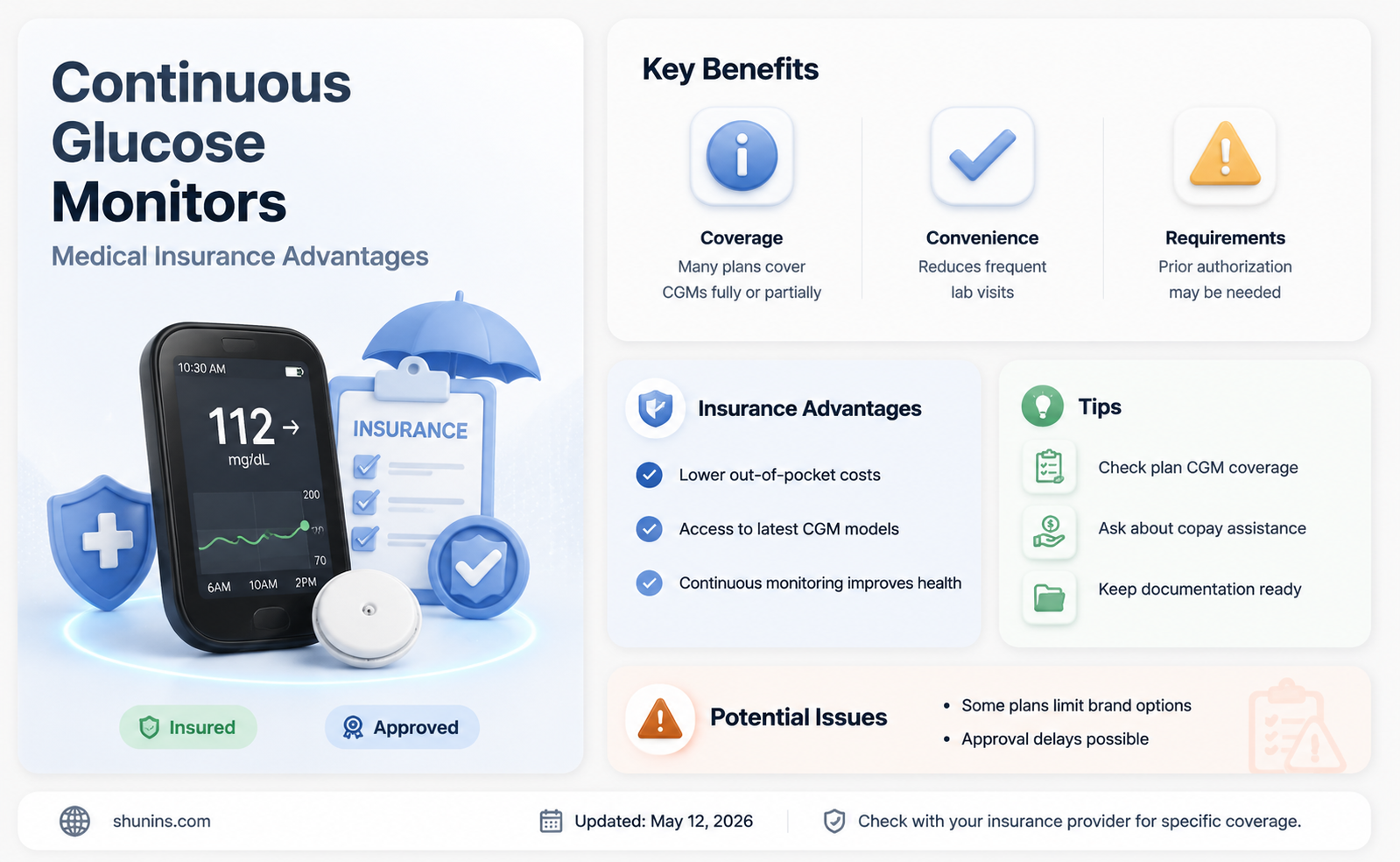

Continuous glucose monitors (CGMs) are essential for effective diabetes management, allowing users to adjust their diet, exercise, and medication in real-time, reducing the risk of complications. While these devices can be costly, many medical insurance plans cover CGMs, including Medicare, Medicaid, and private insurance plans. However, the coverage varies by provider, plan type, and policy terms, and specific eligibility criteria must be met. This article will explore the requirements and processes for getting CGMs covered by different types of medical insurance, including the necessary documentation, preauthorization steps, and potential challenges to obtaining coverage. Understanding these factors is crucial for individuals seeking to access CGMs through their medical insurance plans.

