the excess amount would be taxable as income. For instance, if the policy paid out $75,000, the $25,000 above the $50,000 threshold would be subject to federal income tax and possibly state taxes. Beneficiaries should review the policy details and consult a tax professional to understand their obligations. Additionally, if the employer requires employees to pay premiums for any portion of the coverage, the tax treatment may differ, emphasizing the importance of clarity in policy terms.

In conclusion, the tax-free nature of the first $50,000 in employer-provided group life insurance is a valuable benefit for beneficiaries, offering immediate financial relief without tax complications. By understanding the rules and limitations, beneficiaries can maximize this provision’s impact. Employers, too, benefit by offering a cost-effective way to support employees’ families, enhancing overall workplace satisfaction and loyalty. This benefit serves as a reminder of the importance of reviewing and understanding employer-provided benefits to ensure full utilization in times of need.

Debunking Myths: Which Life Insurance Company Claim is False?

You may want to see also

Explore related products

![]()

Accidental Death & Dismemberment (AD&D): Benefits are usually tax-free as per IRS rules

Accidental Death & Dismemberment (AD&D) insurance provides a financial safety net for individuals and their families in the event of a severe accident. One of its most significant advantages is that the benefits paid out are typically tax-free, as outlined by the Internal Revenue Service (IRS). This means that if you or your beneficiaries receive a payout due to an accidental death or dismemberment, the amount is generally not subject to federal income tax. Understanding this tax-free status is crucial for policyholders, as it ensures that the full benefit amount can be utilized for immediate needs, such as medical expenses, funeral costs, or replacing lost income.

To qualify for tax-free status, AD&D benefits must meet specific IRS criteria. According to IRS Publication 525, benefits paid due to accidental death or dismemberment are excluded from taxable income if they are received under an accident or health insurance policy. This includes policies provided by employers as part of a group plan or individually purchased policies. However, it’s essential to note that if the premiums for the policy were paid with pre-tax dollars (e.g., through a cafeteria plan), the benefits may be taxable. Always consult a tax professional to ensure compliance with current regulations.

For families, the tax-free nature of AD&D benefits can provide much-needed financial relief during a difficult time. For example, if a breadwinner dies in a car accident, the beneficiary could receive a lump-sum payment without worrying about a significant tax burden. Similarly, if an individual loses a limb in an accident and receives a dismemberment benefit, this amount can be used to cover medical bills, rehabilitation costs, or home modifications without reducing the payout’s value due to taxes. This makes AD&D insurance a valuable addition to a comprehensive financial plan.

When considering AD&D insurance, it’s important to review the policy’s terms and conditions carefully. Some policies may have exclusions or limitations, such as accidents occurring during high-risk activities or while under the influence of substances. Additionally, benefit amounts for dismemberment are often structured as a percentage of the death benefit, depending on the type and severity of the injury. For instance, losing a hand or foot might pay out 50% of the policy’s face value, while losing sight in one eye could pay out 30%. Understanding these details ensures that you’re adequately covered and can maximize the tax-free benefits available.

In conclusion, AD&D insurance offers a unique advantage with its tax-free benefits, providing financial security without the added stress of tax implications. By familiarizing yourself with IRS rules and carefully selecting a policy, you can ensure that you or your loved ones are protected in the event of a severe accident. Whether as a standalone policy or part of a group plan, AD&D insurance is a practical tool for safeguarding your financial future.

Best Insurance Rates in Ontario: Top Companies Compared for 2023

You may want to see also

Explore related products

![]()

Health Insurance Payouts: Not death benefits; taxable if paid by employer post-death

Health insurance payouts can sometimes blur the lines between benefits and taxable income, especially when they occur post-death. Unlike traditional death benefits, which are typically tax-free, health insurance payouts made by an employer after an employee’s death often fall into a different category. These payments, if made as part of a group health plan, may be considered taxable income to the beneficiary. This distinction arises because health insurance benefits are generally not structured as death benefits but rather as reimbursements or coverage for medical expenses. Understanding this nuance is crucial for beneficiaries to avoid unexpected tax liabilities.

Consider a scenario where an employer continues to pay a deceased employee’s health insurance premiums or provides a lump-sum payout from a group health plan. The IRS treats such payments as taxable income if they exceed the employee’s after-tax contributions. For example, if an employer pays $10,000 in health insurance benefits post-death and the employee contributed $2,000 after taxes, the remaining $8,000 would be taxable to the beneficiary. This rule applies regardless of whether the beneficiary is a spouse, dependent, or other designated recipient. To navigate this, beneficiaries should request a breakdown of contributions and payouts from the employer or insurer to determine the taxable portion accurately.

