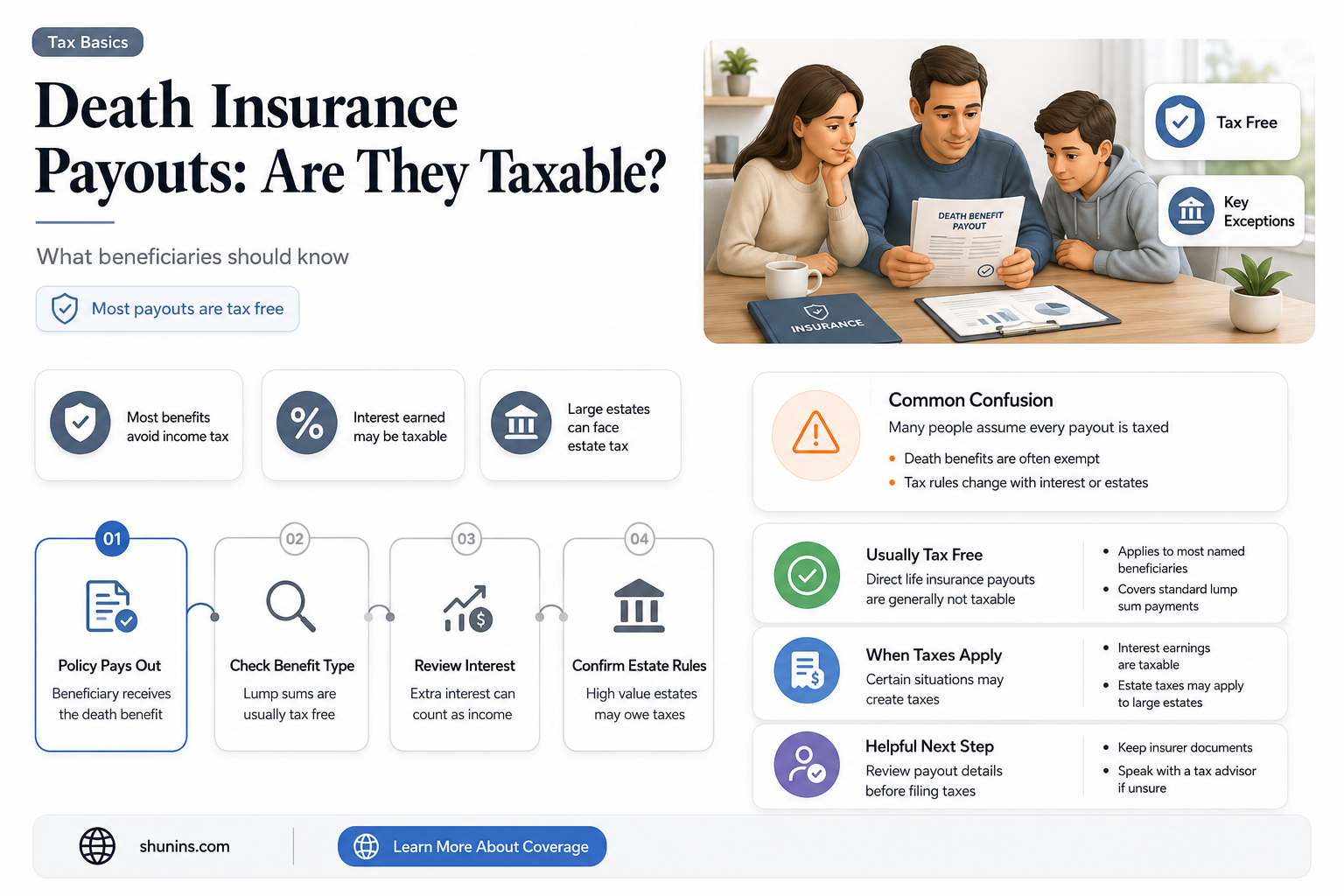

Life insurance payouts are generally not taxable, but there are some exceptions. For example, if the payout has accumulated interest, taxes are usually due on the interest. If the payout is received in instalments, the interest accrued is taxable. If the payout exceeds the federal estate tax threshold of $12.92 million, estate taxes must be paid on the proceeds over the allowed limit. If the policy was transferred for cash or other valuable consideration, the exclusion for the proceeds is limited to the sum of the consideration paid.

Explore related products

$16.56 $19.95

$15.45 $14.95

What You'll Learn

![]()

Life insurance payouts are generally tax-free

Generally, life insurance payouts are not taxable. The death benefit is typically paid directly to the beneficiaries tax-free. However, there are some exceptions to this rule.

