The cost of health insurance for children is a significant concern for many families, as it can vary widely depending on factors such as the type of plan, family size, and the child's age. While children generally require fewer medical services than adults, their inclusion in a health insurance policy can still lead to higher premiums, especially for comprehensive coverage that includes preventive care, vaccinations, and emergency services. Additionally, families with multiple children may face even greater expenses, prompting many to weigh the benefits of robust coverage against the financial burden. Understanding the factors that influence these costs and exploring available options, such as employer-sponsored plans or government programs like CHIP, can help parents make informed decisions to ensure their children’s health without straining their budget.

Explore related products

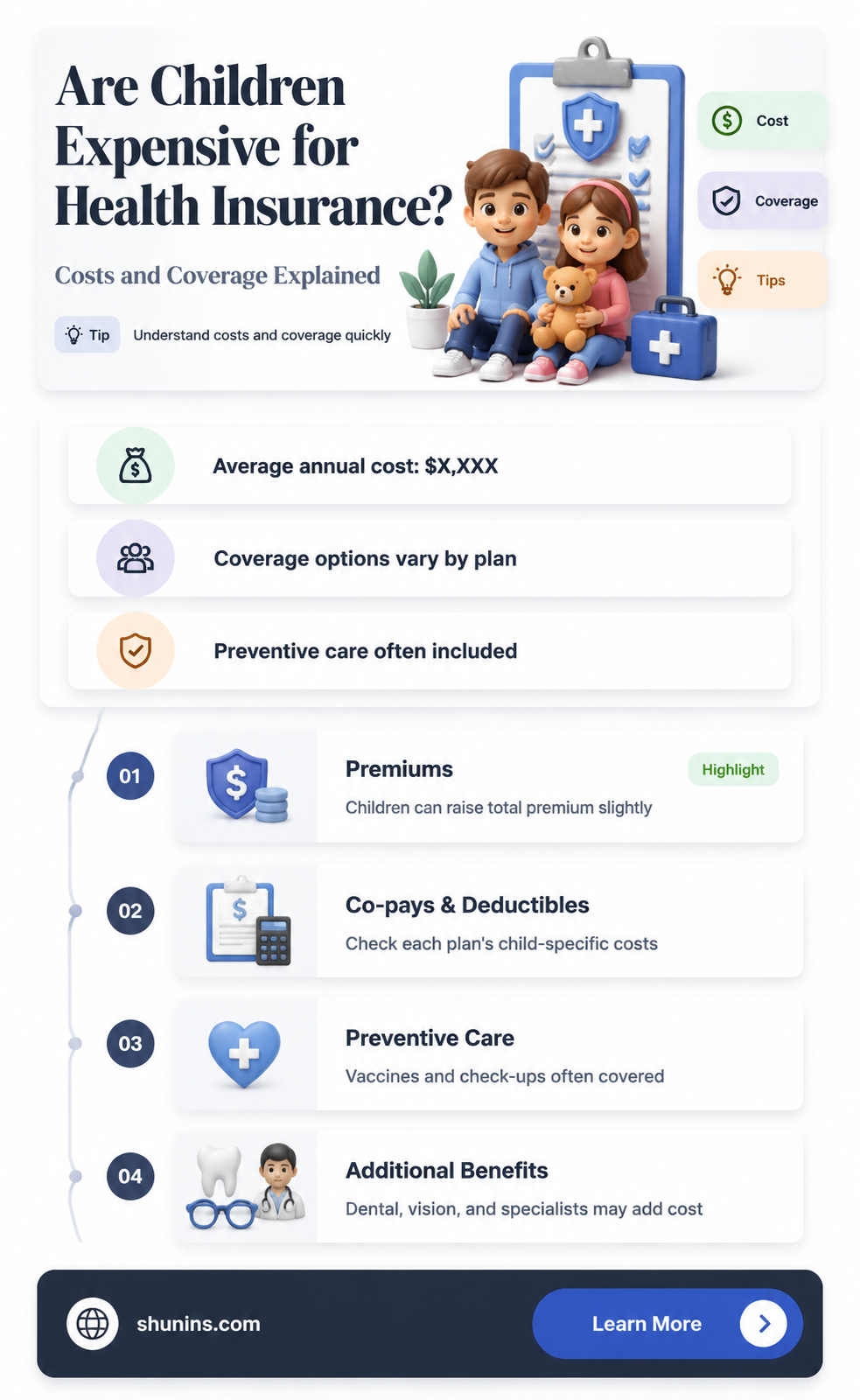

What You'll Learn

![]()

Cost of Adding Children to Plans

Adding children to health insurance plans significantly increases premiums, often by 20% to 50%, depending on the number of children and the plan’s structure. For instance, a family plan with one child might see a monthly premium rise from $600 to $750, while adding a second child could push it to $900 or more. These increases reflect the broader coverage children require, including vaccinations, pediatric visits, and emergency care. Families must weigh these costs against the financial risk of uninsured medical expenses, which can dwarf premiums in the event of serious illness or injury.

