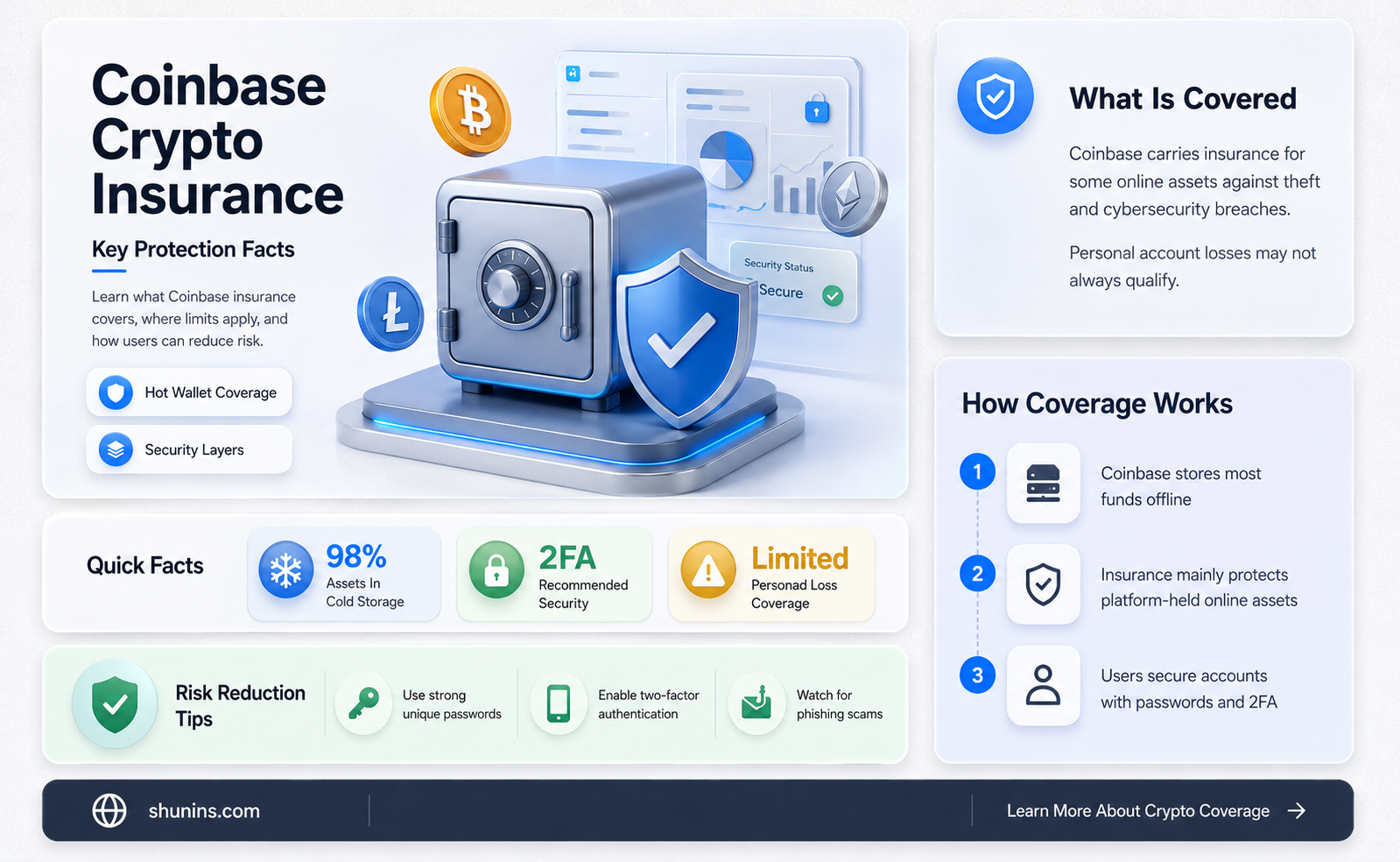

Coinbase has a $255 million insurance program for customers' cryptocurrency holdings. The policy, facilitated through Lloyd's of London, covers losses due to hacking, insider theft, and fraudulent transfers. However, it's important to note that Coinbase is not an FDIC-insured bank, and digital currencies are not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or the Securities Investor Protection Corporation (SIPC). While Coinbase will endeavour to make customers whole in the event of a covered security event, total losses may exceed insurance recoveries, leaving funds at risk. For non-US customers, funds are held separately from Coinbase funds in dedicated custodial accounts, and Coinbase does not use these funds for corporate purposes.

