Credit unions, like banks, are financial institutions that offer a range of services to their members, including savings accounts, loans, and investment opportunities. One common concern among potential members is the safety of their deposits in the event of a credit union failure. To address this, many credit unions are insured by the government, providing a level of protection for members' funds. In the United States, for example, most credit unions are insured by the National Credit Union Administration (NCUA), an independent federal agency that oversees and regulates federal credit unions and insures deposits in both federal and state-chartered credit unions, up to $250,000 per account. This insurance is similar to the Federal Deposit Insurance Corporation (FDIC) insurance provided to banks, ensuring that members' deposits are safe and secure. Understanding the insurance coverage provided by credit unions is essential for anyone considering joining one, as it can provide peace of mind and confidence in the financial institution's stability.

| Characteristics | Values |

|---|---|

| Government Insurance | Yes, credit unions are insured by the government in many countries. |

| U.S. Insurance | Insured by the National Credit Union Administration (NCUA) up to $250,000 per depositor. |

| U.K. Insurance | Covered by the Financial Services Compensation Scheme (FSCS) up to £85,000 per person. |

| Canada Insurance | Protected by Credit Union Deposit Insurance Corporation (CUDIC) or provincial equivalents. |

| Australia Insurance | Covered by the Australian Prudential Regulation Authority (APRA) and state-based schemes. |

| Coverage Limits | Varies by country; typically ranges from $250,000 (U.S.) to £85,000 (U.K.). |

| Type of Accounts Covered | Savings, checking, certificates of deposit, and other eligible accounts. |

| Non-Covered Items | Investments, mutual funds, and certain non-deposit products. |

| Purpose of Insurance | Protects members' funds in case of credit union failure. |

| Comparison to Banks | Similar to FDIC insurance for banks in the U.S. and other national schemes. |

| Global Variations | Insurance schemes differ by country, but most offer government-backed protection. |

Explore related products

What You'll Learn

![]()

