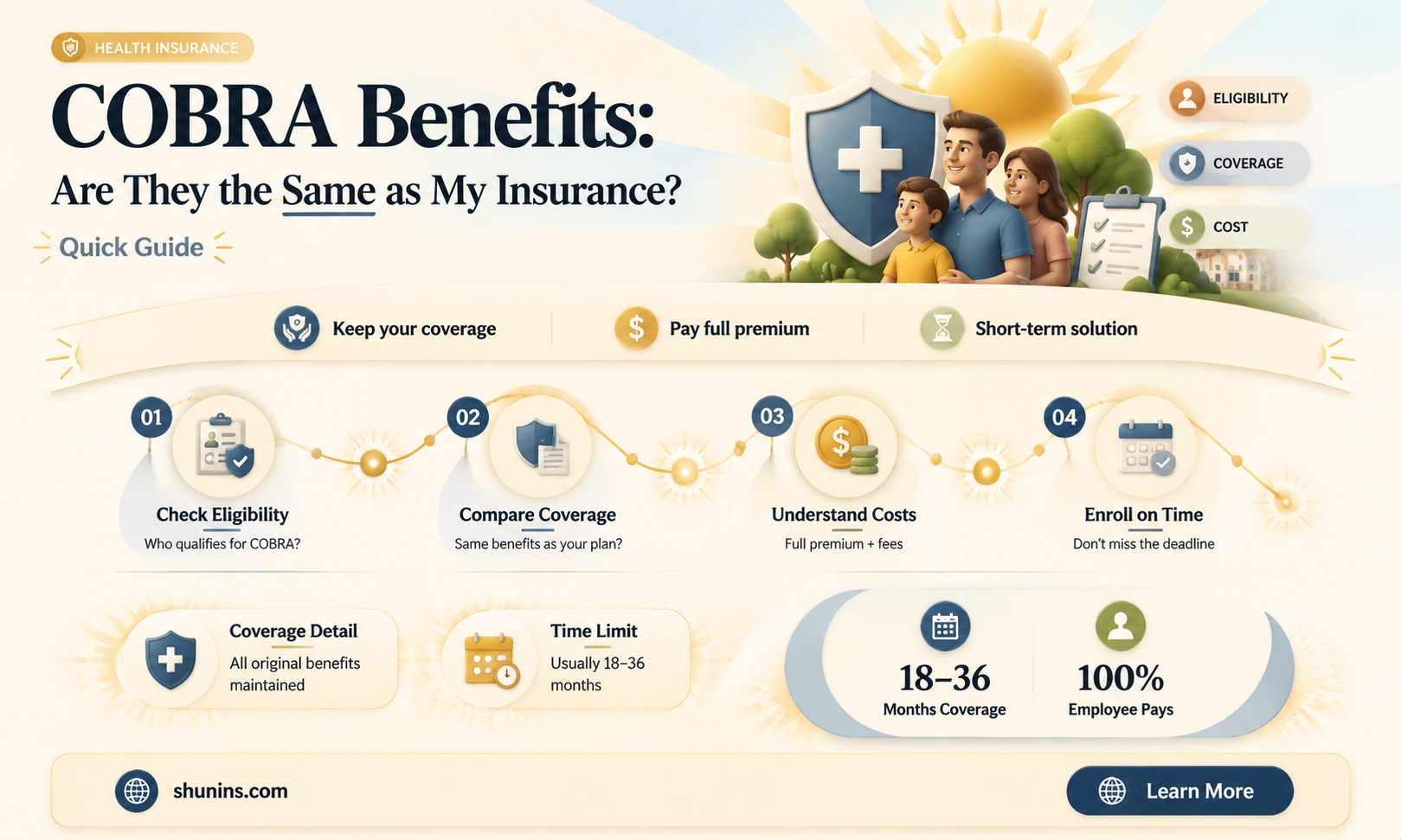

If you've lost your job, had your hours reduced, or experienced another qualifying event, you may be eligible for COBRA insurance, which allows you to temporarily maintain your employer-provided health insurance coverage. COBRA insurance covers the same benefits as your employer's health plan, including medical, dental, pharmacy, and behavioural health services. However, it does not cover supplemental coverage such as disability or life insurance. While COBRA can provide continuity of coverage and access to the same healthcare providers, it is important to note that it can be significantly more expensive since you are responsible for paying the full premium plus an administrative fee. Therefore, it is essential to weigh the pros and cons of COBRA insurance and explore other options, such as joining a spouse's plan or enrolling in a government-offered individual health insurance plan.

