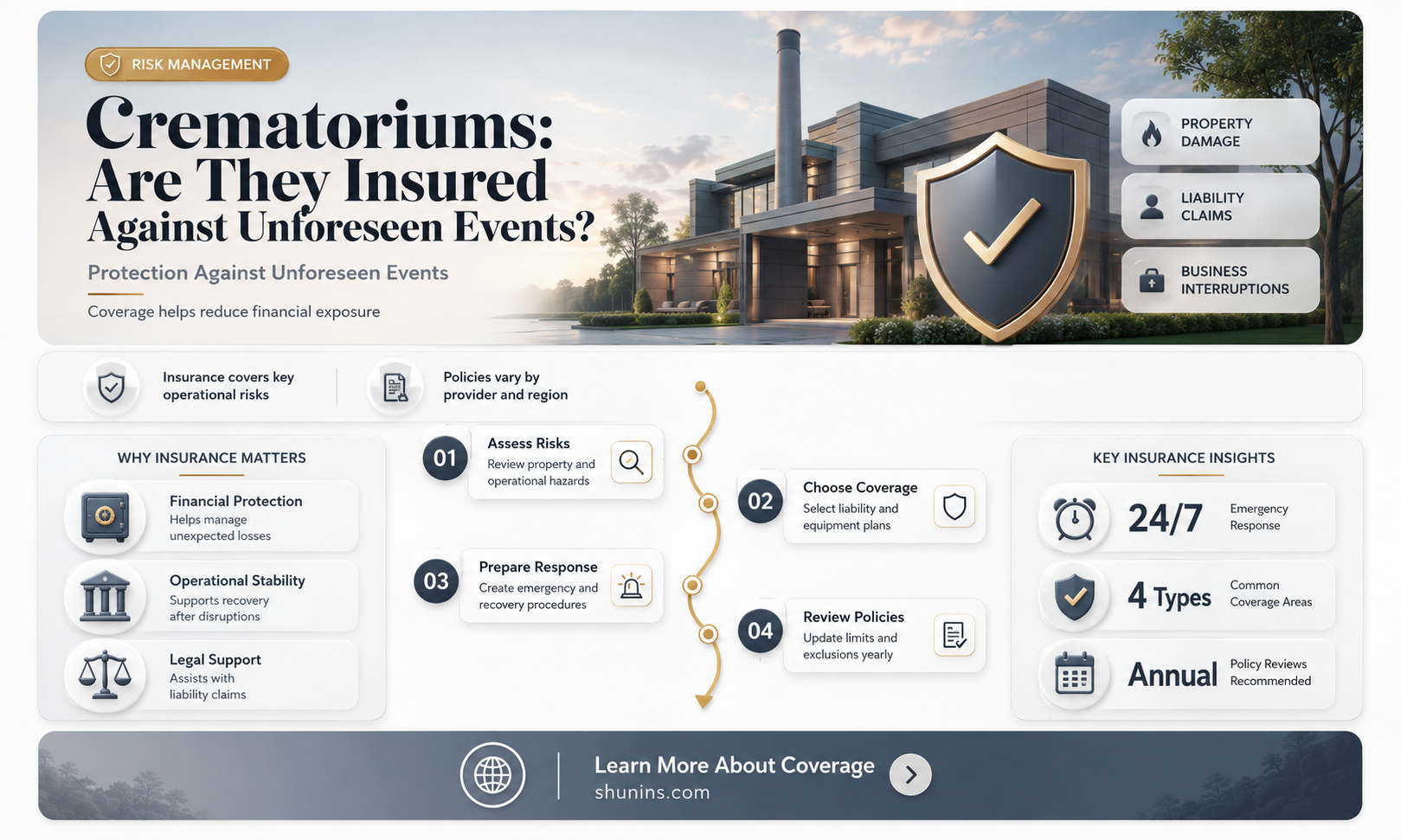

Crematoriums and funeral homes are businesses that face a variety of risks and require insurance to protect them from financial losses. These risks include fire, floods, earthquakes, theft, vandalism, lawsuits, and employee injuries. There are several types of insurance policies that crematoriums can purchase to mitigate these risks, including commercial property insurance, workers' compensation insurance, commercial auto insurance, cyber liability insurance, and various liability insurance policies. These insurance policies can provide coverage for property damage, injuries, cyber-related incidents, and lawsuits, among other potential issues. It is important for crematorium owners to carefully consider their specific risks and needs when selecting insurance policies to ensure adequate protection for their business.