NCUA Insurance Coverage Limits

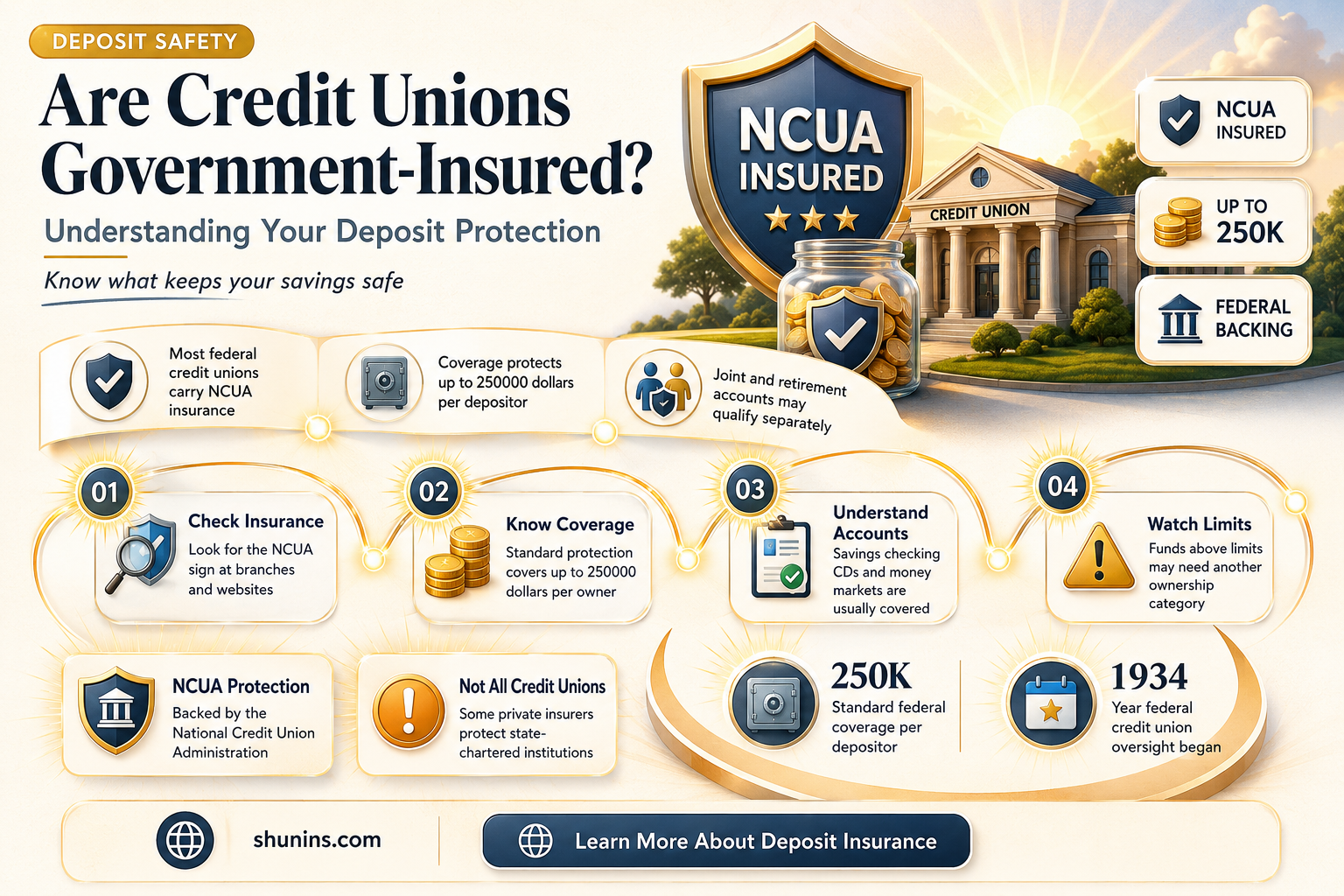

Credit unions in the United States are indeed insured by the government, providing members with protection similar to that offered by the Federal Deposit Insurance Corporation (FDIC) for banks. The National Credit Union Administration (NCUA) is the independent federal agency responsible for insuring deposits in federally insured credit unions. This insurance ensures that members' funds are safe, even in the unlikely event of a credit union failure. Understanding the NCUA insurance coverage limits is crucial for credit union members to maximize their protection.

The NCUA insurance coverage limits are designed to protect members' deposits up to certain amounts. As of the most recent guidelines, the standard insurance coverage is $250,000 per depositor, per insured credit union, for each account ownership category. This means that if you have multiple accounts in the same credit union but under different ownership categories (e.g., individual accounts, joint accounts, retirement accounts), each category is insured separately up to $250,000. For example, if you have an individual account and a joint account with your spouse, both accounts are insured for up to $250,000 each, providing a total of $500,000 in coverage.

It’s important to note that certain types of accounts and ownership structures can qualify for additional coverage. For instance, trust accounts, where one person is named as the owner and one or more beneficiaries are named, can be insured up to $250,000 per beneficiary, provided specific requirements are met. Similarly, business accounts, including sole proprietorships, partnerships, and corporations, are also insured up to $250,000. Understanding these nuances can help members structure their accounts to maximize their insurance coverage.

Another key aspect of NCUA insurance is its applicability to various types of deposits, including checking accounts, savings accounts, money market accounts, and certificates of deposit (CDs). However, it’s essential to recognize that non-deposit products such as stocks, bonds, mutual funds, and life insurance policies are not covered by NCUA insurance. Members should be aware of what is and isn’t protected to make informed financial decisions.

To ensure your deposits are fully insured, it’s advisable to regularly review your account structure and confirm that your credit union is federally insured. You can verify a credit union’s insurance status by using the NCUA’s online tool or by looking for the official NCUA insurance sign at the credit union’s branches. By staying informed about NCUA insurance coverage limits, credit union members can have peace of mind knowing their funds are secure and protected by the federal government.

Borrowing Money: Government Mutual Life Insurance Options

You may want to see also

Explore related products

![]()

FDIC vs. NCUA Differences

When it comes to understanding whether credit unions are insured by the government, it's essential to explore the roles of the Federal Deposit Insurance Corporation (FDIC) and the National Credit Union Administration (NCUA). Both entities provide insurance to protect depositors, but they operate differently and cater to distinct financial institutions. The FDIC primarily insures deposits in banks, while the NCUA provides insurance for credit unions. This distinction is crucial for understanding the safety nets available to consumers.

One of the key FDIC vs. NCUA differences lies in the types of institutions they cover. The FDIC was established in 1933 to restore trust in banks after the Great Depression, and it insures deposits in commercial banks and savings institutions. On the other hand, the NCUA, created in 1970, specifically insures deposits in federally chartered credit unions and those that are federally insured. This means that if you have an account at a bank, your funds are protected by the FDIC, whereas credit union members' deposits are safeguarded by the NCUA.