| Characteristics | Values |

|---|---|

| Insured by FDIC | No |

| Insured by NCUSIF | No |

| Insured by SIPC | No |

| Crypto insured | No |

| Insurance for customers' money | Yes |

| Insurance provider | Lloyd's of London |

| Insurance limit | $255 million |

| Insurance type | Hot wallet policy |

| Insurance coverage | Losses due to hacking, insider theft, and fraudulent transfers |

| Pass-through insurance coverage limit | $250,000 per depositor |

Explore related products

What You'll Learn

![]()

Coinbase's $255 million insurance policy

Coinbase has a $255 million insurance policy that covers losses in customers' hot wallets due to hacking, insider theft, and fraudulent transfers. This policy also includes fiat currency and physical damage or theft of private key data in cold storage.

Coinbase's insurance policy is an important development in the opaque crypto market, where policies are generally written to exchanges or custodians rather than the owners of the cryptocurrency. The company's vice president of security, Philip Martin, has emphasised the need for "'value in flight' insurance, which covers digital assets that are essentially online and vulnerable to potential hacks. This type of insurance is particularly relevant in bull markets, where asset prices can move faster than insurance policy limits can grow.

It is important to note that Coinbase's crime insurance policies do not cover any losses resulting from unauthorised access to personal or business accounts due to a breach or loss of credentials. Additionally, digital currencies held on Coinbase are not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC), the National Credit Union Share Insurance Fund (NCUSIF), or the Securities Investor Protection Corporation (SIPC). While Coinbase endeavours to make customers whole in the case of a security event covered by their insurance policies, total losses may still exceed insurance recoveries, leaving funds at risk.

Coinbase maintains custodial accounts at FDIC-insured banks or NCUSIF-insured credit unions, allowing the company to make pass-through insurance claims for each customer up to a certain limit (currently $250,000 per depositor). This pass-through insurance protects funds held on behalf of Coinbase customers against the risk of loss if the insured financial institutions where the custodial accounts are maintained fail.

Incorporate Third Parties in Your Life Insurance Policy

You may want to see also

Explore related products

![]()

Crypto vs. cash balances

Coinbase is not an FDIC-insured bank, and digital currency is not insured or guaranteed by the Federal Deposit Insurance Corporation ("FDIC"), the National Credit Union Share Insurance Fund ("NCUSIF"), or the Securities Investor Protection Corporation ("SIPC"). However, for U.S. customers, Coinbase combines cash balances with those of other customers and holds those funds in custodial accounts at U.S. financial institutions or invests them in liquid U.S. Treasuries, money market funds, or other permissible investments. For non-U.S. customers, funds are held as cash in dedicated custodial accounts separate from Coinbase funds.

For U.S. customers, Coinbase's custodial accounts are FDIC-insured or NCUSIF-insured, offering protection up to $250,000 per depositor. This pass-through insurance protects funds against the risk of loss if any insured financial institutions where Coinbase maintains custodial accounts fail. It is important to note that this insurance covers cash balances and not the crypto itself.

Coinbase provides a "`hosted` wallet service, where they hold your crypto on your behalf. This means you don't have to manage your private keys, and you can easily make basic crypto transactions through Coinbase. However, some users prefer self-custody wallets, where they have complete control over their assets and private keys. Self-custody wallets, such as the Coinbase Wallet, serve as a gateway to various crypto applications and allow users to interact with multiple blockchains.

While Coinbase may be considered one of the safer exchanges to leave your money, it is important to understand the risks involved. In the event of the company going out of business, users may lose their crypto and money stored on the platform. Therefore, some individuals choose to use a combination of exchanges and private wallets to balance convenience and security.

Punitive Damages in North Carolina: Are They Insurable?

You may want to see also

Explore related products

![]()

Pass-through insurance

Coinbase is not an FDIC-insured bank, and digital currency is not insured or guaranteed by the Federal Deposit Insurance Corporation ("FDIC"), the National Credit Union Share Insurance Fund ("NCUSIF"), or the Securities Investor Protection Corporation ("SIPC"). However, Coinbase offers pass-through FDIC or NCUSIF insurance for its customers' funds.