Firstly, if the beneficiary of a life insurance policy chooses to receive the benefit in instalments, the benefit is placed into an account that can accrue interest. While the beneficiary will not pay taxes on the benefit itself, they will be responsible for paying income taxes on any interest accrued.

Secondly, there may be taxes involved if a different person holds the role of the policyholder and the insured. In this case, the IRS considers the payout a taxable gift from the policyholder to the beneficiary, and gift taxes may apply if the benefit amount exceeds federal gift tax exemption limits.

Thirdly, if the policy was transferred to the beneficiary for cash or other valuable consideration, the exclusion for the proceeds is limited to the sum of the consideration paid, and taxes may be due on any amount exceeding this sum.

Lastly, if the life insurance proceeds are included as part of the deceased's estate and together exceed the federal estate tax threshold, estate taxes must be paid on the proceeds over the allowed limit.

Life Insurance and Bipolar Disorder: What's Covered?

You may want to see also

Explore related products

![]()

Interest on the payout is taxable

Although death benefits are generally not taxable, interest accrued on the payout is taxable. This is a crucial distinction to make, as it can significantly impact the beneficiary's financial outcome. Here are some key points to consider regarding the taxability of interest on death insurance payouts:

Taxable Scenarios

In certain scenarios, interest on death insurance payouts is subject to taxation. One such scenario is when the beneficiary chooses to receive the payout in installments. In this case, the insurance company will place the benefit into an interest-bearing account, and the beneficiary will be responsible for paying income taxes on the accrued interest. This scenario is important to consider, as it gives the beneficiary more control over the taxation of their benefit. By choosing to receive the payout in installments, they can potentially time the disbursements to align with their overall financial strategy and tax planning.

Another scenario where interest on death insurance payouts may be taxable is when the policy has accumulated substantial interest over time. Whole life insurance and universal life insurance policies, for example, earn interest, contributing to their cash value. If the beneficiary takes out a loan or withdrawal that exceeds the total amount of premiums paid, the excess, including any accrued interest, can be taxed. This is an important consideration for policyholders who intend to borrow against their policy or make withdrawals, as it can impact the overall value of their benefit.

Tax Strategies

To mitigate the tax burden on beneficiaries, policyholders can consider transferring ownership of their policy to another person or entity. By doing so, they can remove the death benefit from their estate, potentially reducing the tax liability for their loved ones. Additionally, setting up an irrevocable life insurance trust (ILIT) ensures that the trust owns the policy rather than the individual, which can provide additional tax advantages. These strategies demonstrate the importance of proactive tax planning when setting up a life insurance policy.

Tax Exemptions

While interest on death insurance payouts is generally taxable, there are certain exemptions. For example, accelerated death benefits received under a life insurance contract for a terminally or chronically ill individual are typically excluded from taxable income. Additionally, unreimbursed medical care expenses may be deductible if the beneficiary is eligible to itemize their deductions. These exemptions highlight the importance of understanding the specific circumstances surrounding the policy and the beneficiary's situation.

In conclusion, while death benefits themselves are typically tax-exempt, the interest accrued on these payouts is generally subject to taxation. This distinction has important implications for both the policyholder and the beneficiary. By understanding the tax treatment of interest on death insurance payouts, individuals can make more informed decisions when setting up or modifying their life insurance policies, ultimately maximizing the benefit for their loved ones.

Annuities and Life Insurance: What's the Connection?

You may want to see also

Explore related products

![]()

Employer-paid plans over $50,000 may be taxable

Generally, life insurance payouts are not taxable. However, there are some exceptions to this rule. One such exception is when an employer-paid plan exceeds a certain amount. According to the Internal Revenue Service (IRS), if an employer-paid group life plan pays out more than $50,000, the amount over $50,000 may be taxable. This means that if the payout exceeds $50,000, the beneficiary may have to pay taxes on the portion of the benefit that exceeds this threshold. It's important to note that this rule specifically applies to group life plans that are fully paid by the employer.

In such cases, the beneficiary of the life insurance policy may be responsible for paying taxes on a portion of the death benefit. This is an important consideration for individuals who are setting up their life insurance policies and planning their estates. It's always a good idea to review the specific details and rules around taxation with a financial advisor or tax professional to ensure that you understand any potential tax implications.

