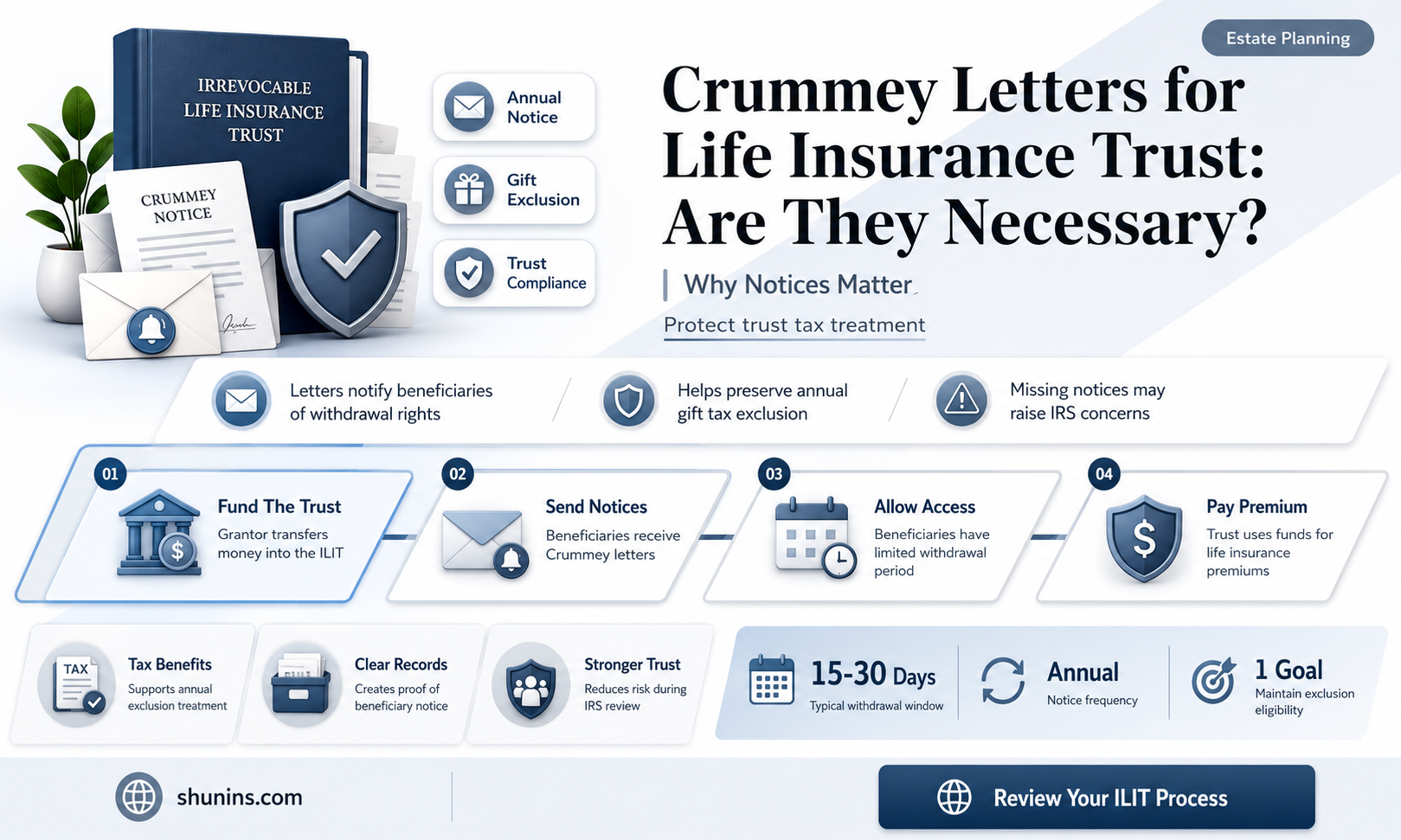

Crummey letters are an important consideration for anyone looking to set up an Irrevocable Life Insurance Trust (ILIT). An ILIT is a tool for estate planning that can help avoid hefty federal taxes on high-value life insurance policies. When a grantor places funds into an ILIT to cover insurance premiums, this is considered a gift to the trust's beneficiaries, and without the proper documentation, this gift may be taxable. This is where Crummey letters come in. A Crummey letter is a notice sent to the beneficiaries of an ILIT, informing them of their right to withdraw the gifted funds within a specified time frame, typically 30 days. While beneficiaries have the option to withdraw the funds, doing so may cause the insurance policy to lapse, which is counter to the purpose of the trust. By sending out these letters, the trustee of the ILIT ensures that the gift qualifies for the annual gift tax exclusion, and the beneficiaries are made aware of their rights.

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UL320_.jpg)

What You'll Learn

![]()

Crummey Letters and Irrevocable Life Insurance Trusts (ILIT)

Irrevocable Life Insurance Trusts (ILIT) are a type of estate planning tool that can help high-net-worth individuals avoid hefty federal estate taxes on their life insurance policies upon their death. An ILIT is specifically designed to own life insurance policies, ensuring that the value of these policies is not included in an individual's estate and thus reducing their estate tax liability.

To fund an ILIT, an existing life insurance policy can be transferred into the trust, or the trust can purchase a new policy directly. It's important to note that an ILIT must be irrevocable, meaning that once funded, the grantor relinquishes all rights and ownership interests in the trust and can no longer make changes to it. Additionally, the grantor cannot serve as the trustee of an ILIT to avoid "incidents of ownership," which would result in the IRS including the trust assets in their estate.

Now, what do Crummey Letters have to do with all of this? When the grantor of an ILIT places funds into the trust to pay the insurance premiums, the beneficiaries are considered to be receiving a "gift." To qualify this contribution as a "tax-free gift" under the $15,000 gift tax exclusion, it must be a present gift with the beneficiary having immediate and unrestricted access to the funds. This is where Crummey Letters come into play.

