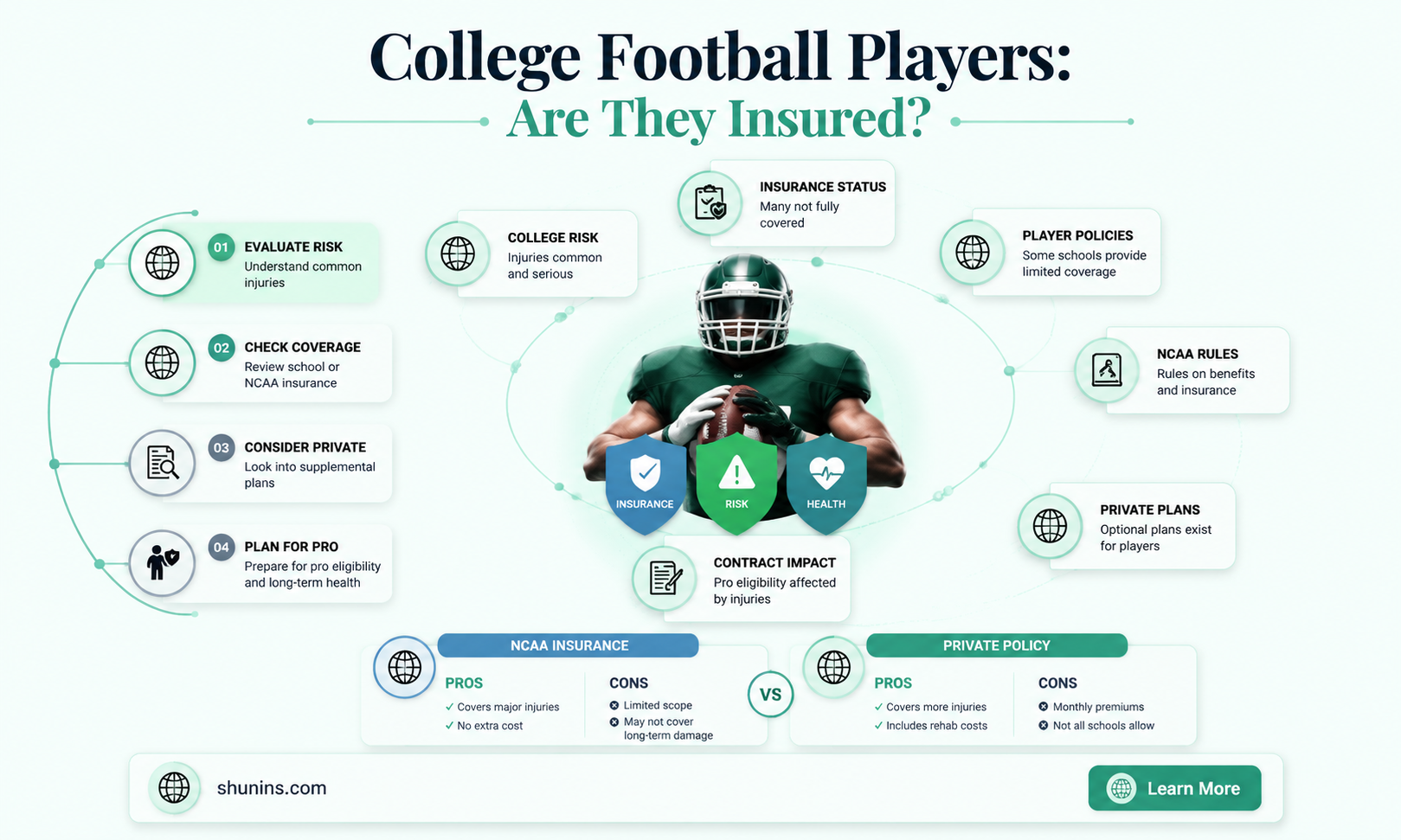

College football players in the US are insured, but the quality of their insurance is a matter of debate. The NCAA provides two types of insurance: the catastrophic injury insurance program and the Exceptional Student-Athlete Disability Insurance Program. The former has a $90,000 deductible, meaning it only kicks in after this sum has been paid through other coverage. The latter provides coverage for high-profile athletes who suffer a career-ending injury, but players must prove their professional draft stock, pay high premiums, and can have their benefits cut if they are able to work full-time after their injury. Additionally, colleges can choose to pay for insurance policies for their athletes out of the student assistance fund provided by the NCAA, but not all colleges do so. As a result, some college football players have to secure loans to pay for insurance premiums, and the policies may not fully cover their losses if they are injured and drop in the draft.