| Characteristics | Values |

|---|---|

| Insurance coverage | Medicare and Medicaid may offer coverage for continuous glucose monitors (CGMs) if you meet certain eligibility criteria. |

| Eligibility criteria | Requirements include having diabetes mellitus, taking insulin or having a history of problems with low blood sugar, and having a prescription for testing supplies and instructions on how often to test your blood glucose. |

| Prescription requirements | A prescription from a qualified healthcare provider is required for insurance coverage. The prescription must include the patient's diabetes diagnosis, medical justification for the device, and the prescribed CGM model. |

| Preauthorization | Most insurance plans require preauthorization before covering a CGM. This involves the healthcare provider submitting a request to the insurer via an electronic portal or faxing a prior authorization form. |

| Costs | Medicare Part B typically covers 80% of the approved costs for CGMs, with the patient responsible for the remaining 20% (coinsurance) after meeting the Part B deductible. Medicaid deductibles, copays, and other out-of-pocket costs are usually very low. |

| Discounts and financial assistance | Financial support for CGMs is available through medical device manufacturers and patient assistance programs. Additionally, using funds in a Health Savings Account (HSA) can help cover costs. |

Explore related products

What You'll Learn

- Continuous Glucose Monitors (CGMs) are covered by Medicare if you meet certain eligibility criteria

- Private/employer-sponsored insurance plans are not required to cover diabetes devices unless mandated by the state or territory

- Insurance coverage for CGMs varies by provider, plan type, and policy terms

- Insurers require itemized invoices listing CGM components, with corresponding billing codes

- Insurers require a prescription from a qualified healthcare provider for insurance coverage

![]()

Continuous Glucose Monitors (CGMs) are covered by Medicare if you meet certain eligibility criteria

Medicare Part B covers CGMs as durable medical equipment with a 20% copayment. If you have a private Medigap plan to supplement your Medicare coverage, it may cover the copayment. To qualify for Medicare coverage for a CGM, you must meet the following eligibility criteria:

- You must have diabetes mellitus (type 1 or type 2 diabetes).

- You must be taking insulin or have a history of problems with low blood sugar (hypoglycemia).

- You must have a prescription for testing supplies and instructions on how often to test your blood glucose.

- You or your caregiver must be trained to use a CGM as prescribed by your doctor.

- Your doctor must confirm that you meet the above criteria and that CGM is medically necessary for you.

- The CGM device must be FDA-approved and purchased from a Medicare-approved supplier.

- You must meet with your doctor in person or through a Medicare-approved telehealth visit within six months before ordering a CGM to evaluate whether your diabetes is being controlled.

It is important to note that Medicare Advantage plans, which are offered by private insurance companies, may also cover CGMs. If you are considering a Medicare Advantage plan, be sure to check with the plan provider to understand their specific coverage and eligibility criteria for CGMs.

In addition, Medicare has been increasing its coverage for CGMs. In April 2023, the Centers for Medicare & Medicaid Services expanded continuous glucose monitor coverage to any Medicare recipient prescribed insulin to treat diabetes, regardless of insulin type or amount. This change made approximately 1.5 million more people eligible for CGM coverage.

Choosing the Right Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Private/employer-sponsored insurance plans are not required to cover diabetes devices unless mandated by the state or territory

Continuous glucose monitors (CGMs) are crucial for effective diabetes management. They allow for immediate adjustments in diet, exercise, and medication, reducing the risk of complications. While CGMs are essential for diabetes care, not all insurance plans cover them.

If your insurance plan does not cover diabetes devices, there are other options to explore. Firstly, you can contact your state insurance department to inquire about insurance requirements and protections in your state. You may also be eligible for special enrollment in other group health coverage, such as a spouse or parent's job-based health plan. Additionally, you can look into financial assistance programs and discounts that can help cover the costs of diabetes devices. For example, GoodRx can help lower the cost of the FreeStyle Libre 2 reader to a maximum of $65 per month for sensors. Furthermore, patient assistance programs may provide free or low-cost diabetes supplies depending on your insurance status and income.

Medical Insurance: Anytime Access and Availability Explained

You may want to see also

Explore related products

![]()

Insurance coverage for CGMs varies by provider, plan type, and policy terms

Insurance coverage for continuous glucose monitors (CGMs) varies depending on the insurance provider, the type of insurance plan, and the specific terms of the policy.

Medicare, a government insurance program for people aged 65 and older, provides broad coverage for CGMs, although there may be some out-of-pocket costs. Medicare Part B, specifically, covers CGMs as durable medical equipment (DME) prescribed by a doctor for home use. After meeting the Part B deductible, individuals typically pay 20% of the approved cost, with Medicare covering the remaining 80%. Medicare Advantage plans, which are provided by private insurance companies, also generally cover diabetes monitoring devices, including CGMs.