A Crummey Letter is a physical letter sent to the beneficiaries of an ILIT, informing them that a gift has been made to the trust and that they have the right to withdraw their share of the gift within a specified time frame, typically 30 to 60 days. This letter essentially converts a future gift into a present gift by giving the beneficiaries immediate access to the funds. If the beneficiaries choose to exercise their "Crummey Power" and withdraw the funds, the insurance policy may lapse due to non-payment of premiums. However, if they do not withdraw the funds, the contribution will be used to pay the policy premium.

To qualify for the gift tax exclusion, beneficiaries must be informed of their right to withdraw each time a contribution is made to the ILIT. Therefore, sending Crummey Letters is a crucial step in the process of maintaining an ILIT and ensuring that premium payments are tax-free.

Life Insurance Annual Charges: What You Need to Know

You may want to see also

Explore related products

![]()

Crummey Letters and Tax Exemptions

Crummey Letters are an important component of wealth management plans that can help avoid extraneous taxation on sums gifted to beneficiaries of an irrevocable trust. They are named after Reverend D. Clifford Crummey, who, along with his children, argued that the sums gifted to his children's trusts should not be subject to gift taxes. The case, Crummey v. Commissioner, established the concept of Crummey Power and the use of Crummey Letters.

Understanding Crummey Power

Crummey Power refers to the ability of beneficiaries to withdraw contributions to a trust at will, converting a future interest gift to a present interest gift. This right is typically limited to a specific period (often 30, 45, or 60 days) and an amount equal to the current annual gift tax exclusion. If the beneficiary does not exercise this right, the Crummey Power lapses, and the assets remain in the trust.

The Role of Crummey Letters

Crummey Letters are formal letters sent to the beneficiaries of an irrevocable trust, informing them of a gift to the trust and their right to withdraw their share immediately and without restriction. This letter changes what would be a future gift into a present gift, allowing the gift to qualify for the annual gift tax exclusion. The letter also specifies a time period for withdrawal, usually 30 days, after which the option lapses, and the contribution is used to pay the policy premium.