For U.S. customers, Coinbase combines customer balances with the balances of other customers and holds those funds in custodial accounts at U.S. financial institutions or invests them in liquid U.S. Treasuries, USD-denominated money market funds, or other permissible investments in accordance with state money transmitter laws. These custodial accounts are maintained in a manner that allows Coinbase to make a claim against pass-through FDIC or NCUSIF insurance for each customer up to the per-depositor coverage limit, which is currently $250,000 per depositor.

It is important to note that pass-through insurance coverage does not apply to non-U.S. customers, as their funds are held separately from Coinbase funds in dedicated custodial accounts. While Coinbase will not use these funds for its operating expenses or any other corporate purposes, they are not insured in the same way as U.S. customer funds.

Whole Life Insurance: Tax-Deferred Benefits Explained

You may want to see also

Explore related products

![]()

Cold storage

Coinbase is not an FDIC-insured bank and digital currency is not insured or guaranteed by the Federal Deposit Insurance Corporation (“FDIC”), the National Credit Union Share Insurance Fund (“NCUSIF”), or Securities Investor Protection Corporation (“SIPC”). However, in the case of a security event covered by Coinbase's crime insurance policies, they will endeavour to compensate customers, although total losses may exceed insurance recoveries. For U.S. customers, Coinbase combines customer balances with funds from other customers and its own contributions for operational reasons. These funds are then held in custodial accounts at U.S. financial institutions or invested in liquid U.S. Treasuries, USD-denominated money market funds, or other permissible investments.

Hot wallets, or software wallets, are connected to the internet and are commonly used by those new to cryptocurrencies due to their ease of use and accessibility. They are typically installed on devices like smartphones or laptops and generate seed phrases and store private keys online. While this online presence makes transactions straightforward, it also raises security concerns, as there is no way of knowing if the seed phrase and private keys remain secret.

The choice between hot and cold wallets depends on individual needs and preferences. Those who frequently transact with cryptocurrencies may prefer the convenience of hot wallets, while those seeking long-term storage and higher security may opt for cold wallets. A combination of both can also be used, with a hot wallet for regular transactions and small amounts of cryptocurrencies, and a cold wallet for storing larger amounts for the long term.

How Life Insurance Sales Can Make You Rich

You may want to see also

Explore related products

![]()

Crypto insurance challenges

Crypto insurance is a way to protect yourself and recover financial losses if your digital currencies are lost or stolen. It provides protection against losses that can occur from exchange breaches, hacks, or theft. Crypto insurance is funded by a premium, which is the payment a policyholder makes for coverage. These premiums automatically compensate investors if a loss occurs.

However, there are challenges associated with crypto insurance. Cryptocurrency is not considered an established asset class challenging traditional investments, especially in the eyes of the insurance market. There is a lack of regulatory clarity for digital assets, which is essential for investor protection. The high rates of fraud in the digital assets space and its use as a ransomware payment method also contribute to an apprehensive insurance market.

Additionally, there is a debate over whether cryptocurrency is a security or a commodity, leading to regulatory discussions between the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) in the US. The volatile and highly-regulated nature of the cryptocurrency market also poses challenges for insurance providers when assessing risk and creating custom plans.

Coinbase, for example, is not an FDIC-insured bank, and digital currency on the platform is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC). However, Coinbase does have crime insurance policies and maintains accurate records to allow for pass-through FDIC or NCUSIF insurance for each customer up to a certain limit. While Coinbase may endeavour to make users whole in the event of a security breach, total losses may exceed insurance recoveries, and funds may still be at risk.

First-to-Die Life Insurance: Whole Life Coverage for Couples

You may want to see also

Frequently asked questions

Coinbase has a $255 million insurance program for customers' cryptocurrency holdings. The policy is underwritten by Lloyd's of London and covers losses due to hacking, insider theft, and fraudulent transfers. However, it's important to note that Coinbase is not an FDIC-insured bank, and digital currency is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC).

Coinbase has a $255 million hot wallet policy to cover losses due to hacking, insider theft, and fraudulent transfers. The policy is in place to protect customers' cryptocurrencies held at the exchange from losses.

Yes, Coinbase offers Specie coverage for physical damage or theft of private key data in cold storage. This type of insurance covers the costs associated with incident response and protects against losses in cold storage.