From a practical standpoint, beneficiaries should proactively consult a tax professional or financial advisor when receiving health insurance payouts post-death. These experts can help interpret the tax implications based on the specific terms of the insurance plan and the deceased’s contributions. Additionally, beneficiaries should retain all documentation related to the payout, including contribution records and plan details, to support their tax filings. Ignoring these steps could result in underreporting income, leading to penalties or audits. Early preparation is key to managing this often-overlooked aspect of estate and tax planning.

Comparatively, life insurance death benefits and health insurance payouts highlight the importance of understanding the source and structure of post-death payments. While life insurance proceeds are generally tax-free, health insurance payouts are not automatically exempt. This difference underscores the need for clarity in employer-provided benefits and individual policies. Beneficiaries should review their loved one’s insurance policies and employer benefits to identify potential tax exposures. By doing so, they can ensure compliance with tax laws while maximizing the financial support intended by these benefits.

In conclusion, health insurance payouts made by an employer post-death are not treated as tax-free death benefits. Instead, they are subject to taxation if they exceed the deceased’s after-tax contributions. Beneficiaries must carefully assess these payments, seek professional guidance, and maintain thorough documentation to avoid tax complications. This proactive approach ensures that the financial support provided through health insurance serves its intended purpose without unintended financial consequences.

Insurance Application: A Window of Opportunity

You may want to see also

Explore related products

![]()

Estate Tax Considerations: Large payouts may impact estate taxes, not income taxes

Death benefits from life insurance policies are generally income tax-free, but this doesn't mean they're entirely exempt from taxation. A critical yet often overlooked area is their impact on estate taxes. When a beneficiary receives a large payout, the amount could increase the value of the deceased's estate, potentially pushing it into a taxable bracket. Estate taxes, levied on the transfer of assets after death, can significantly reduce the inheritance intended for loved ones. Understanding this distinction is crucial for effective estate planning.

Consider a scenario where an individual passes away with a $5 million life insurance policy. If the estate's total value, excluding the policy, is $10 million, the addition of the death benefit could push the estate's value to $15 million. Depending on the jurisdiction, estates above a certain threshold—for instance, $12.92 million in the U.S. as of 2023—may be subject to estate taxes. In this case, the $2.08 million exceeding the threshold could be taxed at rates as high as 40%, drastically reducing the intended inheritance. This highlights the importance of strategic planning to minimize estate tax exposure.

One practical strategy to mitigate this risk is to establish an irrevocable life insurance trust (ILIT). By transferring ownership of the policy to the trust, the death benefit is excluded from the taxable estate. The trust becomes the policyholder and beneficiary, ensuring the payout remains tax-free. However, this must be done at least three years before the insured's death to avoid inclusion in the estate under the IRS's "three-year rule." Consulting an estate planning attorney is essential to navigate these complexities and ensure compliance with tax laws.

Another consideration is the portability of estate tax exemptions between spouses. Married couples can take advantage of the unlimited marital deduction, allowing tax-free transfers between spouses. However, without proper planning, the surviving spouse may not fully utilize the deceased spouse's unused exemption. For example, if the first spouse dies with a $5 million estate and a $10 million exemption, the surviving spouse could inherit the unused $5 million exemption through portability. This requires filing an estate tax return, even if no tax is owed, to preserve the exemption for future use.

In conclusion, while death benefits are income tax-free, their impact on estate taxes demands careful attention. Large payouts can inadvertently trigger estate tax liabilities, reducing the intended inheritance. Strategies such as establishing an ILIT or leveraging portability can help preserve wealth for beneficiaries. Proactive estate planning, tailored to individual circumstances, is key to ensuring that life insurance proceeds fulfill their intended purpose without unintended tax consequences.

Medication-Assisted Therapy: A Cost-Effective Solution for Insurance Companies

You may want to see also

Frequently asked questions

Death benefits received from health insurance policies are generally tax-free in many jurisdictions, as they are considered a return of premiums or a benefit rather than taxable income. However, tax laws vary by country, so it’s important to check local regulations.

In most cases, beneficiaries do not need to report death benefits from health insurance on their tax returns, as these payments are typically tax-exempt. However, if the benefit includes interest or investment gains, those portions may be taxable.

Death benefits from health insurance are usually not subject to estate taxes, as they are paid directly to the beneficiary and not part of the deceased’s estate. However, if the policy is owned by the estate, it may be included in estate tax calculations.