Medicaid, on the other hand, varies significantly from state to state. In some states, Medicaid programs do not provide any coverage for CGMs, while in others, coverage is available for individuals with type 1 or type 2 diabetes. As of 2024, 48 states and Washington, D.C., offer some level of CGM coverage for Medicaid beneficiaries. Additionally, all children under the age of 21 enrolled in any Medicaid program can access a CGM through the Early and Periodic Screening, Diagnostic, and Treatment (EPSDT) program.

Private or employer-sponsored insurance plans are not required to cover diabetes devices unless mandated by the state or territory. However, most states require coverage of diabetes monitoring devices under the Affordable Care Act (ACA).

It is important to note that, regardless of the insurance provider, certain eligibility criteria must be met to qualify for CGM coverage. These criteria may include having a documented history of diabetes and a need for frequent glucose monitoring, as verified by a healthcare provider. Additionally, a prescription from a doctor is usually needed to qualify for insurance coverage of a CGM.

To determine specific coverage details, individuals should refer to their insurance plan's benefits document or contact their healthcare provider for assistance.

Medical Insurance Costs: Single Person, Big Expense?

You may want to see also

Explore related products

![]()

Insurers require itemized invoices listing CGM components, with corresponding billing codes

Continuous glucose monitors (CGMs) are crucial for people with diabetes, helping them to track their blood sugar levels in real-time. This enables them to make immediate adjustments to their diet, exercise, and medication, reducing the risk of complications and improving overall health.

CGMs can be expensive, so insurance coverage is important. Many insurance plans cover CGMs, but each insurer has its own specific criteria and approval processes. Medicare Part B, for example, covers CGMs as durable medical equipment (DME) if the patient has diabetes, uses insulin, and meets other criteria. Medicaid also offers coverage for CGMs, but eligibility criteria and specific benefits vary by state. Private insurance plans are required to cover essential health benefits, and most states mandate coverage of diabetes monitoring devices.

To ensure coverage, insurers require detailed documentation and itemized invoices. These invoices must list the CGM components, including transmitters, sensors, and readers, along with their corresponding billing codes. These codes are vital as they align with the insurer's classification of CGMs as either DME or a pharmacy benefit, which affects billing and cost-sharing structures. In addition to the components, the invoice must include the prescribing physician's information, the patient's diagnosis code, and proof of purchase from an approved supplier.

It is important to note that incorrect or missing information on the invoice can lead to claim rejections or delays. Therefore, patients should carefully review the eligibility criteria and documentation requirements of their insurance plan to ensure that their CGM expenses are covered.

Understanding POS Medical Insurance Plans: Hybrid Healthcare Coverage

You may want to see also

Explore related products

![]()

Insurers require a prescription from a qualified healthcare provider for insurance coverage

Continuous glucose monitors (CGMs) are crucial for effective diabetes management. They help users maintain their glucose levels within target ranges, which is essential for long-term health. While CGMs can be costly, there are several options for insurance coverage.

Medicare Part B (Medical Insurance) covers blood glucose (blood sugar) monitors as durable medical equipment (DME) that your doctor prescribes for use in your home. After you meet the Part B deductible, you pay 20% of the Medicare-approved amount. Medicare Advantage plans also cover diabetes monitoring devices. Medicaid also covers CGMs, and deductibles, copays, and other out-of-pocket costs are typically low.

To qualify for insurance coverage, a prescription from a qualified healthcare provider is usually required. This prescription must be deemed medically necessary, and your doctor may need to submit a supporting statement. This process is known as prior authorization, where insurers require approval to control costs. It is important to note that not all medications are covered by insurance, and you may need to explore alternative options or request an exception.

If you are unable to obtain insurance coverage for a continuous glucose monitor, there are other options to consider. You may qualify for free or low-cost diabetes monitoring devices through patient assistance programs, depending on your income. Additionally, medical device manufacturers offer discounts and financial support for CGMs. Using funds from a Health Savings Account (HSA) is another way to cover the costs of a CGM.

Preparing for a Life Insurance Medical Exam: A Quick Guide

You may want to see also

Frequently asked questions

A CGM is a device that helps users maintain their glucose levels within target ranges, which is essential for long-term health.

A prescription from a qualified healthcare provider is required for insurance coverage. The prescription must include the patient's diabetes diagnosis, medical justification for the device, and the prescribed CGM model.

Both Medicare and Medicaid require that you have a documented history of diabetes and a need for frequent glucose monitoring. Your healthcare provider will play a crucial role in documenting this need.

First, you'll need a prescription from your doctor. Then, you'll need to submit a request to the insurer, typically via an electronic portal or by faxing a prior authorization form. The form must include the patient’s diagnosis, prescribed CGM model, and a summary of medical necessity.

If you don’t have insurance or your health plan doesn’t cover a CGM, you may qualify for programs that provide free or low-cost devices. For example, you may qualify for free or low-cost diabetes supplies through patient assistance programs, depending on your insurance status and income.