| Characteristics | Values |

|---|---|

| Type of insurance | Commercial Property Insurance, Commercial Auto Insurance, Cyber Liability Insurance, Workers' Compensation Insurance, General Liability Insurance, Premises Liability Insurance, Professional Liability Insurance |

| Purpose | Protect crematoriums from financial losses due to fire, floods, earthquakes, natural disasters, theft, vandalism, cyber-attacks, employee injuries, lawsuits, etc. |

| Cost | Varies depending on the amount of commercial property and company vehicles insured, and the business's prior claims history |

| Payout | Covers cremation costs and other end-of-life expenses; paid directly to beneficiaries who can use the money flexibly |

| Coverage | Coverage limits vary across policies; typically includes cremation and related funeral expenses |

Explore related products

What You'll Learn

![]()

Commercial Property Insurance

In addition to property damage, commercial property insurance can also encompass liability coverage. General liability insurance protects crematoriums and funeral homes from lawsuits arising from property damage, errors, or oversight in their services. This includes instances where a family sues due to their loved one being mistakenly cremated or cases of incorrect remains being provided to survivors. Liability insurance helps cover legal costs and provides financial protection in the event of a lawsuit.

Furthermore, commercial property insurance can be tailored to the unique needs of crematoriums and funeral homes. For example, businesses that use vehicles for processions or transportation may require commercial auto insurance. This type of coverage protects against injuries or damages caused by company vehicles, including hearses and other specialised vehicles used in funeral services. By having adequate commercial auto insurance, businesses can mitigate the risk of substantial financial losses in the event of accidents or vehicle-related incidents.

Overall, commercial property insurance plays a vital role in safeguarding crematoriums and funeral homes from potential risks and financial losses. By investing in comprehensive coverage, businesses can protect their assets, mitigate disruptions, and ensure they can continue serving their communities without incurring significant expenses due to unforeseen events or liabilities.

Life Insurance and SSDI: Any Conflict?

You may want to see also

Explore related products

![]()

Workers' Compensation Insurance

Crematoriums, like any other business, need to be insured against a variety of risks. Workers' Compensation Insurance is one of the key types of insurance that crematoriums should carry. This type of insurance covers expenses related to employee injuries, illnesses, or deaths that occur as a result of the work environment or job duties. It ensures that employees will have their medical care and lost wages covered and can also provide financial support to the families of deceased employees.

In some states, it is a legal requirement for crematoriums to carry Workers' Compensation Insurance. For example, in New Mexico, funeral homes and crematoriums are legally required to have this type of insurance to cover employee injuries incurred on the job. However, the specific provisions and requirements of Workers' Compensation Insurance can vary from state to state, and even between insurers and policies.

The risks associated with working in a crematorium include burns from the use of furnaces, as well as other types of injuries such as tripping, falling down stairs, or straining muscles from heavy lifting. These risks can be mitigated with proper safety measures, but accidents can still occur, and Workers' Compensation Insurance provides essential coverage in these instances.

In addition to Workers' Compensation Insurance, there are several other types of insurance that crematoriums should consider. These include Commercial Property Insurance, Cyber Liability Insurance, Employment Practices Liability Insurance (EPLI), Commercial Auto Insurance, and Crime Insurance. Each of these types of insurance provides coverage for different risks, such as property damage, cyber incidents, employee lawsuits, vehicle accidents, and theft or dishonesty, respectively. By having a comprehensive insurance package in place, crematoriums can protect themselves financially and legally in the event of unforeseen incidents.

Lincoln Financial Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Commercial Auto Insurance

Crematoriums and funeral homes in New Mexico are advised to invest in Commercial Auto Insurance to protect their vehicles and drivers. This type of insurance is designed for businesses that use vehicles for work-related purposes and offers more extensive coverage than a personal auto insurance policy.

Businesses that commonly require Commercial Auto Insurance include contractors, landscapers, construction companies, delivery services, transportation services, and food services. Even businesses that use vehicles for errands or client transportation, such as shops and restaurants, may need this type of insurance. It's important to note that personal auto insurance usually does not extend to business usage, leaving companies vulnerable without the proper commercial coverage.