Another important FDIC vs. NCUA difference is the insurance coverage limits. Both agencies insure deposits up to $250,000 per depositor, per insured bank or credit union, for each account ownership category. This limit was permanently raised from $100,000 to $250,000 in 2010 under the Dodd-Frank Wall Street Reform and Consumer Protection Act. However, the way they manage and oversee their respective institutions differs. The FDIC has a broader regulatory role, including examining and supervising banks, while the NCUA focuses exclusively on credit unions, ensuring they operate safely and soundly.

The funding mechanisms for these agencies also highlight FDIC vs. NCUA differences. The FDIC is funded by premiums that banks pay for deposit insurance, while the NCUA’s National Credit Union Share Insurance Fund (NCUSIF) is capitalized by credit unions through premiums and other sources. Both funds are backed by the full faith and credit of the U.S. government, ensuring that depositors’ funds are secure even in the unlikely event of a bank or credit union failure.

Lastly, the oversight and regulatory frameworks of the FDIC and NCUA differ significantly. The FDIC is an independent agency that works closely with other federal and state regulators to supervise banks, manage receiverships, and address systemic risks. In contrast, the NCUA is an independent federal agency that regulates and insures all federally insured credit unions, focusing on their unique cooperative structure and member-owned model. Understanding these FDIC vs. NCUA differences helps consumers make informed decisions about where to deposit their money, knowing that both banks and credit unions offer government-backed insurance protection.

Prospecting for Life Insurance: Strategies for Success

You may want to see also

Explore related products

![]()

State-Chartered Credit Union Protection

Credit unions, including state-chartered ones, are indeed insured by the government, providing members with a safety net similar to that of traditional banks. For state-chartered credit unions, this protection primarily comes through the National Credit Union Share Insurance Fund (NCUSIF), administered by the National Credit Union Administration (NCUA). The NCUSIF insures deposits in federally insured credit unions, ensuring that members' funds are safe up to $250,000 per share owner, per insured credit union, for each account ownership category. This coverage is backed by the full faith and credit of the U.S. government, giving members confidence in the security of their deposits.

State-chartered credit unions must meet specific criteria to qualify for NCUSIF coverage. They must apply for federal insurance through the NCUA and adhere to federal regulations, even though they are chartered by their respective states. Once insured, these credit unions are subject to regular examinations and oversight by the NCUA to ensure compliance with safety and soundness standards. This dual oversight—by both state regulators and the NCUA—provides an additional layer of protection for members, as it ensures that credit unions maintain strong financial practices.

In addition to federal insurance, some states offer their own deposit insurance programs for state-chartered credit unions. These programs can provide supplemental coverage beyond the $250,000 limit set by the NCUSIF. For example, states like Massachusetts and Ohio have their own insurance funds that may cover additional amounts, offering members even greater peace of mind. However, it’s important for members to verify whether their credit union participates in such state-level programs, as not all state-chartered credit unions opt for this additional coverage.

Members of state-chartered credit unions can easily confirm their institution’s insurance status by looking for the official NCUA insurance sign or verifying their credit union’s status on the NCUA’s website. This transparency ensures that members are aware of the protections in place for their deposits. It’s also worth noting that credit union insurance covers a variety of account types, including savings, checking, money market accounts, and certificates of deposit, providing comprehensive protection for members’ financial assets.

While state-chartered credit unions operate under state laws, their participation in the NCUSIF ensures that they are held to the same federal insurance standards as federally chartered credit unions. This uniformity in protection is a key advantage for credit union members, as it eliminates confusion and ensures consistent safeguards across the industry. Ultimately, state-chartered credit union protection through the NCUSIF and, in some cases, state-level programs, reinforces the safety and reliability of credit unions as financial institutions, making them a secure choice for consumers.

Flu Shot Coverage: What Your Insurance Plan Offers

You may want to see also

Explore related products

![]()

Non-Federally Insured Credit Unions

While most credit unions in the United States are federally insured, there exists a subset known as Non-Federally Insured Credit Unions (NFICUs). These institutions operate without the backing of the National Credit Union Administration (NCUA), the federal agency that insures deposits in federally insured credit unions. Instead, NFICUs may rely on private insurance, state-level insurance programs, or, in some cases, no insurance at all. This distinction is crucial for members, as it directly impacts the safety and security of their deposits.

For members of NFICUs, understanding the insurance coverage—or lack thereof—is essential. Federally insured credit unions provide up to $250,000 in deposit insurance per depositor, per insured credit union, through the NCUA’s National Credit Union Share Insurance Fund (NCUSIF). In contrast, NFICUs may offer private insurance through companies like the American Share Insurance (ASI), which provides similar coverage limits. However, private insurance is not guaranteed by the federal government, and its stability depends on the financial health of the insurer. Members should carefully review the insurance details provided by their NFICU to ensure they understand the level of protection offered.