The age of the child plays a critical role in cost determination. Infants and toddlers, for example, often incur higher expenses due to frequent well-child visits, immunizations, and developmental screenings. By contrast, older children may have lower routine costs but higher potential expenses for sports injuries or orthodontic care. Some plans offer tiered pricing based on age brackets (e.g., 0–5, 6–12, 13–18), allowing families to anticipate costs as children grow. Understanding these age-related cost drivers helps parents select plans that balance affordability with comprehensive coverage.

Employer-sponsored plans frequently provide subsidies that offset the cost of adding children, making them a more economical option than individual market plans. For example, an employer might cover 70% of the total premium, reducing the family’s out-of-pocket cost from $1,200 to $360 monthly. However, not all employers offer such generous contributions, and part-time workers may be excluded altogether. Families should compare employer-sponsored options with marketplace plans, especially if they qualify for premium tax credits or cost-sharing reductions, which can significantly lower expenses for lower-income households.

Strategic planning can mitigate the financial impact of adding children to health insurance. Families should review plan details annually during open enrollment, considering changes in child health needs, such as upcoming orthodontic work or chronic conditions. High-deductible health plans (HDHPs) paired with health savings accounts (HSAs) can reduce premiums while allowing tax-free savings for future medical expenses. Additionally, bundling children’s preventive care appointments and leveraging telehealth services can maximize cost efficiency without compromising care quality.

Ultimately, the cost of adding children to health insurance plans demands careful consideration of both immediate premiums and long-term health needs. While the expense is undeniable, the alternative—uninsured medical bills—can be financially devastating. By understanding cost drivers, exploring subsidies, and adopting cost-saving strategies, families can secure adequate coverage without breaking the bank. The goal is not to find the cheapest option but the most value-driven one, ensuring children’s health needs are met at every stage of development.

Why Kia Vehicles Are Being Denied Insurance Coverage: Key Factors

You may want to see also

Explore related products

![]()

Child-Specific Coverage Requirements

Children’s health insurance needs are distinct, driven by developmental stages, higher preventive care demands, and legal mandates like the Affordable Care Act’s essential health benefits. Child-specific coverage requirements are not one-size-fits-all; they vary by age, state regulations, and insurer policies. For instance, well-child visits, immunizations, and dental care are federally required for children under 19, but the frequency and scope of these services differ. A 2-year-old might need 4 well-child visits annually, while a 10-year-old may require only 1, yet both must include vision and hearing screenings. Understanding these nuances is critical for parents to avoid gaps in coverage or unexpected out-of-pocket costs.

Pediatric preventive care is a cornerstone of child-specific coverage, often fully covered under ACA-compliant plans. This includes vaccinations like the MMR (measles, mumps, rubella) series, typically administered at 12-15 months and 4-6 years, and the HPV vaccine, recommended starting at age 11. Mental health services, such as autism screenings at 18 and 24 months, are also mandatory. However, not all plans cover specialized therapies equally. For example, applied behavior analysis (ABA) therapy for autism may have annual visit limits or require pre-authorization, even in states with autism mandates. Parents should scrutinize policy details to ensure their child’s specific needs are met.

Chronic conditions in children, such as asthma or diabetes, introduce additional coverage requirements. Asthma, affecting 1 in 12 children, often necessitates regular inhaler prescriptions (e.g., albuterol or fluticasone) and allergy testing. Diabetes care for children includes continuous glucose monitors (CGMs) and insulin pumps, which can cost $5,000-$7,000 annually without adequate coverage. Some plans may limit CGM supplies to one per month, insufficient for active children. Parents should verify coverage for durable medical equipment (DME) and specialty medications to prevent financial strain.

Dental and vision care are often siloed in child-specific coverage, requiring separate policies or add-ons. Pediatric dental plans typically cover two cleanings per year, fluoride treatments, and orthodontic evaluations starting at age 7. Vision coverage usually includes annual eye exams and a pair of glasses or contacts. However, some plans cap orthodontic benefits at $1,000-$1,500 lifetime, far below the $5,000 average cost of braces. Families should assess their child’s risk factors—such as a history of myopia or malocclusion—and choose plans with appropriate benefit levels.