| Characteristics | Values |

|---|---|

| Can college football players get insured? | Yes, college football players can take out insurance policies. |

| Who provides the insurance? | The NCAA provides insurance plans for student-athletes, but these are considered inadequate by some. Private companies like A-G Specialty Insurance also offer insurance plans for college athletes. |

| What type of insurance can they get? | College football players can get loss-of-value (LOV) insurance, which is an add-on to a permanent total disability insurance policy. |

| Who pays for the insurance? | The NCAA provides a student assistance fund that universities can use to pay for insurance policies, but it is not mandatory. Some schools choose to pay for their athletes' insurance, while others may secure loans or use personal funds. |

| Why do college football players need insurance? | The sport has inherent risks of injuries, including long-term and head injuries. Insurance protects players financially if they get hurt and slip in the draft, resulting in a financial loss. |

Explore related products

![Lamshaw Compatible for KeenPlus MP4 Player Screen Protector, [6 Pack] Full Coverage TPU Clear Film Compatible for KeenPlus C4 4.3" MP4 Player (6 Pack)](https://m.media-amazon.com/images/I/71Q2ldL56QL._AC_UY218_.jpg)

![Lamshaw Compatible for ZAQE X20 Mp3 Player Screen Protector, [6 Pack] Full Coverage TPU Clear Film Compatible for ZAQE X20 2 inches HiFi Mp3 Player (6 Pack)](https://m.media-amazon.com/images/I/71CeW3FpfCL._AC_UY218_.jpg)

![Lamshaw Compatible for ODEJOI Mp3 Player Screen Protector, [6 Pack] Full Coverage TPU Clear Film Compatible for ODEJOI 2 inches HiFi Mp3 Player (6 Pack)](https://m.media-amazon.com/images/I/81RHkskFuoL._AC_UY218_.jpg)

![Lamshaw Compatible for Surfans F22 Mp3 Player Screen Protector, [6 Pack] Full Coverage TPU Clear Film Compatible for Surfans F22 2.8" inches HiFi Mp3 Player (6 Pack)](https://m.media-amazon.com/images/I/81SUvmdJvlL._AC_UY218_.jpg)

![Lamshaw Compatible for PECSU G4S MP3 Player Screen Protector, [6 Pack] Full Coverage TPU Clear Film Compatible for PECSU G4S 4" MP3 Player (6 Pack)](https://m.media-amazon.com/images/I/717E8fuFUVL._AC_UY218_.jpg)

What You'll Learn

![]()

Loss-of-value insurance

College football players can take out insurance policies to protect themselves financially in the event of an injury that could hurt their future and their team's fortunes. This type of insurance is called loss-of-value insurance or LOV insurance.

LOV insurance is an add-on to a permanent total disability insurance policy. It cannot be purchased on its own; it must be added to a PTD policy to provide protection in case of a catastrophic injury. The insurance pays the difference between the actual contract's value and the policy's predetermined threshold value if the athlete's professional contract falls below the threshold due to an injury or illness during the coverage period.

The cost of LOV insurance can be covered in a few ways. One way is for the player to borrow against their future earnings, allowing them to receive protection before the draft and repay the insurance provider after signing their contract. Another option is for the player's university to cover the costs using the Student Assistance Fund provided by the NCAA to help student-athletes financially.

The availability of LOV insurance for college football players has decreased in recent years, with only about half a dozen prospects securing such coverage before the 2018 NFL Draft, compared to over 45 players in the previous year's draft class. However, as the earning potential for college athletes continues to grow, and with football being an inherently violent sport, the demand for LOV insurance is likely to increase.