State-chartered credit unions that are not federally insured may also participate in state-specific insurance programs. These programs vary widely in terms of coverage limits and reliability. For example, some states have their own credit union insurance funds, while others may not offer any insurance at all. Prospective members of NFICUs should research their state’s regulations and the specific insurance arrangements of the credit union they are considering joining. This due diligence is critical to making an informed decision about where to deposit funds.

One of the risks associated with NFICUs is the potential lack of insurance altogether. Some credit unions, particularly smaller or specialized ones, may operate without any deposit insurance. In such cases, members’ funds are not protected against the failure of the credit union. This scenario underscores the importance of thoroughly vetting NFICUs before becoming a member. Members should inquire about the credit union’s financial stability, governance, and risk management practices to assess the safety of their deposits.

Despite the risks, NFICUs can offer unique benefits, such as personalized service, community focus, and specialized financial products. For members who prioritize these advantages and are willing to accept the associated risks, NFICUs can be a viable option. However, it is imperative to weigh these benefits against the lack of federal insurance. Members should also consider diversifying their deposits across multiple institutions to mitigate risk, especially if their chosen NFICU does not provide adequate insurance coverage.

In conclusion, Non-Federally Insured Credit Unions operate outside the federal insurance framework, relying on private, state, or no insurance at all. Members of these institutions must carefully evaluate the insurance arrangements and financial stability of the credit union to protect their deposits. While NFICUs may offer unique advantages, the absence of federal insurance requires members to exercise caution and conduct thorough research before entrusting their funds to these institutions.

How to File a Claim with Globe Life Insurance

You may want to see also

Explore related products

![]()

Credit Union Failure Safeguards

Credit unions, like banks, are subject to various safeguards to protect members' funds in the event of financial failure. One of the primary safeguards is federal insurance, which ensures that members' deposits are protected up to a certain limit. In the United States, credit unions are insured by the National Credit Union Administration (NCUA), an independent federal agency. The NCUA operates the National Credit Union Share Insurance Fund (NCUSIF), which provides insurance coverage of up to $250,000 per share owner, per insured credit union, for each account ownership category. This insurance is backed by the full faith and credit of the U.S. government, providing members with the same level of protection as federal bank deposit insurance.

In addition to federal insurance, credit unions are subject to strict regulatory oversight to minimize the risk of failure. The NCUA regularly examines credit unions to ensure they adhere to safety and soundness standards, maintain adequate capital levels, and follow prudent lending practices. These examinations help identify potential issues early, allowing regulators to take corrective action before a credit union’s financial condition deteriorates. Credit unions are also required to submit regular financial reports, providing transparency and accountability to both regulators and members.

Another critical safeguard is the credit union’s capital structure. Unlike banks, credit unions are member-owned cooperatives, and their members are required to maintain a minimum share balance, which serves as part of the institution’s capital base. This member-focused structure incentivizes prudent management and reduces the likelihood of risky behavior. Additionally, credit unions often have a more conservative lending approach, focusing on serving their local communities and members rather than pursuing high-risk investments.

In the rare event of a credit union failure, the NCUA’s liquidation and merger processes ensure that members’ funds are protected and services continue with minimal disruption. If a credit union is unable to continue operating, the NCUA steps in to manage the liquidation process, paying out insured deposits directly to members or transferring accounts to a healthy credit union. This seamless transition ensures that members retain access to their funds and financial services without significant interruption.

Lastly, credit unions often participate in state-level insurance programs in addition to federal coverage, providing an extra layer of protection in some cases. However, the primary safeguard remains the NCUA’s federal insurance, which is universally available to all federally insured credit unions. Members can verify their credit union’s insured status by looking for the official NCUA insurance sign or checking the NCUA’s online database. These combined safeguards make credit unions a safe and reliable option for managing personal finances, offering government-backed protection comparable to that of traditional banks.

Share Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Yes, credit unions are insured by the National Credit Union Administration (NCUA), which is a federal agency.

NCUA insurance covers up to $250,000 per depositor, per insured credit union, for each account ownership category.

Yes, NCUA insurance for credit unions is comparable to FDIC insurance for banks, offering the same level of protection for depositors.

If a credit union fails, the NCUA will step in to ensure depositors receive their insured funds, up to the coverage limit, typically within a few days.