The taxation of life insurance payouts can be a complex topic, and there are other exceptions and scenarios that can impact whether or not a payout is taxable. For example, if the life insurance proceeds have accumulated interest, taxes are typically due on the interest earned, even if the death benefit itself is not taxable. This is because interest income is generally considered taxable income. Additionally, if the life insurance policy is included as part of the deceased's estate, and the total value exceeds certain thresholds, estate taxes may need to be paid.

It's worth noting that there are strategies that beneficiaries can employ to minimise tax liability. For instance, transferring ownership of the policy to another person or entity can help avoid taxation in certain cases. Additionally, setting up an irrevocable life insurance trust (ILIT) ensures that the trust owns the policy rather than the individual, which can have tax advantages. Consulting with a tax professional or financial advisor can help individuals navigate these complexities and make informed decisions regarding their life insurance policies and tax obligations.

Life, AD&D Insurance: What's Supplemental Coverage?

You may want to see also

Explore related products

![]()

Estate taxes may apply if proceeds exceed the federal threshold

Life insurance payouts are generally not taxable. However, there are some exceptions to this rule. One such exception is estate taxes, which may apply when the proceeds from the life insurance policy are included as part of the deceased's estate and together exceed the federal estate tax threshold. As of 2023, this threshold is set at $12.92 million, and any amount over this limit is subject to estate taxes.

In the context of life insurance, an estate refers to when a policyholder chooses their estate as the beneficiary of their policy. In such cases, the death benefit is paid directly to the estate rather than to a specific individual or entity. This scenario is less common than designating a person or entity as the beneficiary, but it can occur when the policyholder wants to ensure the proceeds are used for specific purposes or distributed according to their wishes.

When the life insurance proceeds are included in the estate, the total value of the estate, including the death benefit, is considered when determining estate taxes. If the combined value exceeds the federal threshold, taxes must be paid on the portion that surpasses the allowed limit. This means that the beneficiaries or heirs of the estate will be responsible for paying taxes on the excess amount.

It is important to note that estate taxes are separate from other taxes that may apply to life insurance proceeds, such as gift taxes or income taxes on accrued interest. While estate taxes are triggered by the total value of the estate, gift taxes come into play when the life insurance policy's cash value exceeds the gift tax exemption. As of 2023, the gift tax exemption is $17,000 per year or $12.92 million per individual over their lifetime. Additionally, while the death benefit itself is typically not taxable, any interest accrued on the payout may be subject to income taxes.

Life Insurance and THC: Does AAA Test for It?

You may want to see also

Explore related products

![]()

Policy riders are usually not taxed

Life insurance payouts are generally not taxable, but there are some exceptions. Policy riders are typically not taxed, but they will reduce the amount that the beneficiary receives. Riders are optional features that can be added to a standard life insurance policy to cover specific life events. For example, WAEPA's Chronic Illness Rider allows policyholders to collect up to 50% of their Group Term Life Insurance benefit to help cover chronic illness costs. This benefit is paid directly to the policyholder over four years and is tax-free.

If a life insurance policy has accumulated interest, taxes are usually due on the interest accrued. The death benefit is typically exempt from income tax, but if the beneficiary chooses to receive the benefit in instalments, the benefit is placed in an account that can accrue interest. While the beneficiary will not pay taxes on the benefit itself, they will be responsible for paying income taxes on any interest accrued.

In the case of employer-paid group life plans, a payout of more than $50,000 may be taxable, according to the Internal Revenue Service (IRS). Additionally, if the death benefit and the total value of the deceased's estate exceed the federal estate tax threshold, estate taxes must be paid on the proceeds over the allowed limit. As of 2023, the estate tax threshold is $12.92 million.

Furthermore, if the policy was transferred for cash or other valuable consideration, the exclusion for proceeds is limited to the sum of the consideration paid. There may also be tax implications if the policyholder chooses their estate as the beneficiary, depending on the estate's value.

Life Insurance: Organization and Its Benefits Explained

You may want to see also

Frequently asked questions

Death benefits are generally exempt from income tax. However, there are some exceptions. For example, if the payout has accumulated interest, taxes are usually due on the interest.

If the death benefit and the total value of the deceased's estate exceed the federal estate tax threshold, estate taxes must be paid on the proceeds over the allowed limit. As of 2023, the threshold is \$12.92 million.

Yes, if the policyholder chose their estate as a life insurance beneficiary, taxes might apply. The taxes depend on the estate's value.

The benefit is placed into an account that can accrue interest. While the beneficiary will not pay taxes on the benefit itself, they will be responsible for paying income taxes on any interest accrued.