Finally, emergency and urgent care needs highlight the importance of network adequacy in child-specific coverage. Children are twice as likely as adults to visit the ER, often for injuries or sudden illnesses. Plans with narrow networks may limit access to pediatric specialists or children’s hospitals, delaying critical care. Parents should verify in-network providers and understand out-of-network costs, especially for services like stitches or fracture care. Proactively selecting a plan with robust pediatric emergency coverage can save thousands in unexpected bills and ensure timely treatment for a child’s unique vulnerabilities.

Why Cholangiocarcinoma Often Falls Outside Insurance Coverage

You may want to see also

Explore related products

![]()

Impact on Monthly Premiums

Adding children to a health insurance plan invariably increases monthly premiums, but the extent of this increase varies widely based on factors like family size, location, and plan type. For instance, a family adding one child to a Silver-level plan under the Affordable Care Act (ACA) might see premiums rise by 20% to 50%, depending on the state. In high-cost regions like New York or California, this could translate to an additional $150 to $300 per month. Conversely, states with lower healthcare costs, such as Alabama or Mississippi, may see increases closer to $100. Understanding these regional disparities is crucial for families budgeting for expanded coverage.

The age of the child also plays a role in premium calculations, though less directly than one might assume. Insurers typically categorize dependents into broad age groups (e.g., 0–18), with premiums increasing incrementally for each additional child rather than scaling with age. For example, adding a newborn to a plan may cost the same as adding a teenager, despite differing healthcare utilization patterns. This flat-rate approach simplifies pricing but can feel inequitable for families with younger children who require more frequent pediatric care. To mitigate costs, families can explore plans with lower premiums but higher deductibles, balancing monthly expenses with out-of-pocket risks.

Employer-sponsored plans often soften the financial blow of adding children, as employers typically subsidize a portion of family coverage. However, the employee’s share of the premium still rises significantly—sometimes doubling—when transitioning from individual to family coverage. For instance, an employee paying $200 monthly for individual coverage might see their share jump to $400 for a family plan. To navigate this, employees should review their company’s open enrollment materials carefully, comparing the cost of adding dependents to the potential savings from tax-advantaged Flexible Spending Accounts (FSAs) or Health Savings Accounts (HSAs).

For families purchasing insurance on the ACA marketplace, premium tax credits can offset the cost of adding children, but eligibility depends on household income. A family of four earning up to 400% of the federal poverty level (approximately $111,000 in 2023) may qualify for subsidies that reduce monthly premiums. For example, a family earning $75,000 annually might pay only $300 monthly for a family plan instead of the unsubsidized $800. To maximize savings, use the marketplace’s subsidy calculator during enrollment and update income information annually to reflect any changes.

Finally, families should consider the long-term value of comprehensive coverage for children, even if premiums are higher. Pediatric preventive services, such as vaccinations and well-child visits, are covered at no cost under most plans, potentially saving hundreds of dollars annually. Additionally, children with preexisting conditions benefit from guaranteed coverage under the ACA, eliminating the risk of premium surcharges or denials. While the immediate impact on monthly premiums is undeniable, the financial and health security provided by robust insurance often outweighs the added expense.

Sitting Your Company's Exams: Can It Lower Your Insurance Premiums?

You may want to see also

Explore related products

$4.99 $5.99

![Waterproof Air Tag Bracelet for Kids [2 Pack], Cute Cartoon Air Tag Holder for Kids with Full Coverage Hidden Design, Silicone Airtag Wristband for Child, Healthy Material Red+Black](https://m.media-amazon.com/images/I/81WXwSAP5CL._AC_UY218_.jpg)

![]()

Preventive Care for Kids

Children’s health insurance costs often reflect the frequency of their medical needs, but preventive care can significantly reduce long-term expenses. Regular check-ups, vaccinations, and early screenings are not just medical recommendations—they are cost-saving strategies. For instance, the American Academy of Pediatrics (AAP) recommends well-child visits at specific intervals: 3-5 days after birth, then at 1, 2, 4, 6, 9, 12, 15, 18, and 24 months, followed by annual visits. These visits often include developmental screenings, immunizations, and growth monitoring, which can catch issues before they escalate into costly treatments. Insurance plans typically cover these preventive services at no out-of-pocket cost, making them a financially savvy choice for parents.

Consider the impact of vaccinations, a cornerstone of preventive care. The CDC’s immunization schedule for children includes vaccines like MMR (measles, mumps, rubella), DTaP (diphtheria, tetanus, pertussis), and influenza, administered in specific doses by age. For example, the flu vaccine is recommended annually starting at 6 months, while the MMR vaccine is given in two doses, the first at 12-15 months and the second at 4-6 years. These vaccines prevent diseases that can lead to hospitalizations costing thousands of dollars. A 2018 study in *Health Affairs* found that every dollar spent on childhood immunizations saves $10 in healthcare costs. By adhering to these schedules, parents not only protect their children’s health but also minimize insurance claims related to preventable illnesses.