| Characteristics | Values |

|---|---|

| Coverage | COBRA offers the same coverage as your previous employer's health plan. |

| Cost | COBRA can be more expensive than your previous plan as you pay 100% of the costs plus a 2% service fee. |

| Duration | COBRA coverage typically lasts 18-36 months but can be extended due to qualifying events. |

| Eligibility | COBRA is available to employees who worked at a company with 20 or more employees. |

| Alternatives | Other options include joining a spouse's plan, enrolling in a group plan, or applying for CHIP. |

Explore related products

What You'll Learn

- COBRA insurance provides the same benefits as your employer's health plan

- COBRA insurance is available to employees who worked at a public or private company with 20 or more employees

- COBRA insurance is temporary and can last for 18 to 36 months depending on the qualifying event

- COBRA insurance can be significantly more expensive as you pay 100% of the costs for the health plan

- COBRA insurance is not your only option if you lose your employer-sponsored plan

![]()

COBRA insurance provides the same benefits as your employer's health plan

Losing your job is stressful, and one of the biggest concerns is often the loss of employer-sponsored health insurance. This is where COBRA insurance comes in. COBRA is an acronym for the Consolidated Omnibus Budget Reconciliation Act, a federal law created in 1985. It gives individuals who experience a job loss or other qualifying events the option to continue their current health insurance coverage for a limited amount of time.

However, it's important to note that COBRA can be significantly more expensive than what you paid under your employer's plan. This is because you are now responsible for paying 100% of the costs for the health plan, including any costs previously covered by your employer. There is also an additional administrative fee of up to 2% of the premium cost.

COBRA coverage typically lasts for 18 to 36 months, depending on the qualifying event that made you eligible. It is a temporary solution to help bridge the gap between job-based coverage and finding new health insurance options. During this time, it's essential to explore other insurance plans to ensure continued coverage once your COBRA benefits end.

Colonial Penn Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

COBRA insurance is available to employees who worked at a public or private company with 20 or more employees

Losing your job can be stressful, especially when it comes to figuring out your insurance situation. COBRA insurance is available to employees who worked at a public or private company with 20 or more employees. This means that if you worked at a company with 20 or more employees and you lose your job, you may be eligible for COBRA insurance.

COBRA insurance is a federal law that allows you to temporarily continue your current health insurance coverage after leaving your job. It is called the Consolidated Omnibus Budget Reconciliation Act and was created in 1985. This law gives individuals who experience a job loss or other qualifying events the option to maintain their health insurance coverage for a limited time.

The duration of COBRA coverage depends on the qualifying event that made you eligible. For example, if your hours were reduced or you were terminated, you can typically receive COBRA benefits for 18 months. In cases of divorce, legal separation, or the death of the covered employee, COBRA coverage for the spouse or dependent child can last for 36 months.

COBRA insurance provides the same benefits as your employer's health plan, including medical, dental, pharmacy, and behavioural coverage. However, it does not cover supplemental insurance like disability, life insurance, or hospital care insurance. One significant difference is that under COBRA, you are responsible for paying 100% of the costs for the health plan, which can make it more expensive than your previous coverage.

It's important to note that COBRA insurance is not your only option when you lose your job. You may also qualify for other health benefits, such as joining your spouse's employer plan, enrolling in a trade or professional group plan, or applying for the Children's Health Insurance Program if you have a low to moderate family income.

MetLife Annuity Contracts: Insurance for Life?

You may want to see also

Explore related products

![Cobra - Collector's Edition [Blu-ray]](https://m.media-amazon.com/images/I/81mc0ZQlTvL._AC_UY218_.jpg)

![]()

COBRA insurance is temporary and can last for 18 to 36 months depending on the qualifying event

COBRA insurance is a federal law that allows employees to temporarily maintain their employer-provided health insurance during situations such as job loss or a reduction in hours worked. It is a helpful option for those who need health coverage during the transition period between losing job-based coverage and starting new health coverage.

COBRA insurance is indeed temporary and can last for 18 to 36 months, depending on the qualifying event. Employees who lose their jobs can typically stay on COBRA for up to 18 months. This coverage period provides flexibility in finding other health insurance options. However, it is important to note that COBRA may be more expensive than other options as individuals are responsible for paying their portion of the health insurance cost, which includes any costs previously covered by the employer, plus a 2% administrative fee.