Life Insurance: Adaptable Options for a Changing World

You may want to see also

Explore related products

![Lamshaw Compatible for Oilsky H18 Mp3 Player Screen Protector, [6 Pack] Full Coverage TPU Clear Film Compatible for Oilsky H18 4.0" Mp3 Player (6 Pack)](https://m.media-amazon.com/images/I/71Zh25g5NPL._AC_UY218_.jpg)

![Lamshaw Compatible for SHANLING M3 Plus MP3 Player Screen Protector, [6 Pack] Full Coverage TPU Clear Film Compatible for SHANLING M3 Plus 4.7 Inches MP3 Player (6 Pack)](https://m.media-amazon.com/images/I/71+mwdrp0sL._AC_UY218_.jpg)

![Lamshaw Compatible for Surfans F35 Mp3 Player Screen Protector, [6 Pack] Full Coverage TPU Clear Film Compatible for Surfans F35 4.0 inches HiFi Mp3 Player (6 Pack)](https://m.media-amazon.com/images/I/710nlQ8nzfL._AC_UY218_.jpg)

![Lamshaw Compatible for PECSU S2 MP3 Player Screen Protector, [6 Pack] Full Coverage TPU Clear Film Compatible for PECSU S2 1.77" MP3 Player (6 Pack)](https://m.media-amazon.com/images/I/71AdmtlAgtL._AC_UY218_.jpg)

![]()

Permanent total disability insurance

College football players can take out insurance policies to protect themselves financially in case of injuries that could hurt their future and their teams' fortunes. One such insurance policy is permanent total disability insurance. This type of insurance covers athletes for long-term or career-ending injuries, providing a safety net that allows them to focus on recovery without financial worries.

The general rule is that a top-10 pick will qualify for $10 million of permanent total disability with a $5 million loss-of-value rider. The 10 to 20 picks would be looking at $5 to $7.5 million of permanent total disability and $2 to $3 million in loss of value. Picks in the 20 to 30 pick range would be around $5 million in total disability.

The NCAA provides a student assistance fund to every university, which can be used to help student-athletes financially. Universities are allowed to pay for insurance policies out of this fund, but not all universities choose to do so. For example, Texas A&M paid $50,000 from this fund to help offensive lineman Cedric Ogbuehi secure insurance. On the other hand, Jake Butt and his family secured loans to pay for the premium instead of using the student assistance fund at Michigan.

How Insured Are Casinos?

You may want to see also

Explore related products

![]()

Student assistance fund

College football players in the US have traditionally been required to have a basic health and accident plan. However, the insurance coverage provided by universities has often been deemed inadequate, especially in the case of a dangerous sport such as college football, where the risk of long-term injuries, particularly head injuries, is high.

To address this issue, the NCAA has introduced a Two-Year Post Eligibility Insurance Program, which aims to support student-athletes beyond their playing days. This program includes the option for post-eligibility injury insurance coverage, with a deductible of $90,000, which will be available to member schools beginning August 1, 2024. Additionally, the NCAA offers permanent total disability (PTD) coverage, which can be supplemented with a loss-of-value insurance rider to protect athletes' future earnings in the event of an injury.

The Student Assistance Fund is a crucial component of the financial support provided to college football players. This fund is provided by the NCAA to every university and can be used to financially assist student-athletes in a variety of scenarios, including travel for funerals, formula for babies, and insurance policy premiums. While not all universities choose to use the fund for insurance purposes, it serves as a safety net for athletes facing emergency situations.

The availability of insurance coverage for college football players is evolving, with the introduction of Name, Image, and Likeness (NIL) policies in 2021, allowing athletes to profit from their names, images, and likenesses while maintaining their amateur status. These policy changes have expanded financial benefits and opportunities for student-athletes, including the implementation of healthcare coverage recommendations.

While the insurance landscape for college football players is improving, there is still a need for high-quality, comprehensive healthcare and insurance coverage that prioritizes the health and well-being of athletes over financial considerations.