Beyond vaccinations, preventive care includes dental and vision screenings, which are often overlooked. The AAP advises the first dental visit by age 1, yet many children don’t see a dentist until much later. Early dental care can prevent cavities, which affect over 40% of U.S. children by kindergarten and can lead to costly procedures like fillings or root canals. Similarly, vision screenings starting at age 3 can detect issues like amblyopia (lazy eye), which, if untreated, can cause permanent vision loss. Most insurance plans cover these screenings, but parents must proactively schedule them. A simple tip: pair dental and vision appointments with annual check-ups to ensure consistency.

Nutrition and behavioral health are also critical components of preventive care. Childhood obesity, affecting 1 in 5 U.S. kids, can lead to diabetes, asthma, and other chronic conditions that drive up insurance costs. Pediatricians often provide guidance on age-appropriate diets, such as limiting sugar intake to less than 25 grams per day for children over 2. Behavioral health screenings, recommended starting at age 10, can identify anxiety, depression, or ADHD early, allowing for timely interventions. These services are typically covered under preventive care, but parents must advocate for them during visits. For example, ask your pediatrician about BMI tracking, dietary advice, and mental health assessments during well-child visits.

Finally, preventive care extends to safety measures that reduce injury risks, a leading cause of childhood hospitalizations. Car seat checks, for instance, ensure proper installation and use, reducing injury risk by 71-82% in car accidents. Pediatricians often provide guidance on age-appropriate car seats: rear-facing until age 2, forward-facing with a harness until at least 4, and booster seats until seat belts fit properly (usually 9-12 years). Insurance plans may also cover safety devices like helmet fittings or home safety kits. By investing time in these preventive steps, parents not only safeguard their children but also avoid the high costs of emergency care. Preventive care isn’t just a health strategy—it’s a financial one.

Dental Insurance Coverage for Adults with Medicaid

You may want to see also

Explore related products

![]()

Subsidies for Family Health Insurance

Children under 18 represent 23% of the U.S. population but account for only 15% of total healthcare spending, according to the Centers for Medicare & Medicaid Services. Yet, their inclusion in family health insurance plans often triggers premium increases, leaving many families struggling to afford coverage. Subsidies, however, can significantly offset these costs, making comprehensive care accessible for dependents.

Eligibility for Subsidies: A Step-by-Step Guide

To qualify for family health insurance subsidies, households must meet specific income thresholds, typically ranging from 100% to 400% of the federal poverty level (FPL). For a family of four in 2023, this translates to an annual income between $29,900 and $119,680. Applications are processed through the Health Insurance Marketplace, where the number of dependents directly influences subsidy amounts. For instance, a family with two children earning $75,000 annually might receive a monthly premium reduction of $300 or more, depending on plan selection.

Types of Subsidies: Advanced Premium Tax Credits vs. Cost-Sharing Reductions

Advanced Premium Tax Credits (APTC) lower monthly premiums, while Cost-Sharing Reductions (CSRs) reduce out-of-pocket expenses like deductibles and copays. Families with children often benefit more from CSRs, as pediatric care frequently involves preventive services (covered at 100%) and unexpected illnesses. For example, a CSR-eligible family might pay only $20 for a child’s asthma inhaler, compared to $200 without assistance.

Practical Tips for Maximizing Subsidies

First, update your Marketplace application annually to reflect changes in income or family size, as subsidies are recalculated each year. Second, consider enrolling in a Silver-tier plan if eligible for CSRs, as these plans offer enhanced cost-sharing benefits for families. Lastly, explore state-specific programs like CHIP (Children’s Health Insurance Program), which provides low-cost coverage for children in households earning too much for Medicaid but still struggling with private insurance costs.

Long-Term Impact: Subsidies as a Tool for Preventive Care

Subsidies not only make insurance affordable but also encourage consistent pediatric care, reducing long-term healthcare costs. Vaccinations, well-child visits, and early intervention for conditions like ADHD or asthma are fully covered under subsidized plans, preventing minor issues from escalating into costly emergencies. By leveraging these programs, families can ensure their children receive timely care without financial strain.

Renters Insurance: Understanding Medical Payments Coverage

You may want to see also

Frequently asked questions

Children are generally less expensive to insure than adults because they typically require fewer medical services and have lower healthcare costs.

Adding a child to your plan will increase your premiums, but the cost is usually lower compared to adding an adult, as children’s coverage tends to be less expensive.

Yes, programs like the Children’s Health Insurance Program (CHIP) offer low-cost or free health insurance for eligible children in low-income families.

Costs may vary slightly by age, but children’s premiums are primarily based on family size and plan type rather than individual health conditions, thanks to regulations like the Affordable Care Act.