The cost of Commercial Auto Insurance can vary depending on several factors, including the business's location, the number and types of vehicles, and the driving records of the employees operating them. It's recommended to get a quote from insurance providers to find the most suitable coverage for your business needs.

By investing in Commercial Auto Insurance, businesses can protect themselves from unexpected expenses and ensure their vehicles are covered for work-related usage. This type of insurance is an essential consideration for any company that relies on vehicles as part of its operations.

Asurea and Globe Life Insurance: What's the Connection?

You may want to see also

Explore related products

![]()

Cyber Liability Insurance

Crematoriums and funeral homes are businesses fraught with unique risks, from professional liability to property damage, and even cyber threats. As such, it is important to secure comprehensive insurance coverage to protect against financial losses and business interruptions.

One type of insurance that crematoriums should consider is Cyber Liability Insurance. This type of insurance provides financial protection in the event of a data breach or other cyber-related incidents that expose sensitive information and put customer and employee privacy at risk. It can help cover the costs associated with legal fees, notification expenses, credit monitoring services, and other related costs. For example, if a crematorium's systems are hacked and personal data is stolen, Cyber Liability Insurance can help cover the costs of notifying affected individuals, providing credit monitoring services, and defending against any legal claims arising from the breach.

Additionally, crematoriums should be aware that cyber threats are constantly evolving, and the impact of a cyber-attack can be devastating. Without adequate Cyber Liability Insurance, businesses may be left vulnerable to significant financial losses and may struggle to recover.

By investing in Cyber Liability Insurance, crematoriums can mitigate the financial risks associated with cyber-attacks and data breaches, ensuring that they can continue serving their customers and protecting sensitive information. This type of insurance is an important component of a comprehensive insurance package for any crematorium, helping to safeguard against the unique challenges posed by the digital age.

Gold Star Families: Life Insurance Coverage Explained

You may want to see also

Explore related products

![]()

General Liability Insurance

Crematoriums face a variety of risks, including fires, theft, vandalism, and lawsuits. As such, they require a range of insurance policies to protect their business and their customers.

One such insurance policy is General Liability Insurance. This type of insurance covers bodily injury and property damage to others (slip and fall incidents) that occur on the premises. For example, if a visitor to the crematorium trips and falls, injuring themselves, General Liability Insurance will cover the costs of any subsequent legal proceedings. General Liability Insurance also protects against property damage that may occur during the cremation process. For instance, if a furnace overheats and causes a fire, this insurance will cover the costs of repairs and replacement of any contents that are ruined.

In addition to General Liability and Professional Liability Insurance, crematoriums may also require Commercial Auto Insurance, Workers' Compensation Insurance, Cyber Liability Insurance, and Employment Practices Liability Insurance (EPLI). Commercial Auto Insurance protects businesses from costs associated with injuries or damages caused by company vehicles, such as hearses. Workers' Compensation Insurance covers expenses related to employee injuries or illnesses caused by the work environment or job duties, such as burns from furnaces or trips and falls. Cyber Liability Insurance provides financial protection in the event of a data breach or cyber-related incident that exposes sensitive information. Finally, EPLI covers employers in the event they are sued by employees or former employees for wrongful termination, discrimination, sexual harassment, or civil rights violations.

Term or Life Insurance: Which is the Better Option?

You may want to see also

Frequently asked questions

It is a type of life insurance policy designed to cover the costs of cremation and related funeral expenses. This insurance provides financial assistance to the policyholder's beneficiaries to ensure that the costs of cremation, a memorial service, and any other final expenses are covered.

Cremation insurance covers the costs of cremation, saving your loved ones from unexpected financial losses. It also covers related funeral expenses, providing financial relief to beneficiaries.

Most cremation insurance policies do not require extensive medical exams, making them more accessible to older individuals or those with health issues. The policyholder designates beneficiaries who will receive the insurance payout to cover the cremation and associated costs. The payout can be used for any end-of-life expenses, not just cremation.

Funeral homes and crematoriums require insurance to protect their businesses from various risks. This includes commercial property insurance to cover losses caused by natural disasters, theft, or vandalism. They may also need commercial auto insurance to protect their vehicles and employees from injuries or damages.

In addition to general liability insurance, funeral homes and crematoriums may require professional liability insurance. This covers incidents when a third party sues the business for professional services, such as following the chain of identification of cremated remains. Cyber Liability Insurance is another option that provides financial protection in the event of a data breach or cyber-related incident.