Importance of Crummey Letters for Tax Exemptions

Crummey Letters are essential for tax exemptions because they serve as proof that beneficiaries were aware of their right to withdraw funds. Without this documentation, the gift may not be considered tax-exempt. By sending annual Crummey Letters, trustors or trustees can reduce the likelihood of further IRS investigation and potential additional taxation.

Best Practices for Crummey Letters and Tax Exemptions

To ensure compliance with IRS requirements and maximize the chances of tax exemption, it is recommended to:

- Send Crummey Letters annually with a withdrawal period of at least 30-60 days prior to the policy lapsing.

- Encourage beneficiaries to allow the withdrawal period to lapse without acting, rather than proactively notifying the trustee of their decision not to exercise their withdrawal rights.

- Avoid any agreement or implication that beneficiaries should not or will not exercise their withdrawal power.

- Ensure there is sufficient cash in the trust to fulfill potential beneficiary distributions during the entire withdrawal period.

- Do not allow the grantor to pay annual insurance premiums directly; instead, the trust should make all premium payments.

- Provide written notification of withdrawal powers using methods that can prove the mailing date, such as certified mail.

- Specify a withdrawal period of at least 30 days in the trust document to give the beneficiary sufficient time to consider their decision.

Whole Life Insurance: A Child's Smart Investment Strategy?

You may want to see also

Explore related products

![]()

Crummey Notices and Estate Planning

A Crummey notice is a letter sent to the beneficiary of a trust, informing them that assets have been added to the trust and that they have the right to withdraw those assets. The notice should also include a deadline by which the assets must be withdrawn, after which they become the property of the trust.

The purpose of a Crummey notice is to ensure that beneficiaries of a trust understand their rights and are given the opportunity to exercise their "Crummey power", or their right to withdraw assets from the trust. This right is especially important in the case of irrevocable trusts, where beneficiaries may only have a limited time window, such as 30 to 60 days, to withdraw funds once they are deposited.

The Crummey power is derived from a landmark tax case in 1968, where the courts ruled in favor of the Crummey family and established that a gift to a trust could be treated as a "present interest" gift, even if the beneficiary's access to the gift is restricted until a future date or event. This ruling allows gifts to trusts to qualify for the annual gift tax exclusion, as long as the beneficiary is given immediate access to the gift (unless they are a minor under the age of 18).

To maintain the tax-exempt status of contributions to a trust, it is important that Crummey notices are sent out each time a contribution is made. Failure to send a Crummey notice when a contribution is made could result in the IRS deciding that the amounts do not qualify for exemption from the annual gift tax, leading to taxes and penalties.

In the case of irrevocable life insurance trusts (ILITs), beneficiaries typically ignore the Crummey notice and forego their ability to withdraw assets. This is because the funds in an ILIT are intended to be used to pay the premiums on a life insurance policy that will ultimately pay out a considerable sum of money to the beneficiaries after the settlor's death. Withdrawing the assets through the Crummey power would go against the purpose of the trust and could result in the policy premiums going unpaid and the policy lapsing.

Life Insurance Application: Location, Location, Location?

You may want to see also

Explore related products

![]()

Crummey Letters and Trustee Responsibilities

Crummey Letters are an important part of the process when it comes to irrevocable trusts and life insurance policies. Trustees have a set of responsibilities to fulfil when it comes to Crummey Letters, and it is important to understand the role they play in estate planning.

A Crummey Letter is a formal letter sent to the beneficiaries of an irrevocable trust, informing them that a gift has been made to the trust. This gift is typically a contribution to the trust's life insurance policy premium. The letter also informs the beneficiaries that they have the immediate right to withdraw those funds. This right is usually limited to a certain time period, often 30 to 60 days.

Crummey Letters are important because they change a "future gift" into a "present gift". By giving the beneficiaries immediate access to the funds, the gift qualifies for the annual gift tax exclusion. This helps to reduce the taxable value of an estate, which can be particularly beneficial for high-wealth families.

Trustee Responsibilities

The Trustee of an Irrevocable Life Insurance Trust (ILIT) has several key responsibilities when it comes to Crummey Letters:

- The Trustee should have a tax identification number and set up a checking account for the trust.