Dependents on the plan, such as a spouse or children, may be eligible for up to 36 months of coverage under certain circumstances, such as divorce or the death of the covered employee. Adult children can use COBRA rights for 36 months to keep their parent's health insurance plan until they turn 26. Additionally, if an individual on the plan qualifies as disabled within the first 60 days of COBRA coverage, the coverage period may be extended to 29 months upon determination by the Social Security Administration (SSA).

It is worth noting that COBRA is not the only option when losing employer-sponsored health insurance. Other alternatives include joining a spouse's employer plan, enrolling in a trade or professional group plan, or applying for the Children's Health Insurance Program (CHIP) for low-to-moderate income families.

Term Life Insurance: Understanding Its Characterization

You may want to see also

Explore related products

![]()

COBRA insurance can be significantly more expensive as you pay 100% of the costs for the health plan

COBRA insurance is a federal law that gives individuals who experience a job loss or other qualifying events the option to continue their current health insurance coverage for a limited amount of time. It is called the Consolidated Omnibus Budget Reconciliation Act and was created in 1985. Employers outside the federal government with more than 20 employees are required to offer COBRA coverage to those who qualify.

There are alternative options to COBRA insurance that may be more affordable. One option is to join your spouse's employer's plan, as losing your job triggers a special enrollment period. Another option is to enroll in a trade or professional group plan, such as the National Association for the Self-Employed or the Freelancers Union. You can also apply for the Children's Health Insurance Program (CHIP) if you are a low-to-moderate income family. Additionally, you can shop for individual health plans on the government's individual health insurance marketplace, healthcare.gov, which offers plans under the Affordable Care Act (ACA).

It is important to weigh the pros and cons of COBRA insurance and alternative options to determine which policy best fits your needs. COBRA insurance provides the benefit of continuing your current health insurance coverage, including the same group rate and network of providers. However, the cost of COBRA insurance may be a significant factor to consider, as it can be more expensive than other options.

Mortgage Life Insurance: Protecting Your Home and Family

You may want to see also

Explore related products

![]()

COBRA insurance is not your only option if you lose your employer-sponsored plan

Losing your job is stressful, and one of the most important things to consider is how you will maintain your health insurance coverage. While COBRA insurance can be a good option for some, it is not your only option. Here are some alternatives to consider if you lose your employer-sponsored health plan:

Join your spouse's employer plan

If your spouse has employer-sponsored health insurance, losing your job is considered a qualifying life event that allows you to join their plan outside of the usual open enrollment period. You must do this within 30 days of losing your job.

Enroll in a trade or professional group plan

There are several national organizations that offer health benefits for independent workers at a lower cost. For example, the National Association for the Self-Employed and the Freelancers Union offer health benefits with affordable membership fees.

Apply for the Children's Health Insurance Program (CHIP)

If you are a low-to-moderate income family, you may be eligible for the Children's Health Insurance Program (CHIP). This program provides health coverage for children in families who do not qualify for Medicaid but cannot afford private insurance.

Choose a health plan on the government's individual health insurance marketplace

You can visit HealthCare.gov to explore individual health plans and compare costs. A qualifying life event, such as losing your job, allows you to enroll outside of the open enrollment period, and you have 60 days to choose a plan.

Private Health Insurance

Private health insurance is another option to consider, but it can be more expensive. The cost of private insurance is expected to continue rising, so be sure to weigh the pros and cons before choosing this option.

Remember, it is essential to plan ahead to avoid any lapse in coverage and to find the most suitable and affordable option for your needs.

Life Insurance: Estate Creditors and Your Policy's Protection

You may want to see also

Frequently asked questions

Consolidated Omnibus Budget Reconciliation Act.

COBRA insurance covers the same benefits your employer's health plan covered you for. This includes medical, dental, pharmacy, and behavioural benefits.

COBRA coverage typically lasts for 18 to 36 months, depending on the qualifying event that made you eligible.

COBRA insurance can be significantly more expensive than what you paid under your employer's plan because you are now responsible for paying the full premium, plus an administrative fee.

Alternatives to COBRA insurance include joining your spouse's employer plan, enrolling in a trade or professional group plan, or applying for the Children's Health Insurance Program (CHIP) if you're a low-to-moderate income family.