First Citizens Bank: Life Insurance Offerings and Benefits

You may want to see also

Explore related products

![]()

Exceptional Student-Athlete Disability Insurance Program

The Exceptional Student-Athlete Disability Insurance Program (ESDI) is one of the two health and accident plans provided by the NCAA, the other being the catastrophic injury insurance program. The ESDI program offers extra disability insurance coverage to a select group of elite athletes who are likely to earn millions from careers in professional sports.

Student-athletes are eligible for the program if they have remaining athletic eligibility and have demonstrated their professional potential to be selected in the first two rounds of the upcoming NFL, NHL, or NBA drafts, or the first round of the MLB or WNBA drafts. Exceptional student-athletes in other sports who have demonstrated a strong likelihood of a professional career in their sport may be eligible for coverage under the ESDI Program and can be reviewed on a case-by-case basis by the program administrator, Tokio Marine HCC – Specialty Group.

The ESDI program offers a permanent total disability (PTD) policy, providing 24-hour accident and sickness coverage, including playing and practicing in the student-athlete's respective sport. The policy provides a maximum coverage of $3,000,000 for a PTD policy as quoted by Tokio Marine HCC. To be eligible for benefits, it must be medically determined that the insured student-athlete will never be able to participate in the applicable sporting activity at the professional level.

However, the ESDI program has limitations and flaws. For instance, players have to prove their high professional draft stock in an ambiguous process and pay high premiums. Additionally, disability coverage only comes into effect if an athlete is completely disabled and unable to work any full-time job after their injury. If they can work full-time, the insurance benefits can be reduced to zero, which is a common provision in most disability insurance policies.

Finding the Right Life Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Name, Image and Likeness (NIL) policies

In June 2021, the NCAA implemented an interim policy on name, image and likeness (NIL), allowing college athletes to make money from their personal brand. NIL laws vary by state, and each individual school has oversight of NIL deals, with the right to object to a deal if it conflicts with existing agreements.

NIL gives college athletes the right to benefit financially from the use of their names, images, and likenesses through product endorsements and other commercial activities. This set of rules is protected by the legal concept of the "right of publicity," which generally recognizes that individuals have the right to decide whether their name, photograph, or likeness can be used for commercial purposes and to be compensated for such uses.

Athletes can engage in NIL activities if they follow state laws where their school is located, and schools must ensure these activities comply with state law. Athletes in states without NIL laws can still participate in NIL activities without breaking NCAA rules. Additionally, athletes are allowed to seek professional service providers for their NIL activities and must report NIL activities to their school.

The College Sports Commission (CSC) was created to handle the regulation and enforcement of player compensation issues, including NIL deals. The CSC, in cooperation with Deloitte, launched the NIL Go portal to ensure "fair market value" and a valid business purpose for each deal. The Valid Business Purpose qualification requires that any deal entered into by an athlete must demonstrate Evidence of using the student-athlete's NIL to promote a good or service being offered to the public for profit.

Term Life Insurance: Tax Implications and You

You may want to see also

Frequently asked questions

College football players are not automatically insured. However, they can take out insurance policies to protect themselves financially in case they get hurt and slip in the draft.

College football players can get a loss-of-value or LOV insurance policy. This is a rider or add-on to a permanent total disability insurance policy.

The underwriters set a LOV threshold, which is the draft selection below which the athlete must fall to trigger LOV policy benefits. If the athlete signs a professional contract below this threshold due to an injury or illness during the coverage period, the insurance pays the difference between the actual contract's value and the policy's predetermined threshold value.

The NCAA offers a Two-Year Post Eligibility Insurance Program, which provides support to student-athletes beyond their playing days. The NCAA also offers catastrophic injury insurance, which has a deductible of $90,000, and the Exceptional Student-Athlete Disability Insurance Program. Additionally, companies like A-G Specialty Insurance offer plans such as participant injury insurance and 24-hour student AD&D plans.

College football is a dangerous sport, and injuries can have a significant financial impact on players and their families. Insurance provides a safety net and peace of mind, allowing players to focus on their recovery without worrying about medical expenses.