- They are responsible for sending out the Crummey Letters to the beneficiaries, informing them of their right to withdraw the funds.

- Trustees must ensure that Crummey Letters are sent out promptly after a gift is made to the trust.

- They should also keep clear and detailed records, including signed Crummey Letters, dates, and amounts involved. These records demonstrate that the Trustee has fulfilled their fiduciary duty and can be important for tax purposes.

- Trustees should also be mindful of the timing of gifts and ensure that contributions are not made too late in the year.

- It is important for Trustees to stay updated on tax law changes and how they may impact the trust and the process of sending Crummey Letters.

- Finally, Trustees should maintain confidentiality between beneficiaries and respect their decisions regarding withdrawals.

Chlamydia and Life Insurance: Does It Affect Your Premiums?

You may want to see also

Explore related products

![]()

Crummey Powers and Beneficiary Rights

Crummey powers are an important aspect of estate planning and can offer significant tax benefits to individuals looking to build a trust fund for their beneficiaries while maintaining the ability to claim yearly tax exemption benefits. The concept of Crummey powers originated in the 1960s with D. Clifford Crummey, a wealthy grantor who wanted to create a trust fund for his children while maximising tax benefits.

A Crummey trust, also known as a Crummey provision or Crummey power, is a trust structure that allows gifts to be made in a way that qualifies for exclusion from gift and estate taxes. Typically, gifts made into a trust that the beneficiary will have access to in the future do not qualify for the annual gift tax exclusion, as they are considered "future interests" rather than "present interests". However, a Crummey trust gets around this by offering the beneficiary a limited window of time, usually 30 to 60 days, to take immediate control of the gift. This transforms the gift into a "present interest", making it eligible for the annual gift tax exclusion.

The process of exercising Crummey powers involves sending a Crummey letter to the beneficiaries of an irrevocable trust, informing them of a gift made to the trust and their right to withdraw their share within a specified time frame. This letter serves to change a future gift into a present gift by giving beneficiaries immediate access to the funds. While beneficiaries technically have the right to withdraw the contribution, doing so may cause the insurance policy to lapse, as the funds are intended to pay the policy premiums. Therefore, most grantors hope that beneficiaries will refrain from withdrawing their share.

To qualify for the gift tax exclusion, it is important to follow certain procedures. The trustee of the trust should have a tax identification number and set up a separate checking account. Additionally, beneficiaries must be notified of their right to withdraw each time a contribution is made to the trust. This notification can be in the form of a Crummey letter, which serves as written proof that notice was given. It is also crucial that there is no agreement, express or implied, between the trustee or grantor and the beneficiaries that the withdrawal power will not be exercised.

In summary, Crummey powers and beneficiary rights are essential components of effective estate planning, allowing individuals to maximise tax benefits while providing for their beneficiaries. By understanding and utilising Crummey powers, individuals can ensure that their gifts are structured in a tax-efficient manner, preserving their wealth for future generations.

Clinical Trials: Are You Covered by Life Insurance?

You may want to see also

Frequently asked questions

A Crummey letter is a letter sent to the beneficiaries of an irrevocable trust, informing them that a gift has been made to the trust and that they have the immediate and unrestricted right to withdraw those assets.

A Crummey letter changes what would be a future gift into a present gift by giving the beneficiary an immediate and present interest in the gift. This allows the contribution to qualify for the gift-tax exemption.

Yes, Crummey letters are required for life insurance trusts, specifically irrevocable life insurance trusts (ILITs). The letters inform the beneficiaries of their right to withdraw assets, which is necessary for the contribution to qualify as a "tax-free" gift.

A Crummey letter should include information about the gift made to the trust, the beneficiary's right to withdraw the gift, and a deadline or time period within which the withdrawal must be made.

Crummey letters should be sent out annually and with enough time to allow for the beneficiary's right to withdraw to lapse before the premium payment is due. It is recommended to send the letters at least 45 days in advance of the premium payment.